6 Powerful Fortiva Card Facts – Fair Credit Approval & Rewards Guide

Table of Contents

Fortiva Credit Card Review for Fair Credit Users: Navigating the landscape of credit cards when you have fair credit can be a challenging endeavor. Many individuals find themselves in a position where their credit score isn’t quite “good” enough for premium offers, but it’s also not considered “poor,” leaving them in a somewhat ambiguous middle ground. The Fortiva Credit Card is often presented as a solution for this demographic, specifically targeting those with fair to bad credit who are looking for an unsecured credit option without the need for a security deposit. This comprehensive review will delve into the Fortiva Credit Card, examining its features, benefits, drawbacks, and overall suitability for individuals striving to improve their financial standing.

Understanding Fair Credit: What It Means for Borrowers

Before we dissect the specifics of the Fortiva Credit Card, it’s crucial to establish what “fair credit” entails. According to the FICO Score scale, a fair credit score typically falls within the range of 580 to 669. The VantageScore model also identifies a similar range, often categorizing scores between 601 and 660 as “near prime” or “fair.” Individuals in this range may have an inconsistent payment history, higher credit card debt, or a relatively short credit history. While fair credit is a step up from poor credit, it often means that borrowers may not qualify for the most favorable loan amounts, best credit terms, or top-tier credit cards.

Lenders often view fair credit as “subprime,” meaning there’s a higher perceived risk associated with lending to individuals in this category. This perception can translate into higher interest rates and less attractive terms on financial products. Therefore, a credit card designed for fair credit users aims to provide a pathway for credit improvement, offering access to credit while allowing cardholders to build a more positive payment history. Understanding this context is vital when evaluating whether a card like Fortiva aligns with your financial goals, particularly your aspiration to move into the “good” or “very good” credit tiers. Building credit requires consistent, responsible behavior over time, and the right financial tools can be instrumental in this process. To learn more about improving your credit score, you can read this detailed guide on how to boost your credit score.

Fortiva Credit Card: Key Features for Fair Credit Users

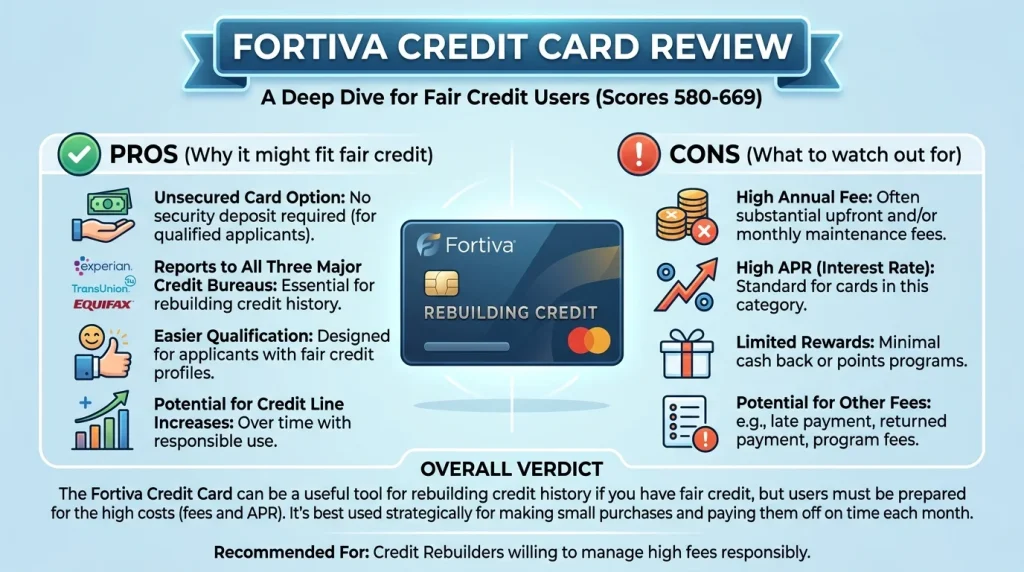

The Fortiva Credit Card, issued by The Bank of Missouri and serviced by Atlanticus, is positioned as an unsecured Mastercard specifically designed for individuals with fair to bad credit. Its primary appeal lies in the fact that it does not require a security deposit, a significant advantage over secured credit cards which necessitate an upfront cash deposit equal to the credit limit.

Key features that are frequently highlighted include:

- No Security Deposit: This is arguably the biggest selling point, as it removes a common barrier for many looking to establish or rebuild credit.

- Unsecured Credit: Unlike secured cards, the Fortiva card provides an unsecured credit line, offering more flexibility without tying up personal funds.

- Credit Reporting: Fortiva reports payment activity to all three major credit bureaus (Experian, Equifax, and TransUnion). This is crucial for credit building, as consistent, on-time payments contribute positively to a credit history.

- Pre-qualification: Applicants can often pre-qualify with a soft credit pull, which does not impact their credit score. This allows individuals to check their eligibility without risk. A hard inquiry is only performed if an offer is accepted.

- Cash Back Rewards: Some versions of the Fortiva Credit Card offer cash back rewards. For instance, cardholders may earn 3% cash back on eligible gas, grocery, and utility bill payments, and 1% on all other eligible purchases. However, these rewards are typically redeemed once a year as a statement credit.

- Mastercard Acceptance: As a Mastercard, the card is widely accepted at millions of locations both online and in physical stores.

- Fraud Liability Protection: Cardholders generally benefit from Mastercard Zero Liability Protection for unauthorized purchases.

The Pros of the Fortiva Credit Card

For individuals with fair credit, the Fortiva Credit Card offers several compelling advantages:

- Accessibility for Fair/Bad Credit: The most significant benefit is its willingness to approve applicants with credit scores in the fair to even bad range (often FICO 500-650). This makes it a viable option for those who have struggled to get approved for other unsecured cards.

- No Security Deposit: This eliminates the need to tie up personal funds, which is a common barrier for many seeking to establish or rebuild credit. For someone with limited savings, this can be a crucial factor.

- Credit Building Potential: By reporting to all three major credit bureaus, Fortiva provides a clear path to improving one’s credit score through responsible usage. Making consistent, on-time payments and keeping utilization low are fundamental steps to credit improvement.

- Pre-qualification with Soft Pull: The ability to check for pre-qualification without affecting your credit score is a valuable feature. This allows potential applicants to gauge their likelihood of approval before committing to a hard inquiry, which can temporarily lower a credit score.

- Cash Back Rewards: While modest and with redemption limitations, the availability of cash back rewards (up to 3% on certain categories) is a positive for a card aimed at this credit tier. Many cards for fair or poor credit offer no rewards at all.

- Mastercard Benefits: Being a Mastercard provides widespread acceptance and standard benefits like fraud liability protection.

Many users attest that the card provides a chance for those who have had issues in the past, making it a good tool for credit building.

The Cons and Potential Drawbacks of Fortiva

Despite its advantages, the Fortiva Credit Card comes with significant drawbacks that fair credit users must carefully consider. These often revolve around its fee structure and high interest rates, which can quickly erode any potential benefits if not managed meticulously.

- High Fees: This is perhaps the most frequently cited concern. Fortiva charges an annual fee, which can range from $49 to $175 in the first year, and then $0 to $49 annually thereafter. In addition to the annual fee, a monthly maintenance fee of $8 per month (approximately $96 per year) can apply after the first year. Some sources indicate an annual fee of $85-$175 first year, and $229 thereafter, along with monthly fees ranging from $5 to $12.50 after the first year. These combined fees can be substantial, making it an expensive card to carry.

- High APR: The Annual Percentage Rate (APR) for purchases on the Fortiva card is notably high, ranging from 22.74% to 36%. This means carrying a balance can quickly become very costly, potentially leading to a cycle of debt if payments are not managed diligently.

- Limited Credit Limits: While the card is unsecured, initial credit limits can be low. Some users report average limits around $851, with $300 being common, and a guaranteed minimum of $350 for approved applicants. High fees can also eat into the initial available credit, reducing actual purchasing power.

- Rewards Redemption Limitations: Although cash back rewards are offered, they can typically only be redeemed once per year as a statement credit, which offers less flexibility compared to other rewards programs.

- Additional Fees: The card may also include other fees such as a foreign transaction fee (3% of each transaction), cash advance fees (either $5 or 5% of the amount, whichever is greater), and late payment fees (up to $41). There can also be an additional card fee for authorized users.

- No Credit Limit Increase Requests: Cardholders generally cannot request a credit limit increase; Fortiva decides if and when an increase might be granted. This lack of control can be a disadvantage for those actively trying to improve their credit utilization ratio.

The overall cost of owning the Fortiva Credit Card can make it a less-than-ideal option for building credit inexpensively.

Fees, APR, and the True Cost of the Fortiva Card

To truly understand the value proposition of the Fortiva Credit Card for fair credit users, a detailed examination of its fee structure and APR is paramount. The information from various sources paints a consistent picture of a card with significant costs.

Here’s a breakdown of common fees and rates:

| Fee/Rate Type | Typical Range/Amount | Notes |

|---|---|---|

| Annual Fee (First Year) | $49 – $175 (some reports up to $85-$175) | Varies based on creditworthiness and specific offer. |

| Annual Fee (Ongoing) | $0 – $49 (some reports $49 or $229) | Can increase substantially after the first year in some cases. |

| Monthly Maintenance Fee | $0 first year, then $5 – $12.50 per month ($60 – $150 annually) | A significant ongoing cost, typically added in the second year. |

| Purchase APR | 22.74% – 36% (Variable) | Extremely high, making carrying a balance very expensive. |

| Cash Advance APR | Up to 36% | Similarly high, interest accrues from transaction date. |

| Late Payment Fee | Up to $41 | Standard penalty for missed payments. |

| Foreign Transaction Fee | 3% of each transaction | Costly for international use. |

| Additional Card Fee (Authorized User) | $19 (one-time or annual depending on offer) | Fee for adding another user to the account. |

The combination of an annual fee and a monthly maintenance fee can result in total yearly costs exceeding $150, particularly after the first year. For example, a $500 credit limit with a $49 annual fee and $96 in monthly fees means nearly 29% of your credit line is used by fees before you even make a purchase. This significantly reduces the effective credit available for actual spending and can negatively impact your credit utilization ratio, a key factor in credit scoring.

The high APR means that any balance carried month-to-month will accrue substantial interest charges, quickly increasing the total amount owed. For someone with fair credit looking to improve their financial situation, these high costs can be counterproductive if they are unable to pay off their balance in full each month. It underscores the importance of thoroughly reading the Schumer box and understanding the specific terms of any offer received, as fees can vary between applicants.

How Fortiva Impacts Credit Building for Fair Credit

The core purpose of many credit cards for fair or rebuilding credit is to help individuals improve their credit scores. The Fortiva Credit Card does offer mechanisms for this, but its effectiveness is heavily dependent on cardholder behavior and the overall cost structure.

Positive Impacts:

- Reporting to All Major Bureaus: Fortiva reports payment activity to Experian, Equifax, and TransUnion. Consistent, on-time payments are the most critical factor in building a positive credit history and improving credit scores.

- Unsecured Access: For those who cannot afford a security deposit, gaining access to an unsecured credit line can be a vital first step in establishing credit. This allows them to demonstrate responsible credit behavior without upfront cash.

Challenges to Credit Building:

- High Fees and Credit Utilization: As previously noted, the substantial annual and monthly fees can consume a significant portion of a low initial credit limit. This automatically inflates your credit utilization ratio (the amount of credit used compared to your total available credit), which can negatively impact your credit score. Lenders generally prefer a utilization ratio below 30%.

- High APR and Debt Trap: The very high APR means that if you carry a balance, the interest charges will quickly increase your debt. This can make it harder to pay down balances, potentially leading to increased utilization and missed payments, both of which are detrimental to credit scores.

For the Fortiva Credit Card to be an effective credit-building tool, users must be extremely disciplined. This means consistently paying the full statement balance every month to avoid interest charges and keeping spending well below the credit limit to maintain a low utilization ratio. If used responsibly, it can indeed help establish a positive payment history. However, for most people, the high fees make the math difficult, and cheaper alternatives often provide a more cost-effective path to credit improvement.

Comparing Fortiva with Alternatives for Fair Credit

Given the high costs associated with the Fortiva Credit Card, it’s essential for fair credit users to consider alternatives that might offer a more affordable or beneficial path to credit improvement. The market for fair credit cards includes both secured and unsecured options, often with varying fee structures and features. For a deeper understanding of various credit score ranges, consider exploring resources on the Consumer Financial Protection Bureau website.

Here’s a brief comparison with common alternatives:

- Secured Credit Cards:

- Example: OpenSky Secured Visa Credit Card. Many secured cards, like OpenSky, do not require a credit check for approval, making them highly accessible. While they require a refundable security deposit (e.g., $200), their fees are often much lower. OpenSky, for instance, has a $35 annual fee and no monthly maintenance fee. The deposit also serves as the credit limit. For many, the math favors secured cards because the deposit is refundable, whereas Fortiva’s fees are not.

- Benefit: Lower overall costs, often easier approval, and the security deposit is returned. They report to bureaus and effectively build credit.

- Drawback: Requires an upfront deposit, which not everyone can afford.

- Other Unsecured Cards for Fair Credit:

- Examples: Capital One Platinum Credit Card, Capital One QuicksilverOne Cash Rewards Credit Card, Avant Credit Card. Some unsecured cards for fair credit offer no annual fees or significantly lower annual fees than Fortiva. The Capital One Platinum, for instance, has no annual fee and helps build credit. The Capital One QuicksilverOne offers 1.5% cash back with a $39 annual fee, which can be more attractive if you spend enough to offset the fee.

- Benefit: No security deposit, potentially lower fees, and some may offer rewards or paths to credit limit increases.

- Drawback: May have stricter approval requirements than Fortiva or higher APRs.

- Retail Credit Cards:

- Benefit: Often easier to get approved for with fair credit, especially if you’re a regular customer. Can help build credit history with responsible use.

- Drawback: Typically have high APRs and are limited to purchases within a specific store or brand.

For individuals with fair credit, exploring options like the Capital One Platinum or a reputable secured card often presents a more financially sound strategy for credit building due to lower costs and clearer pathways to graduation or better terms.

Application Process and Eligibility for the Fortiva Card

The application process for the Fortiva Credit Card is designed to be user-friendly, primarily conducted online. Here’s what potential applicants can expect:

- Pre-qualification: Fortiva offers a pre-qualification process that involves a soft credit inquiry. This allows you to see if you’re likely to be approved without affecting your credit score. If you receive a mail offer, it usually means your chances of approval are high.

- Formal Application: If you accept a pre-qualified offer, you will proceed with a formal application. This step typically triggers a hard credit inquiry, which can have a minor, temporary impact on your credit score.

- Eligibility Requirements: Common requirements usually include being at least 18 years of age, having legal residency in the application region, possessing a valid government-issued identification number, and demonstrating a stable source of income sufficient to cover monthly obligations. Income verification through access to your bank account information may also be required.

- Credit Score Range: While aimed at fair to bad credit, approval is common for FICO scores between 500 and 650. However, meeting eligibility criteria does not guarantee final approval.

It’s worth noting that, according to some recent reports, the Fortiva Credit Card might not currently be accepting new applicants for certain versions of the card, suggesting that availability can change. However, Fortiva continues to offer various credit solutions. Always check the most current information directly from Fortiva or trusted financial review sites before applying.

Conclusion: Is Fortiva the Right Choice for Your Fair Credit Journey?

The Fortiva Credit Card is a legitimate unsecured credit card option, primarily aimed at individuals with fair to bad credit who are looking to rebuild their financial standing. Its main allure is the ability to obtain an unsecured credit line without a security deposit and its reporting to all three major credit bureaus, which is essential for credit building.

However, the significant drawbacks, particularly the high annual fees, monthly maintenance fees, and exceptionally high APR, make it a costly card to carry. These fees can quickly diminish a low initial credit limit and make carrying a balance financially detrimental, potentially hindering rather than helping credit improvement if not managed with extreme discipline.

For fair credit users who are diligent about paying their balance in full every month and keeping utilization low, Fortiva can serve as a stepping stone. The modest cash back rewards on certain categories offer a minor perk that some alternative cards in this tier might lack.

Yet, for most, there are often more affordable and arguably more effective credit-building alternatives available, such as secured credit cards with lower fees or other unsecured cards designed for fair credit with more favorable terms. It is crucial for prospective applicants to carefully weigh the benefits of unsecured access against the substantial costs and to consider whether they can consistently manage the card to avoid incurring expensive interest and fees. Always read the fine print of any specific offer you receive to understand the exact terms and conditions. While Fortiva offers a chance, it demands careful consideration to ensure it aligns with your long-term financial health and credit-building objectives.