7 Powerful Mission Lane Card Facts – Build Credit Without a Deposit

Table of Contents

Mission Lane Credit Card products have emerged as a notable option for individuals seeking to build or rebuild their credit history. In a financial landscape where access to credit can be challenging for those with less-than-perfect credit scores, Mission Lane aims to provide a clear and accessible pathway. This comprehensive review and credit building guide will delve into the various aspects of Mission Lane credit cards, examining their features, benefits, potential drawbacks, and how they can be effectively utilized to improve your financial standing. We’ll explore who these cards are best suited for, the application process, associated fees, and how responsible usage can lead to a healthier credit profile.

Introduction to Mission Lane Credit Cards

Mission Lane is a financial technology company that partners with banks like Transportation Alliance Bank and WebBank to issue Visa credit cards. Their primary focus is on helping consumers establish or rebuild credit through transparent pricing and a user-friendly experience. Unlike many traditional lenders, Mission Lane specifically targets individuals with bad to fair credit scores, or those with limited credit history, who might otherwise struggle to get approved for an unsecured credit card. The company emphasizes a dignified customer experience and leverages technology and data analytics to provide accessible financial products. With over 3 million members, Mission Lane has grown significantly as a credit-building solution.

Who Are Mission Lane Credit Cards For?

Mission Lane credit cards are primarily designed for individuals who are in the process of building or rebuilding their credit. This includes:

- Individuals with Limited or No Credit History: Many young adults or newcomers to the credit system find it difficult to obtain their first credit card. Mission Lane offers an entry point to establish a credit file.

- Those with Bad or Poor Credit: For consumers who have experienced financial setbacks, such as missed payments or previous bankruptcies, Mission Lane can provide a second chance to demonstrate responsible credit behavior and improve their credit scores. The average credit score for members who have matched with Mission Lane Silver Line Visa or similar cards is around 599, with 572 being the most common. For the Mission Lane Secured Visa, the average credit score is 577, with 547 being common.

- Consumers Who Want to Avoid a Security Deposit: Several Mission Lane cards, particularly the Green Line and Silver Line Visa, are unsecured, meaning they do not require an upfront security deposit. This can be a significant advantage for those who cannot or prefer not to tie up funds in a secured card.

However, it’s important to note that while Mission Lane is accessible, individuals with good credit scores might find cards with more extensive rewards programs and lower APRs elsewhere.

Mission Lane Credit Card Options: Unsecured, Secured, Green Line, Silver Line, and Gold Line

Mission Lane offers a few different credit card products tailored to various credit-building needs, categorized primarily into unsecured and secured options, with distinct lines offering different benefits.

Unsecured Mission Lane Cards

The core offerings from Mission Lane are generally unsecured credit cards, which means they do not require a security deposit. These are often preferred by individuals who want to avoid tying up their cash.

- Mission Lane Green Line Visa: This is a no-frills, unsecured credit-building card designed for individuals with bad to fair credit. It typically has a starting credit limit of at least $300, and some cardholders report limits as high as $2,000 to $3,000. The annual fee can range from $0 to $59, depending on the applicant’s credit profile. This card aims to provide a straightforward path to credit improvement without the need for a deposit.

- Mission Lane Silver Line Visa: Similar to the Green Line, the Silver Line Visa is also an unsecured card that does not require a security deposit. A key distinguishing feature for the Silver Line Visa is the offer of unlimited 1.5% cash back on every purchase. This makes it a more attractive option for those who want to build credit while also earning some rewards. It also typically has a starting credit line up to $3,000 and can come with no annual fee.

- Mission Lane Gold Line Visa: The Gold Line Visa appears to be a premium unsecured option within Mission Lane’s portfolio, offering enhanced rewards. It boasts unlimited 3% cash back on gas, travel, and dining, plus 1% on all other purchases. This card also advertises a starting credit line up to $3,000 and no annual fee, along with no foreign transaction fees.

Secured Mission Lane Card

For those who may not qualify for an unsecured card or prefer the structure of a secured card, Mission Lane also offers a secured option.

- Mission Lane Secured Visa Credit Card: This card requires an upfront cash deposit, which typically becomes your credit limit. The minimum deposit can be as low as $200. Secured cards are often easier to get approved for, especially for individuals with very low credit scores, and the deposit serves as collateral for the lender. As with other Mission Lane cards, responsible use is reported to credit bureaus to help build credit.

Key Features and Benefits of Mission Lane Credit Cards

Mission Lane credit cards, while primarily focused on credit building, offer several features designed to support users on their financial journey.

- No Security Deposit (for unsecured cards): A major draw of the Green Line, Silver Line, and Gold Line Visa cards is the absence of a security deposit, which can be a barrier for many seeking credit.

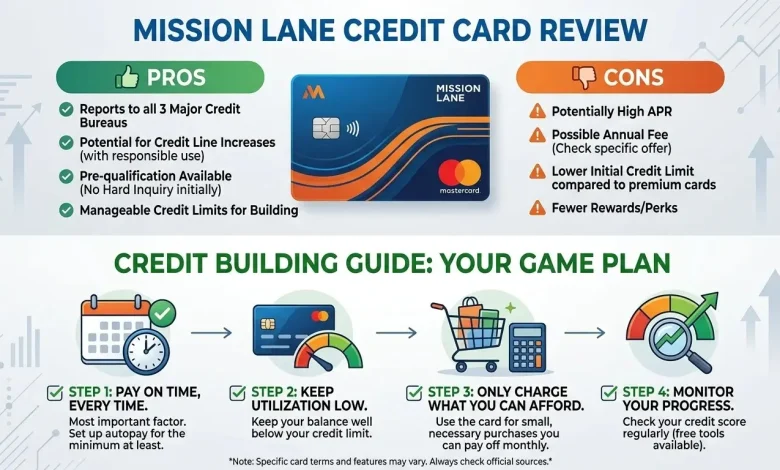

- Credit Building Focus: All Mission Lane cards report payment activity to the three major credit bureaus (Equifax, Experian, and TransUnion). Consistent on-time payments and responsible usage are crucial for improving credit scores.

- Opportunity for Credit Limit Increases: Mission Lane reviews accounts for potential credit limit increases, often automatically, after demonstrating responsible usage for several months (e.g., as soon as seven months). A higher credit limit can positively impact your credit utilization ratio, a key factor in credit scoring.

- Prequalification with No Credit Impact: Mission Lane allows applicants to check if they prequalify for a card without a hard inquiry on their credit report, meaning it won’t affect their credit score. This allows potential cardholders to gauge their approval odds risk-free.

- Mobile App and Financial Education Tools: Mission Lane provides a mobile app for easy account management, tracking payments, and accessing financial education tools. The app generally receives positive feedback for its user-friendliness.

- Cash Back Rewards (Silver Line and Gold Line): The Silver Line Visa offers unlimited 1.5% cash back on all purchases, while the Gold Line offers 3% on gas, travel, and dining, plus 1% on all other purchases. This is a valuable perk for credit-building cards, which often come with no rewards.

- Transparent Fees: The company aims for transparent pricing and generally avoids hidden fees common with some subprime cards.

- Basic Visa Benefits: Cardholders receive standard Visa benefits such as $0 fraud liability and 24-hour customer service.

Applying for a Mission Lane Credit Card: What to Expect

The application process for a Mission Lane credit card is generally straightforward, beginning with a prequalification step.

- Prequalification: You can check for prequalification online, which involves a soft credit pull and will not impact your credit score. This step helps you understand your approval odds and the potential terms, including the annual fee, before a formal application.

- Eligibility Requirements: To apply, you typically need to be at least 18 years old, have a Social Security number or International Tax Identification Number, and sufficient income to make monthly payments. You will also need a physical U.S. address (excluding certain states like Maine, Maryland, Nevada, North Dakota, and West Virginia).

- Formal Application: If you prequalify and decide to proceed, you will complete a formal application. This usually involves a hard credit inquiry, which may temporarily affect your credit score by a few points.

- Information Required: You will need to provide your street address, Social Security number, income information, an active phone number, and an active email address. Mission Lane also complies with the USA PATRIOT Act, requiring identity verification to prevent fraud.

- Approval and Credit Limit: Upon approval, your initial credit limit will be determined based on your credit profile and history. Starting limits commonly range from $300 to $2,000, with some users reporting limits as high as $3,000 to $4,000 for the Silver Line and Gold Line cards.

While prequalification increases your approval odds, it does not guarantee approval. Applicants with recent bankruptcies or current delinquencies may still face denial.

Fees, APRs, and Other Costs Associated with Mission Lane

Understanding the costs associated with any credit card is crucial, especially for those building credit. Mission Lane cards come with various fees and interest rates that users should be aware of.

| Fee/Rate Type | Mission Lane Green Line Visa | Mission Lane Silver Line Visa | Mission Lane Gold Line Visa | Mission Lane Secured Visa |

|---|---|---|---|---|

| Annual Fee | $0 – $59 (variable) | $0 (may vary by offer) | $0 | $0 – $59 (variable) |

| Purchase APR (Variable) | 19.99% – 33.99% | Up to 33.99% | Not explicitly stated, but generally high for credit-building cards | 19.99% – 33.99% |

| Cash Advance APR (Variable) | 19.99% – 33.99% | Same as Purchase APR (generally high) | Not explicitly stated, but generally high | 19.99% – 33.99% |

| Foreign Transaction Fee | 3% | 3% | 0% | Not explicitly stated, but generally 3% for Visa |

| Late Payment Fee | Up to $41 (or up to $35 depending on terms) | Up to $41 | Up to $41 (assumed) | Up to $41 (assumed) |

| Security Deposit | None | None | None | Required (minimum $200) |

The variable APRs, ranging from approximately 19.99% to 33.99%, are a critical point to consider. These rates are high, which means carrying a balance can quickly become expensive due to accumulating interest. Mission Lane explicitly states that if you are charged interest, the charge will be no less than $0.50. The annual fee can vary by card and individual credit profile. While some offers might be $0 annual fee, others can be up to $59. It’s essential to check the specific terms of your offer during the prequalification stage.

How Mission Lane Helps You Build Credit

The primary purpose of Mission Lane credit cards is to facilitate credit building or rebuilding. They achieve this through several key mechanisms:

- Reporting to All Three Major Credit Bureaus: Mission Lane consistently reports your account activity—including payments, balances, and credit limits—to Equifax, Experian, and TransUnion every month. This consistent reporting is fundamental for establishing a credit history and allowing credit bureaus to calculate your credit score.

- Establishing a Revolving Credit Account: A credit card is a type of revolving credit, which is an important component of a healthy credit mix. By managing a Mission Lane card responsibly, you demonstrate your ability to handle different types of credit.

- Credit Limit Increases: After a period of responsible use (often as soon as seven months), Mission Lane automatically reviews accounts for credit limit increases. A higher credit limit, combined with keeping your balance low, improves your credit utilization ratio, which is a significant factor in credit scoring. For example, if your credit limit increases from $300 to $600 and you continue to spend $100, your utilization drops from 33% to 16.7%. Generally, keeping utilization below 30% is recommended.

- Encouraging On-Time Payments: The structure of the card and its reporting practices incentivize making payments on time, which is the most crucial factor in credit score calculations.

- Credit Builder Account Program: Beyond credit cards, Mission Lane also offers a Credit Builder Account program. This program, offered through TAB Bank, allows consumers to take out a small loan ($25 per month for a year) that is deposited into a secured savings account. Repaying this loan builds positive payment history, which is reported to at least one major credit bureau, while simultaneously building savings. This is an excellent option for those who might not qualify for a credit card immediately.

To effectively build credit with a Mission Lane card, it is essential to make all payments on time and in full whenever possible, and to keep your credit utilization low. Consistently maintaining good habits can lead to noticeable credit score improvements within 6-12 months. For further understanding of how credit scores work and how to improve them, resources like Wikipedia’s article on Credit Score can provide valuable insights into the underlying principles of credit reporting and scoring.

Pros and Cons of Mission Lane Credit Cards

Like any financial product, Mission Lane credit cards come with their own set of advantages and disadvantages.

Pros:

- Accessibility for Poor/Limited Credit: Mission Lane is genuinely accessible to individuals with limited or bad credit, providing an opportunity to build a credit history where other lenders might decline.

- No Security Deposit for Unsecured Cards: This is a significant benefit, as it removes the barrier of tying up personal funds, making it easier for many to get started.

- Reports to All Three Bureaus: Consistent reporting to Equifax, Experian, and TransUnion is vital for comprehensive credit building.

- Opportunity for Credit Limit Increases: Automatic reviews for credit limit increases reward responsible behavior and help improve credit utilization.

- Prequalification with Soft Pull: The ability to check for prequalification without affecting your credit score is a consumer-friendly feature.

- Cash Back Rewards: The Silver Line and Gold Line cards offer valuable cash back rewards, a rarity for credit-building cards.

- Transparent Fees: Many users appreciate the straightforward fee structure and lack of unexpected charges.

- User-Friendly Mobile App: The app allows for easy account management and payment tracking.

Cons:

- High Variable APRs: The interest rates are quite high (often 19.99% – 33.99%), making it expensive to carry a balance month-to-month. It is imperative to pay balances in full to avoid significant interest charges.

- Potential Annual Fee: While some offers are $0 annual fee, others can charge up to $59, which is an added cost, especially for a card with limited perks beyond credit building. The specific fee is determined by your credit profile.

- Low Starting Credit Limits: Initial credit limits can be as low as $300, which might feel restrictive for some users and can make it challenging to maintain a low credit utilization ratio if not managed carefully.

- No Manual Credit Limit Increase Requests: While automatic reviews occur, cardholders cannot manually request a credit limit increase, which can be frustrating for those making significant progress.

- Limited Additional Perks: Beyond the cash back on certain cards, Mission Lane cards generally lack extensive benefits or rewards programs found with cards for higher credit tiers.

- Mixed Customer Service Reviews: While many users report positive experiences, some customer reviews mention issues with payment processing, fraudulent transactions, or unhelpful customer service representatives.

Alternatives to Mission Lane for Credit Building

While Mission Lane offers a viable path for credit building, it’s always wise to compare options. Depending on your credit situation and preferences, other credit cards might be more suitable.

- Secured Credit Cards: Often considered the safest bet for those at the very bottom of the credit barrel (FICO score under 500), secured cards like the OpenSky Secured Visa Credit Card or the Discover it® Secured Credit Card are easier to get approved for and typically refund your deposit upon graduation to an unsecured card or account closure. Many secured cards also offer rewards and no annual fees, making them potentially more cost-effective than some Mission Lane unsecured cards with fees.

- Capital One Platinum Credit Card: This card is another popular unsecured option for building credit. It offers similar features to Mission Lane but might have a more straightforward application process for some.

- Capital One QuicksilverOne Cash Rewards Credit Card: If you’re looking to build credit and earn rewards, this card offers 1.5% cash back on every purchase with a moderate annual fee, making it a strong contender for those with fair credit.

- Petal® 2 Visa® Credit Card: This card is marketed as a quality starter credit card with strong perks and could be a good fit for those new to credit.

- Credit One Bank® Platinum Visa® for Rebuilding Credit: This card offers 1% cash back on eligible purchases and provides opportunities for credit line increases, similar to Mission Lane.

- Self Visa® Credit Card: The Self Visa Credit Card takes a different approach by combining a credit builder loan with a secured credit card. You make payments into a credit builder account, and once enough savings are accumulated, these funds can secure a Visa card. This method creates two tradelines, which can be beneficial for your credit mix.

- Store Cards: Some store cards are easier to qualify for with bad credit, but it’s crucial to evaluate their terms, fees, and credit-building benefits carefully, as some can have very high interest rates and few advantages.

When considering alternatives, pay close attention to annual fees, APRs, credit limit increase policies, and whether a security deposit is required. It’s often recommended to start with a secured card if your credit is very poor, as they generally have lower costs and a clearer path to credit improvement.

Conclusion

Mission Lane credit cards present a viable and often accessible option for individuals striving to build or rebuild their credit. Their unsecured offerings, particularly the Green Line and Silver Line Visa, appeal to those who wish to avoid a security deposit while establishing a positive payment history. The inclusion of cash back rewards on the Silver Line and Gold Line cards adds a desirable perk not commonly found in the credit-building card segment. With consistent reporting to all three major credit bureaus and periodic opportunities for credit limit increases, Mission Lane cards can effectively serve as a stepping stone to a stronger financial future.

However, prospective cardholders must be diligent about managing their accounts. The high variable APRs necessitate paying off balances in full each month to avoid accumulating substantial interest charges. While the potential for an annual fee is a consideration, its range is often competitive for subprime cards. For those with very poor credit, or those prioritizing the return of a deposit, a secured credit card might offer a more cost-effective or structured path. Ultimately, the Mission Lane Credit Card can be a powerful tool for credit improvement when used responsibly, demonstrating consistent on-time payments and maintaining low credit utilization. It’s a solid choice for individuals committed to taking control of their financial journey and moving towards better credit opportunities.