7 Credit Card Facts Every User Must Know – Avoid Costly Mistakes

Table of Contents

Credit Card Information is fundamental knowledge in today’s digital economy, where plastic and digital payments have largely supplanted cash as the primary method for transactions. For many, a credit card is an indispensable financial tool, offering convenience, security, and the ability to manage cash flow effectively. However, the seemingly simple act of swiping or tapping a card belies a complex financial instrument that, if not understood and managed properly, can lead to significant financial distress. This comprehensive guide aims to arm every credit card user, from novice to experienced, with the essential information needed to navigate the world of credit cards responsibly and to maximize their benefits while minimizing potential pitfalls.

How Credit Cards Work: The Mechanics Behind Your Spending

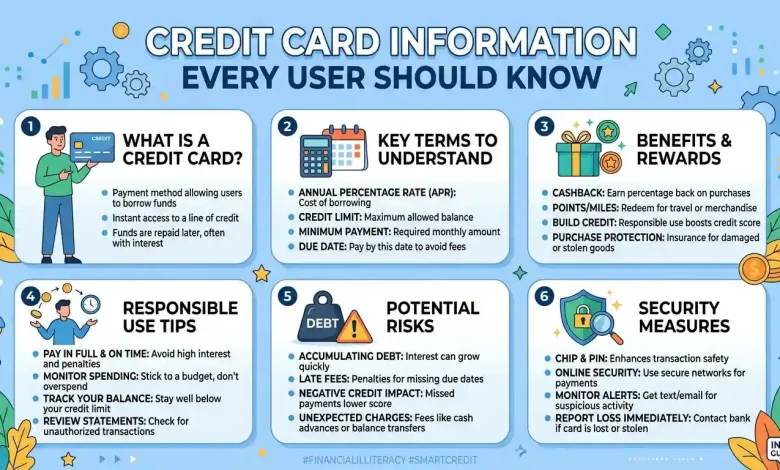

At its core, a credit card is a revolving line of credit extended to you by a financial institution, such as a bank or credit union. Unlike a debit card, which draws funds directly from your bank account, a credit card allows you to borrow money up to a pre-set limit to make purchases. When you use your credit card, the issuer pays the merchant on your behalf, and you, in turn, become obligated to repay the issuer. This repayment typically includes the principal amount borrowed, along with any accrued interest and fees, by a specified due date. The issuer essentially offers short-term loans for your purchases.

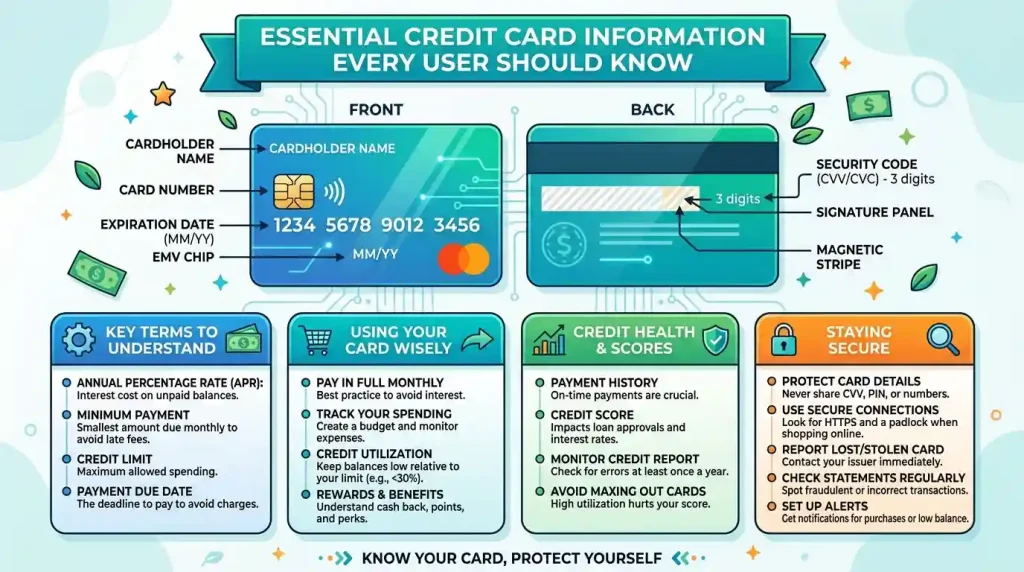

- Credit Limit: This is the maximum amount of money you can charge on your credit card. It’s determined by factors such as your income, credit history, and debt-to-income ratio.

- Billing Cycle: This is the period, usually 28-31 days, for which your credit card statement is generated. All transactions within this period are grouped together.

- Statement Date: The day your billing cycle ends and your statement is generated, detailing all your purchases, payments, and any outstanding balance.

- Due Date: The date by which your payment must be received by the credit card issuer to avoid late fees and interest charges on your new purchases. Typically, it’s 21 to 25 days after your statement date.

- Grace Period: This is the period between your statement date and your payment due date during which you can pay your balance in full without incurring interest on new purchases. If you carry a balance, new purchases will typically start accruing interest immediately.

- Minimum Payment: The smallest amount you must pay by the due date to keep your account in good standing. Paying only the minimum, however, means you’ll pay more interest over time and it will take longer to clear your debt.

Understanding Different Types of Credit Cards

The credit card market is diverse, offering a multitude of options tailored to various financial needs and lifestyles. Understanding the different types is crucial for selecting a card that aligns with your spending habits and financial goals.

- Standard Credit Cards: These are general-purpose cards suitable for everyday purchases. They often come with a range of interest rates and may or may not include rewards programs.

- Rewards Credit Cards: Designed to incentivize spending, these cards offer benefits like cashback, travel points, airline miles, or other perks for eligible purchases. The rewards structure can vary significantly, so it’s important to choose one that aligns with your spending categories.

- Travel Credit Cards: A subset of rewards cards, these are specifically geared towards travelers, offering benefits such as airline miles, hotel points, travel insurance, airport lounge access, and no foreign transaction fees.

- Balance Transfer Credit Cards: These cards offer a low or 0% introductory APR for a set period, designed to help consumers transfer high-interest debt from other credit cards and pay it off more quickly without accruing additional interest during the promotional period. A balance transfer fee usually applies.

- Secured Credit Cards: Ideal for individuals with no credit history or poor credit, secured credit cards require a cash deposit that typically acts as your credit limit. This deposit serves as collateral, reducing the risk for the issuer. Regular, on-time payments help build or rebuild credit history.

- Student Credit Cards: Tailored for college students, these cards often have lower credit limits and may offer rewards relevant to student life. They serve as an entry point for students to begin building a credit history.

- Business Credit Cards: Designed for small business owners, these cards help separate personal and business expenses, often offering rewards on business-related spending categories and tools for expense tracking.

Navigating Interest Rates, Fees, and Charges

One of the most critical aspects of credit card ownership is understanding the associated costs beyond the principal amount of your purchases. These costs primarily come in the form of interest rates and various fees.

- Annual Percentage Rate (APR): This is the annual rate of interest charged on your outstanding balance. APRs can be fixed or variable, meaning they can fluctuate with market rates. Introductory or promotional APRs are often low or 0% for a period before reverting to a standard rate.

- Cash Advance APR: Typically higher than the purchase APR, this rate applies to cash advances taken from your credit card. There is usually no grace period for cash advances, meaning interest accrues immediately.

- Penalty APR: A significantly higher APR that can be applied to your account if you make a late payment or violate other terms of your cardholder agreement. This rate can remain in effect for a considerable period.

- Annual Fee: Some credit cards, particularly those with premium rewards or benefits, charge a yearly fee for the privilege of holding the card.

- Late Payment Fee: Charged when your minimum payment is not received by the due date.

- Balance Transfer Fee: A fee, usually a percentage of the amount transferred, applied when you move debt from one credit card to another.

- Cash Advance Fee: A fee charged for taking a cash advance, typically a percentage of the amount withdrawn or a flat fee, whichever is greater.

- Foreign Transaction Fee: A fee, usually 1% to 3% of the transaction amount, charged when you make a purchase in a foreign currency or through a foreign merchant. Many travel cards waive this fee.

- Over-the-Limit Fee: Charged if you exceed your credit limit. However, regulations often require cardholders to opt-in for over-limit transactions, otherwise, transactions exceeding the limit will simply be declined.

Understanding these costs is paramount. Carrying a balance and only paying the minimum can lead to a significant portion of your payments going towards interest rather than the principal, prolonging debt repayment significantly.

| Fee Type | Description | Typical Range | How to Avoid |

|---|---|---|---|

| Annual Fee | A yearly charge for card membership. | $0 – $550+ | Choose no-annual-fee cards or ensure rewards outweigh the cost. |

| Late Payment Fee | Charged for not paying the minimum by the due date. | Up to $41 (in the US) | Pay on time, set up automatic payments or reminders. |

| Balance Transfer Fee | Fee for transferring debt from another card. | 3% – 5% of transferred amount | Consider cards with no balance transfer fee promotions. |

| Cash Advance Fee | Charged for withdrawing cash with your credit card. | 3% – 5% of advanced amount or flat fee | Avoid cash advances; use a debit card for cash. |

| Foreign Transaction Fee | Applied to purchases made in foreign currency or abroad. | 1% – 3% of transaction | Use a travel-friendly credit card with no foreign transaction fees. |

Building and Maintaining a Strong Credit Score

Your credit score is a three-digit number that represents your creditworthiness to lenders. It significantly impacts your ability to secure loans, mortgages, car financing, and even apartment rentals or insurance rates. A credit card, used responsibly, is one of the most effective tools for building and maintaining a good credit score.

- Payment History (35%): The most critical factor. Always pay your bills on time. Even a single late payment can negatively impact your score.

- Amounts Owed (30%): This refers to your credit utilization ratio – the amount of credit you’re using compared to your total available credit. Keeping this ratio low (ideally below 30%) indicates responsible credit management.

- Length of Credit History (15%): The longer your credit accounts have been open and in good standing, the better. Avoid closing old, unused accounts, especially if they have a positive history.

- New Credit (10%): Applying for too much new credit in a short period can be a red flag to lenders. Each application can result in a hard inquiry on your credit report, which can slightly lower your score temporarily.

- Credit Mix (10%): Having a healthy mix of different types of credit (e.g., credit cards, installment loans, mortgages) can positively impact your score, showing you can manage various forms of debt.

To establish credit, start with a secured credit card or a student card. Make small purchases and pay them off in full every month. Gradually, you can qualify for unsecured cards with higher limits.

Credit Card Security and Fraud Prevention

In an age of increasing digital transactions, safeguarding your credit card information is paramount. Credit card fraud is a significant concern, but with proper precautions, you can minimize your risk.

- Protect Your Physical Card: Treat your card like cash. Keep it in a secure place, don’t let it out of your sight during transactions, and never write your PIN on the card.

- Online Security: Only use your credit card on secure websites (look for “https://” in the URL and a padlock icon). Be wary of unsolicited emails or calls asking for your card details.

- PIN Protection: Memorize your PIN and never share it. When using an ATM or POS terminal, cover the keypad while entering your PIN.

- Review Statements Regularly: Promptly review your credit card statements for any unauthorized transactions. Report discrepancies immediately to your card issuer.

- Set Up Alerts: Many card issuers offer transaction alerts via email or SMS. These can notify you of purchases made on your card, allowing you to quickly identify fraudulent activity.

- Use Strong Passwords: For online credit card accounts, use unique, strong passwords and consider enabling two-factor authentication.

- Shred Documents: Securely shred old credit card statements, offers, and receipts that contain personal or financial information.

- Be Wary of Public Wi-Fi: Avoid making financial transactions or accessing sensitive accounts when connected to unsecured public Wi-Fi networks.

- Report Lost/Stolen Cards: Immediately report a lost or stolen credit card to your issuer. Most companies offer zero-liability policies, protecting you from unauthorized charges.

- EMV Chip Technology: The EMV chip provides enhanced security by encrypting transaction data, making it much harder for fraudsters to clone your card. Always use the chip reader when available.

Strategies for Managing Credit Card Debt

While credit cards offer immense convenience, they can also lead to accumulating debt if not managed carefully. Uncontrolled credit card debt can spiral, affecting your financial health and credit score. Here are effective strategies for debt management:

- Pay in Full: The golden rule of credit card management is to pay your balance in full every month. This ensures you avoid interest charges altogether and leverage the card’s convenience without cost.

- Pay More Than the Minimum: If paying in full isn’t possible, always aim to pay more than the minimum due. This reduces your principal balance faster, saving you interest in the long run.

- Debt Snowball Method: This strategy involves paying off your smallest debt first while making minimum payments on others. Once the smallest is paid, you apply its payment to the next smallest, creating a “snowball” effect. This method provides psychological wins.

- Debt Avalanche Method: With this method, you prioritize paying off the debt with the highest interest rate first, while making minimum payments on others. This strategy is mathematically more efficient as it saves you the most money on interest.

- Balance Transfer: As mentioned, a balance transfer card with a 0% introductory APR can provide a window to pay down high-interest debt without new interest accruing. Be mindful of the balance transfer fee and ensure you can pay off the transferred amount before the promotional period ends.

- Debt Consolidation Loan: You might consider a personal loan to consolidate multiple credit card debts into a single payment, often with a lower interest rate. This simplifies repayment and can reduce overall interest costs.

- Budgeting: Create a realistic budget to track your income and expenses. This helps identify areas where you can cut back and allocate more funds towards debt repayment.

- Avoid New Debt: While actively paying down debt, refrain from using your credit cards for new purchases, or use them only for items you can immediately pay off.

The Benefits and Drawbacks of Credit Cards

Credit cards are powerful financial tools, but like any tool, they have both advantages and disadvantages. A balanced understanding is crucial for responsible usage.

Benefits:

- Convenience: Credit cards offer a convenient way to make purchases without carrying cash. They are widely accepted globally.

- Building Credit History: Responsible use of a credit card is one of the most effective ways to build a positive credit history, which is essential for future financial endeavors.

- Fraud Protection: Credit cards generally offer robust fraud protection, often with zero-liability policies, shielding you from unauthorized charges. Debit cards offer less protection.

- Emergency Funds: A credit card can serve as a lifeline in unexpected financial emergencies, providing access to funds when immediate cash is unavailable.

- Rewards and Perks: Many cards offer cashback, travel miles, points, purchase protection, extended warranties, and other valuable benefits that can lead to significant savings or added value.

- Record Keeping: Credit card statements provide a detailed record of your spending, which can be useful for budgeting, tracking expenses, and tax purposes.

- No Foreign Transaction Fees: Some credit cards waive foreign transaction fees, making them ideal for international travel.

Drawbacks:

- Interest Charges: If you don’t pay your balance in full, interest can quickly accrue, making purchases more expensive over time.

- Debt Accumulation: The ease of spending can lead to overspending and accumulating unmanageable debt, which can have long-term negative financial consequences.

- Fees: Annual fees, late payment fees, cash advance fees, and other charges can add to the cost of using a credit card.

- Impact on Credit Score: Irresponsible use, such as late payments, high credit utilization, or default, can severely damage your credit score.

- Potential for Fraud: While protected, credit cards are still targets for fraudsters, requiring vigilance and security measures from the user.

- Temptation to Overspend: The psychological effect of using “borrowed” money can make it easier to spend more than you can afford.

For further insights into credit card trends and consumer behaviors, authoritative financial publications and research institutions often provide valuable data. For example, reports from financial bodies or even general news outlets often detail the prevalence of credit card usage and common pitfalls. For an authoritative source on general financial topics and consumer advice, one might consult resources such as Reuters financial news.

Choosing the Right Credit Card for Your Needs

With countless credit card options available, selecting the right one can feel daunting. A thoughtful approach, considering your financial situation and goals, is key.

- Assess Your Credit Score: Your current credit score will largely determine the types of cards you qualify for. If your score is low, you might start with a secured card.

- Evaluate Your Spending Habits:

- Are you a frequent traveler? A travel rewards card might be beneficial.

- Do you spend a lot on groceries or gas? Look for cards offering bonus rewards in those categories.

- Do you rarely carry a balance? A rewards card with an annual fee might be worth it if the rewards outweigh the fee.

- Do you anticipate carrying a balance? Prioritize a card with a low regular APR over rewards.

- Compare Interest Rates and Fees: Always examine the APR, annual fee, late payment fees, and any other potential charges. A low introductory APR is attractive, but understand what the rate will revert to.

- Consider Rewards Programs: If you’re disciplined enough to pay your balance in full, a rewards card can offer significant value. Compare cashback rates, point values, and redemption options.

- Look at Sign-Up Bonuses: Many cards offer attractive sign-up bonuses (e.g., bonus points or cashback after spending a certain amount within the first few months). Factor these into your decision, but don’t let them be the sole reason for choosing a card if its long-term features don’t align with your needs.

- Read the Fine Print: Before applying, thoroughly review the terms and conditions. Understand the grace period, penalty rates, and any specific requirements for earning or redeeming rewards.

- Customer Service and Digital Tools: Consider the card issuer’s reputation for customer service and the quality of their online banking and mobile app. These can greatly impact your experience.

Remember, the “best” credit card isn’t universal; it’s the one that best suits your individual financial behavior and goals. Don’t be swayed by flashy advertisements without understanding the underlying terms.

Conclusion

Credit cards are powerful financial instruments that offer unparalleled convenience, security, and opportunities to build a strong financial foundation. However, their benefits are contingent upon responsible usage and a thorough understanding of their mechanics. From comprehending interest rates and fees to mastering strategies for credit score building and debt management, every user must be equipped with essential credit card information. By exercising financial discipline, staying vigilant against fraud, and choosing cards that align with individual needs, users can harness the full potential of credit cards to their advantage, ensuring a healthier and more secure financial future. Empowering yourself with this knowledge transforms a simple piece of plastic into a sophisticated tool for financial empowerment.