6 Best Credit Cards with No Credit Check for Beginners – Build Credit Easily

Table of Contents

Credit card no credit check options for beginners are a vital stepping stone for individuals looking to establish or rebuild their credit history without facing immediate hurdles. In today’s financial landscape, a good credit score is often essential for significant purchases like a car or a home, securing favorable loan terms, and even renting an apartment. However, for those new to credit, or considered “credit invisible,” getting approved for traditional credit products can be a challenging endeavor. This article will explore various avenues available to beginners, focusing on options that either do not require a traditional credit check or are designed specifically for those with limited to no credit history, helping them responsibly build a positive financial footprint.

Introduction to Building Credit Without a Credit Check

Building credit from scratch can feel like a catch-22: you need credit to get credit. Many traditional credit cards and loans require a solid credit history for approval, leaving beginners in a difficult position. Fortunately, several financial products and strategies are specifically designed to help individuals establish credit without an extensive credit history or even a traditional credit check. These options focus on demonstrating responsible financial behavior over time, which is then reported to the major credit bureaus to build a credit profile. Understanding these alternatives is crucial for anyone starting their financial journey or looking to improve their credit standing. It typically takes three to six months of credit activity to generate a credit score.

Secured Credit Cards: A Solid Foundation

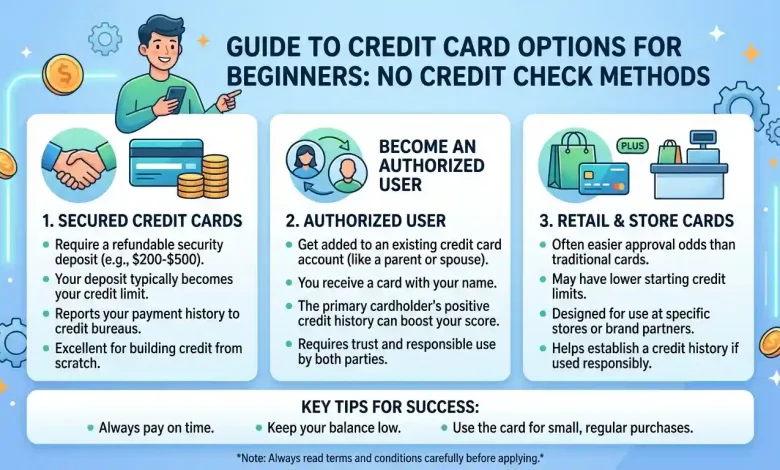

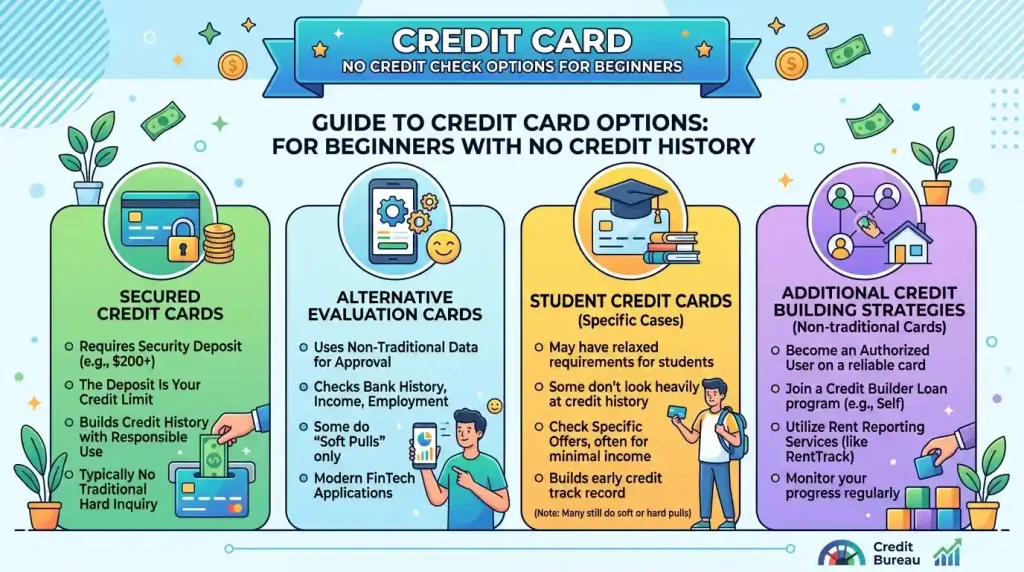

Secured credit cards are arguably one of the most popular and effective no-credit-check options for beginners and those with poor credit alike. Unlike traditional (unsecured) credit cards, a secured credit card requires a refundable cash deposit, which typically serves as your credit limit.

How Secured Credit Cards Work and Why They’re Effective

When you open a secured credit card, you provide the issuer with a security deposit, for example, $200. This $200 then becomes your credit limit. This deposit minimizes the risk for the lender, making these cards much easier to qualify for, even with no credit history. You use the card just like any other credit card, making purchases and then paying your bill each month. The key benefit is that most financial institutions report your account activity, including payment history and credit utilization, to the three major credit bureaus: Experian, Equifax, and TransUnion.

By making on-time payments and keeping your balance low (ideally under 30% of your credit limit), you demonstrate responsible credit behavior, which is then recorded on your credit report. Over time, this consistent positive activity can significantly help build your credit score. After a period of responsible use (often 6-12 months), many secured card issuers may even review your account for an upgrade to an unsecured card and refund your deposit.

It is crucial to choose a secured credit card that reports to all three major credit bureaus to maximize its credit-building potential. Some popular secured card options, such as the Capital One Platinum Secured Credit Card and Discover it® Secured Credit Card, are known for reporting to all three bureaus and may even offer rewards or pathways to upgrade.

- Easier Approval: The security deposit reduces risk for lenders, making approval more accessible.

- Credit Reporting: Responsible use is reported to major credit bureaus, building your credit history.

- Refundable Deposit: The deposit is typically returned when you close the account or graduate to an unsecured card (provided balances are paid).

- Financial Discipline: Helps establish good spending and payment habits within a controlled environment.

Becoming an Authorized User

Another excellent strategy for beginners to build credit without a direct credit check is to become an authorized user on someone else’s credit card account. An authorized user is a person added to an existing credit card account by the primary cardholder, who then receives their own card linked to that account.

When you are an authorized user, the account’s credit limit and payment history may appear on your credit report. If the primary cardholder has a long history of responsible credit use, including on-time payments and low credit utilization, this positive activity can reflect positively on your credit report and help you establish or improve your own credit score.

However, it’s a two-way street. If the primary cardholder makes late payments or carries a high balance, this negative activity can also affect your credit score. Therefore, it’s essential to become an authorized user on an account belonging to someone you trust who has excellent credit habits. You, as the authorized user, are not legally responsible for the debt, but the actions of the primary cardholder directly impact your credit report.

Credit Builder Loans: A Structured Approach

Credit builder loans are specifically designed to help individuals establish or improve their credit history without needing existing credit or a traditional credit check. Unlike a typical loan where you receive funds upfront, with a credit builder loan, the money you “borrow” is held in a savings account or a secured account by the lender.

You then make regular, fixed monthly payments over a period (e.g., 6 to 24 months) to pay off this loan. These on-time payments are reported to the major credit bureaus, demonstrating your ability to handle debt responsibly. Once the loan term is complete and you’ve made all your payments, the funds that were held are released to you, often with interest.

Credit builder loans are beneficial because they provide a structured way to build both a positive payment history and savings simultaneously. They require no collateral upfront and can be approved even with no credit or bad credit. When choosing a credit builder loan, compare options from different credit unions or financial institutions, looking for low interest rates and affordable payment plans.

| Credit-Building Option | Requires Deposit/Collateral | Credit Check Typically Required | Primary Benefit | Potential Drawbacks |

|---|---|---|---|---|

| Secured Credit Card | Yes (Refundable Security Deposit) | No (Easier Approval) | Builds credit with responsible spending and payments. | Ties up cash in a deposit; potential fees. |

| Authorized User | No | No | Leverages primary user’s good credit history. | Dependent on primary user’s credit habits; no legal responsibility for debt. |

| Credit Builder Loan | Yes (Loan amount held in savings) | No (Designed for all credit types) | Builds payment history and savings. | Funds are not immediately accessible; interest and fees apply. |

| Student Credit Card | No (Typically) | Limited/No credit score required. | Opportunity for students to build credit early, often with rewards. | May have lower credit limits or higher interest rates. |

| Cards Using Alternative Data | No (Some options may have fees) | No (Uses income/bank activity instead) | Approval based on non-traditional factors; can offer unsecured credit. | Relatively new; terms can vary; not all widely accepted. |

Student Credit Cards: Tailored for Beginners

For college students with little to no credit history, student credit cards are an excellent option. These cards are specifically designed with more lenient eligibility requirements compared to traditional unsecured credit cards, recognizing that students may not have a substantial income or an extensive credit past. Many student credit cards do not require a credit score for application.

Student cards often come with lower credit limits, which can help beginners manage their spending and develop good credit habits. Many also offer rewards programs and other benefits tailored to student life. Issuers like Discover and Capital One offer popular student credit cards that can help build credit with responsible use. Making on-time payments and keeping balances low on a student card contributes positively to your credit report, setting a strong foundation for future financial endeavors.

Credit Cards Utilizing Alternative Data

A growing number of financial technology (fintech) companies are offering credit cards that move beyond traditional credit scores for approval. These cards utilize “alternative data” such as your banking activity, income, and employment history to assess creditworthiness, rather than relying solely on a FICO or VantageScore.

Some of these cards, like Perpay, Arro, and Current Build Card, explicitly state no hard credit check is required for approval and may even offer unsecured credit lines or secured alternatives with no annual fee or interest. For instance, the Perpay Credit Card assesses eligibility based on your paycheck, while the Current Build Card has no credit check, no annual fee, and no minimum deposit, linking to a checking account to set your spending limit. These options can be particularly attractive for those with absolutely no credit history, as they bypass the traditional barriers of entry.

However, it’s important to research these newer options thoroughly, understand their terms, and verify that they report to all major credit bureaus to ensure your responsible usage actually contributes to building your credit history. Always check for any hidden fees, interest rates, and approval processes. For a detailed guide on various credit-building options including those that use alternative data, you can refer to resources from reputable financial institutions and consumer protection agencies. For instance, the Consumer Financial Protection Bureau (CFPB) offers valuable information on understanding and building credit responsibly: CFPB Guide to Building Credit.

Leveraging Rent and Utility Payments for Credit Building

Traditionally, on-time rent and utility payments do not appear on your credit report. However, this is changing, and these regular payments represent a significant opportunity for beginners to build credit. Several services now allow you to have your on-time rent payments reported to credit bureaus.

Similarly, some services and even certain utility providers (often via third-party platforms) can report your on-time utility and cell phone payments to credit bureaus. Services like Experian Boost, for example, can give you credit for on-time payments you already make, helping to build your credit without taking on debt. This can be a low-effort way to turn existing responsible financial habits into a positive credit history.

It’s worth asking your landlord or property management company if they report payments, or investigating third-party rent reporting services. Be aware that some services may charge fees. The impact on your credit score can vary, as not all credit scoring models accept rental data. Nevertheless, it’s a viable option for those looking to build credit without a traditional credit product.

- Existing Payments: Utilizes payments you already make regularly.

- No New Debt: Builds credit without incurring new debt.

- Direct Impact: On-time payments contribute to your payment history, a significant factor in credit scores.

Conclusion

For beginners seeking credit card no credit check options, the landscape offers several viable pathways to establish a strong credit foundation. Secured credit cards provide a direct route to building credit through responsible use, backed by a refundable deposit. Becoming an authorized user on a trusted family member’s account can offer a valuable boost by leveraging their positive credit history. Credit builder loans offer a structured savings and credit-building program, while student credit cards cater specifically to college students with limited financial experience. Furthermore, innovative credit cards leveraging alternative data, along with services that report rent and utility payments, are expanding the possibilities for those starting from scratch.

The key to success with any of these options is consistent, responsible financial behavior. This includes making all payments on time, keeping credit utilization low, and actively monitoring your credit report. By thoughtfully choosing and diligently managing these credit-building tools, beginners can successfully navigate the journey of establishing credit, opening doors to future financial opportunities and stability. Remember, building credit is a marathon, not a sprint, and patience combined with discipline will yield the best results.