7 Best Credit Cards in 2026 – Maximize Cashback, Travel & Rewards

Table of Contents

Best Credit Cards in 2026 offer unparalleled opportunities for consumers to earn value back on their everyday spending, whether through direct cashback, lucrative travel perks, or flexible rewards points. In an evolving financial landscape, choosing the right credit card is more strategic than ever, requiring a keen understanding of personal spending habits, financial goals, and the dynamic offerings from various issuers. As we navigate 2026, the credit card market continues to innovate, providing a diverse array of products designed to cater to every type of consumer, from the budget-conscious shopper to the frequent international traveler. This comprehensive guide aims to illuminate the top contenders across key categories, helping you make informed decisions to optimize your financial strategy and unlock significant value from your credit card usage.

Introduction to Credit Cards in 2026

Credit cards in 2026 are resilient financial instruments, enabling consumers to manage borrowing and transactions despite ongoing economic shifts such as fluctuating interest rates and inflation. The market is characterized by steady growth and moderate risk, with an increasing emphasis on personalized experiences and advanced technological integrations like AI-driven analytics. The average FICO Score in the U.S. is noted to be around 715, indicating a generally healthy credit environment, though lenders continue to maintain disciplined underwriting standards. Consumers are increasingly looking for cards that not only offer transactional convenience but also provide substantial benefits that align with their lifestyles, whether that means direct savings, travel upgrades, or versatile points. Understanding the nuances of different card types and their associated reward structures is crucial for maximizing these benefits in the current year.

Understanding Credit Card Categories: Cashback, Travel, and General Rewards

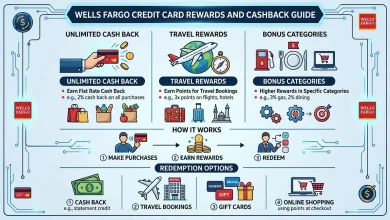

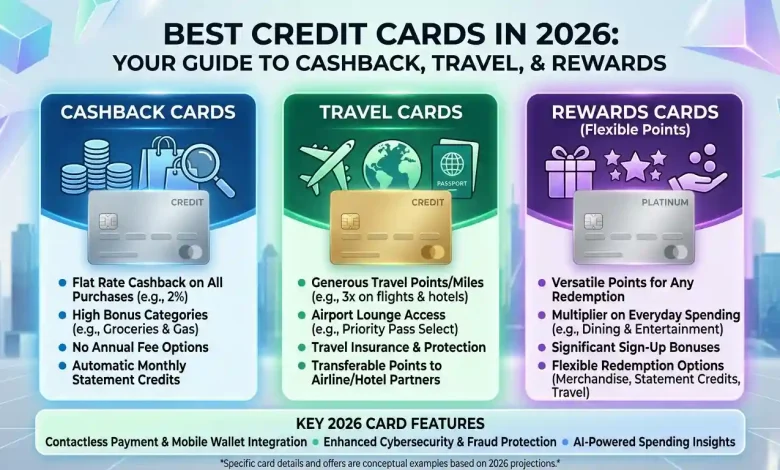

Credit card rewards typically fall into three primary categories: cashback, travel rewards, and general points programs, each offering distinct advantages based on a cardholder’s spending patterns and financial objectives.

- Cashback Credit Cards: These cards offer a percentage of money back on eligible purchases, providing tangible savings on everyday expenses. Cashback can be earned at a flat rate on all purchases, in tiered categories where certain spending areas yield higher percentages (e.g., groceries, gas, dining), or through rotating bonus categories that change quarterly. Cashback is often redeemed as a statement credit, direct deposit, or check, offering simplicity and flexibility.

- Travel Rewards Credit Cards: Designed for frequent travelers, these cards allow cardholders to earn points or miles that can be redeemed for flights, hotel stays, rental cars, and other travel-related expenses. Many travel cards come with premium perks such as airport lounge access, travel insurance, no foreign transaction fees, and statement credits for Global Entry or TSA PreCheck. The value of travel points can often be maximized by transferring them to airline or hotel loyalty partners.

- General Rewards Credit Cards: These programs typically offer points that can be redeemed for a variety of options, including cashback, gift cards, merchandise, and sometimes travel. They strike a balance between the simplicity of cashback and the specific benefits of travel cards, offering flexibility for cardholders who may not exclusively prioritize one type of reward. The value of these points can vary significantly depending on the redemption method, so strategic redemption is key.

Key Trends Shaping the Credit Card Landscape in 2026

The credit card industry in 2026 is experiencing several transformative trends, driven by technological advancements and evolving consumer expectations:

- Increased Personalization and AI Integration: Artificial intelligence is making credit cards “smarter” by enabling more personalization and connecting broader data points for cross-product integration. This means card offers and features are becoming more tailored to individual spending habits and needs. Issuers are leveraging AI for real-time underwriting and advanced fraud prevention, enhancing security and efficiency.

- Evolution of Rewards Programs: Premium credit card offers, often with substantial annual fees, continue to target high-quality cardholders with generous point offers. However, there’s a recognized shift, with cardholders expecting more value as they understand the importance of their transactions to merchants and lenders. Loyalty program transfer rates are expected to see ongoing devaluations, making points and miles less valuable if not redeemed promptly.

- Emphasis on Issuer Travel Portals: Credit card issuers are increasingly enhancing their own travel portals, offering more incentives, such as higher redemption values and bonus points, for bookings made directly through their platforms. This trend is expected to continue, though consumers should be aware that booking through a portal might sometimes be more expensive than external options.

- BNPL and Card Convergence: The distinction between “Buy Now, Pay Later” (BNPL) services and traditional credit cards is blurring. “Installments at the Point of Sale” is becoming a standard feature on major card networks, allowing existing credit cards to convert transactions into fixed-fee loans directly. This trend is partly driven by regulatory changes bringing BNPL under the same umbrella as traditional credit.

- Enhanced Security with Network Tokenization: Security remains a top priority, with network tokenization gaining significant traction. This technology replaces actual card details with unique digital tokens for online and mobile wallet transactions, making breaches less impactful. The adoption of “Click-to-Pay” is a primary driver of this growth, aiming for frictionless and secure checkouts.

Best Credit Cards for Cashback in 2026

For those who prioritize straightforward savings, cashback credit cards remain a top choice in 2026. These cards often feature bonus categories that align with common spending, or offer a consistent flat rate on all purchases. Determining the “best” card depends largely on your spending profile.

Some of the leading options expected to perform well in 2026 include:

- Citi Double Cash® Card: This card is consistently praised for its simple yet effective reward structure, offering 2% cashback on every purchase—1% when you buy and 1% when you pay your bill. It often comes with no annual fee, making it an excellent choice for a “catch-all” card for miscellaneous expenses that don’t fall into other bonus categories. Additionally, it provides 5% total cashback on hotels, car rentals, and attractions booked through Citi Travel.

- Chase Freedom Unlimited®: Offering a robust tiered rewards system, this card provides 5% cashback on travel purchased through Chase Travel℠, 3% on dining and drugstore purchases, and an unlimited 1.5% cashback on all other purchases. With no annual fee, it’s a versatile option for everyday spending, often with a generous sign-up bonus.

- Blue Cash Preferred® Card from American Express: Ideal for families and those with significant grocery spending, this card typically offers a high percentage of cashback on U.S. supermarket purchases (often 6% up to a spending cap), 6% on select streaming subscriptions, and 3% on transit and U.S. gas stations, with 1% on other purchases. It often has an annual fee, but the high reward rates can easily offset it for eligible spenders.

- Capital One Savor Cash Rewards Credit Card: This card is an excellent fit for those who spend heavily on dining and entertainment, often providing elevated cashback rates in these categories, as well as on popular streaming services. It generally features a sign-up bonus and may have no annual fee, making it attractive for a social lifestyle.

When selecting a cashback card, it’s crucial to analyze your budget and spending habits to identify which categories you spend most in, ensuring the card’s reward structure aligns with your lifestyle.

Premier Travel Credit Cards in 2026

For individuals who frequently travel, either for leisure or business, travel rewards credit cards offer substantial value through points, miles, and premium travel benefits. The key to maximizing these cards lies in understanding their redemption options and leveraging their associated perks.

Top travel credit cards for 2026 include:

- Chase Sapphire Preferred® Card: Widely regarded as an excellent entry point into travel rewards, the Sapphire Preferred offers strong earning potential, particularly 5X points on travel purchased through Chase Travel℠, and 2X points on other travel purchases. It also provides 3X points on dining and usually features a significant sign-up bonus. Points are highly flexible and can be transferred to numerous airline and hotel loyalty programs. It has a modest annual fee which can be offset by a $50 annual Chase Travel hotel credit.

- Capital One Venture X Rewards Credit Card: A premium travel card, the Venture X offers a flat 2X miles on every purchase, 10X miles on hotels and rental cars booked through Capital One Travel, and 5X miles on flights booked through Capital One Travel. Its benefits often include a substantial annual travel credit and airport lounge access, which can significantly offset its higher annual fee. This card is ideal for heavy travelers seeking comfort and flexibility.

- American Express® Gold Card: While often considered a rewards card, the Amex Gold is a powerhouse for travel due to its strong earning rates on dining and groceries (often 4X points), which are transferable to airline partners. It comes with valuable statement credits (e.g., dining credits, Uber Cash) that can help offset its annual fee, making it a favorite for foodies and frequent flyers alike.

- Chase Sapphire Reserve®: This card is a premium option for serious travelers, offering enhanced rewards rates on travel (e.g., 10X points on hotels and car rentals, 5X on flights booked through Chase Travel℠) and dining (3X points). It features a higher annual fee but includes a flexible $300 annual travel credit, Priority Pass™ Select lounge access, and a Global Entry/TSA PreCheck credit, making it very valuable for those who leverage its extensive perks.

- American Express Platinum Card®: The “gold standard” for luxury travel, this card provides extensive benefits such as access to exclusive Centurion Lounges, Priority Pass, and Plaza Premium lounges, alongside substantial annual credits for various services (e.g., digital entertainment, Uber, hotel credits). Its high annual fee is justified for those who can fully utilize its luxury perks and travel benefits, including 5X points on flights booked directly with airlines or Amex Travel and on prepaid hotels.

When comparing travel cards, evaluate factors like welcome bonuses, annual fees, foreign transaction fees, interest rates, and the ease of redeeming points or miles.

| Credit Card Category | Primary Benefit | Ideal User Profile | Key Considerations |

|---|---|---|---|

| Cashback | Direct percentage back on purchases | Everyday spenders, budget-conscious, those seeking simplicity | Flat rate vs. rotating/tiered categories, annual fee (often none) |

| Travel Rewards | Points/miles for flights, hotels, travel perks | Frequent flyers, international travelers, those valuing luxury travel benefits | Annual fees, foreign transaction fees, lounge access, transfer partners, sign-up bonuses |

| General Rewards | Flexible points redeemable for various options | Consumers with diverse spending habits, those who value redemption flexibility | Point valuation for different redemption types, annual fees, bonus categories |

| Business Cards | Rewards and tools for business expenses | Small business owners, freelancers, entrepreneurs | Spend management tools, fraud protection, employee cards |

| Secured Cards | Build or rebuild credit history | Individuals with limited or poor credit history | Requires a security deposit, reports to credit bureaus, low credit limits |

Top General Rewards Credit Cards in 2026

General rewards credit cards offer a flexible approach to earning value, allowing cardholders to redeem points for a wide array of options, including statement credits, gift cards, merchandise, and sometimes travel. These cards are suitable for consumers who may not have a singular focus on cashback or travel but appreciate the versatility of their rewards.

Prominent general rewards cards for 2026 include:

- Wells Fargo Rewards Program: In 2025, Wells Fargo was identified as having one of the best overall credit card rewards programs, earning high WalletHub scores. Their rewards cards typically offer competitive earning potential across various categories, with flexible redemption options. Redeeming for travel often yields higher value compared to merchandise or even cashback.

- Capital One Venture Rewards Credit Card: While often categorized under travel, the Capital One Venture Card also functions effectively as a general rewards card due to its straightforward earning of 2X miles on every purchase, which can be easily redeemed for a statement credit to cover travel purchases, or transferred to various travel partners. Its simplicity and consistent earning rate make it appealing for those who want flexible rewards without complex category tracking.

- American Express Membership Rewards Program: Several Amex cards, such as the American Express® Gold Card and American Express Platinum Card®, accrue Membership Rewards points. These points are highly valuable and incredibly flexible, redeemable for travel through Amex Travel, transfers to numerous airline and hotel partners, gift cards, or even statement credits. The value per point can vary significantly based on the redemption method, with travel transfers often providing the highest value.

- Chase Ultimate Rewards Program: Cards like the Chase Freedom Unlimited® and Chase Sapphire Preferred® accrue Ultimate Rewards points. This program is renowned for its flexibility and high value, allowing points to be redeemed for cashback, gift cards, or travel through the Chase Travel℠ portal, often at an elevated rate for Sapphire cardholders. The ability to transfer points to various airline and hotel partners also enhances their utility for travel.

When considering a general rewards card, assess how points are earned, the average value per point across different redemption options, and any associated annual fees. Flexibility in redemption is a significant advantage, but it requires understanding the optimal ways to use your accumulated points for maximum benefit.

How to Choose the Best Credit Card for Your Lifestyle

Selecting the ideal credit card in 2026 requires a thoughtful assessment of your financial habits and goals. The “best” card is highly individual, tailored to how you spend and what you hope to gain from your rewards.

- Analyze Your Spending Habits: This is the foundational step. Review your bank statements or use a budgeting app to understand where most of your money goes each month—groceries, dining out, gas, online shopping, or travel. If you spend a lot on specific categories, a card with bonus rewards in those areas will be most beneficial.

- Define Your Rewards Goals: Decide what kind of rewards you value most. Do you want direct cash back to offset everyday expenses or save money? Are you aiming for free flights and hotel stays? Or do you prefer flexible points that can be used for a mix of options? Your preference between cashback, travel, or general points will guide your choice.

- Evaluate Annual Fees vs. Benefits: Many premium rewards cards come with annual fees, which can range from modest to several hundred dollars. It’s essential to perform a cost-benefit analysis to determine if the value of the rewards and perks (e.g., travel credits, lounge access, insurance benefits) outweighs the annual fee. Some cards offer no annual fee, providing rewards without an upfront cost.

- Consider Introductory Offers and Sign-Up Bonuses: Many cards offer generous sign-up bonuses for new cardmembers who meet a specified spending threshold within the first few months. These bonuses can provide a significant boost to your rewards balance, but ensure you can meet the spending requirement with your planned purchases, not by overspending.

- Review Interest Rates and Other Fees: While focusing on rewards, don’t overlook the Annual Percentage Rate (APR). If you anticipate carrying a balance, a card with a lower APR is paramount, as interest charges can quickly erode any earned rewards. Also, check for foreign transaction fees if you travel internationally.

- Assess Your Credit Score and History: Your creditworthiness plays a significant role in approval for top-tier cards. A higher FICO Score and a strong credit history increase your chances of qualifying for cards with the most lucrative rewards and benefits. If your credit is still developing, consider cards designed for fair credit or secured cards to build your history.

- Simplicity vs. Optimization: Some cardholders prefer a simple, flat-rate cashback card, while others enjoy strategically using multiple cards to maximize rewards in different spending categories. Choose an approach that matches your comfort level with managing multiple cards and tracking varied reward structures.

Ultimately, the best credit card seamlessly integrates into your financial life, offering rewards that genuinely benefit you without encouraging overspending or accumulating debt.

Maximizing Your Credit Card Benefits and Rewards

Earning rewards is only half the battle; truly maximizing your credit card benefits involves strategic usage and smart redemption. By following these practices, you can turn everyday spending into significant financial advantages in 2026.

- Align Cards with Spending Habits: Use the right card for the right purchase. If you have multiple cards, use the one that offers the highest reward rate for a specific category (e.g., a grocery card for supermarket runs, a dining card for restaurants).

- Capitalize on Sign-Up Bonuses: These are often the quickest way to accumulate a large sum of points or cashback. Plan any major purchases around the introductory spending period to meet the requirements without overspending.

- Pay Your Balance in Full and On Time: This is arguably the most crucial tip. Interest charges and late fees can quickly negate any rewards earned. Paying in full also helps maintain a healthy credit score by keeping your credit utilization low.

- Redeem Rewards Wisely: Understand the value of your points across different redemption options. For travel cards, transferring points to airline or hotel partners often yields the highest value. For cashback, direct deposits or statement credits ensure full value. Avoid redeeming for merchandise unless it offers comparable value.

- Monitor Bonus Categories and Promotions: Many cards offer rotating bonus categories or special promotions that provide additional rewards. Stay informed about these offers and adjust your spending accordingly to maximize earnings.

- Leverage Card Perks: Beyond points, many cards offer valuable benefits like travel insurance, extended warranties, purchase protection, airport lounge access, and statement credits. Make sure you’re aware of and utilizing all the perks your card offers to get the full value.

- Avoid Overspending for Rewards: Never spend money you wouldn’t otherwise spend just to earn more rewards or hit a bonus threshold. Credit cards should complement your budget, not dictate it.

- Review and Refresh Your Cards Regularly: Your spending habits and credit card offerings change over time. Periodically reassess your card portfolio to ensure it still aligns with your current lifestyle and financial goals. Look for benefits you’re paying for but not using.

For more detailed strategies on maximizing credit card rewards, consider consulting resources like Wikipedia’s comprehensive article on Credit Card Reward Programs for a broader understanding of how these systems work globally.

Applying for a Credit Card in 2026: What Issuers Look For

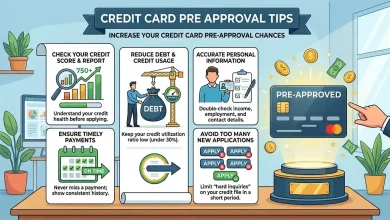

When applying for a new credit card in 2026, understanding the criteria that issuers consider can significantly improve your chances of approval. Lenders use a variety of factors to assess your creditworthiness and the likelihood of you repaying debt.

- FICO Score and Credit Report: This is often the most critical factor. Issuers will pull at least one of your credit reports and a FICO Score based on it. A higher score generally indicates lower risk and better chances of approval for premium cards with lower interest rates. Your credit report details your payment history, types of credit, amounts owed, and length of credit history.

- Income and Debt-to-Income Ratio: Credit card applications typically ask for your household income and monthly housing bills. Issuers use this to estimate your debt-to-income (DTI) ratio, ensuring you have enough income or assets to afford the card’s minimum payments. Some cards also have minimum income requirements.

- Credit History Length and Types: A longer credit history with a mix of different credit accounts (e.g., installment loans, previous credit cards) demonstrates responsible borrowing. If you have a short credit history, consider starting with a secured or student credit card to build it.

- Credit Utilization Rate: This refers to the amount of credit you’re using compared to your total available credit. Keeping your credit utilization low (ideally below 30%) is a strong indicator of responsible credit management.

- Number of Delinquencies and Hard Inquiries: A history of late payments or delinquencies will negatively impact your application. Similarly, too many recent “hard inquiries” (which occur when you apply for new credit) can temporarily lower your credit score and signal to lenders that you might be a higher risk.

- Relationship with the Company: If you have an existing banking relationship with the issuer, or have responsibly managed other products from them, it can sometimes be a favorable factor in your application.

Before applying, utilize pre-qualification tools offered by many issuers. These allow you to see if you’re likely to qualify without a hard credit inquiry, helping you gauge your eligibility and avoid unnecessary dings to your credit score. Remember, applying for multiple cards within a short period can hurt your credit score, so apply sparingly and strategically.

Conclusion

The landscape of credit cards in 2026 continues to offer immense value to consumers willing to navigate its diverse offerings. Whether your priority is maximizing cashback on everyday purchases, unlocking luxurious travel experiences, or enjoying flexible rewards, there is a credit card tailored to your specific needs. The key to success lies in a diligent approach: understanding your unique spending habits, carefully evaluating card features against your financial goals, and practicing responsible credit management. By staying informed about the latest trends—from AI-driven personalization to the evolving nature of rewards programs—and by strategically applying for and utilizing the best credit cards, you can significantly enhance your financial well-being and transform your spending into tangible benefits. Choose wisely, spend responsibly, and let your credit cards work harder for you in the year ahead.