7 Best Starter Credit Cards for Beginners – Build Credit & Earn Rewards

Table of Contents

Credit Card for Beginners: Entering the world of credit cards can feel both exciting and daunting. For many, a credit card represents a significant step towards financial independence, offering convenience, building credit history, and even providing rewards. However, without proper understanding and responsible usage, it can also lead to financial pitfalls. This comprehensive guide aims to demystify credit cards for those new to them, comparing the best starter card options and equipping you with the knowledge to make informed decisions and build a strong financial foundation. Choosing the right first credit card and using it wisely is a crucial step in establishing your creditworthiness, which impacts future financial endeavors from loans to housing.

Understanding the Fundamentals: What is a Credit Card?

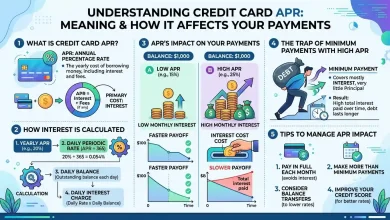

At its core, a credit card is a financial tool that allows you to borrow money from a financial institution (the issuer) to make purchases, with the agreement that you will repay the borrowed amount, usually with interest, at a later date. Unlike a debit card, which draws funds directly from your bank account, a credit card extends a line of credit. When you’re approved for a credit card, the issuer sets a “credit limit,” which is the maximum amount you can charge to the card. Each month, you’ll receive a statement detailing your purchases, payments, and any fees incurred during the “billing cycle.” You are required to make at least a “minimum payment” by the due date. If you pay the “statement balance” in full by the due date, you generally won’t owe any “interest” on your purchases due to a “grace period.” However, if you carry a balance, interest will be applied to the unpaid amount, calculated based on the card’s “Annual Percentage Rate” (APR). This makes understanding how credit cards work essential for responsible management and avoiding unnecessary costs.

The Pros and Cons: Weighing the Benefits and Risks of Your First Credit Card

For beginners, understanding both the advantages and disadvantages of credit cards is paramount. Used wisely, a credit card can be a powerful financial asset. Mismanaged, it can lead to significant debt and negatively impact your financial health.

Benefits of a Credit Card for Beginners

- Building Credit History: One of the most significant benefits for beginners is the ability to establish and build a credit history and credit score. A good credit score is vital for future financial goals, such as securing loans for a car or home, renting an apartment, or even getting better insurance rates. Consistent, on-time payments and responsible use contribute positively to your credit report, demonstrating to lenders that you are a reliable borrower.

- Convenience and Ease of Use: Credit cards offer a convenient way to make purchases without carrying large amounts of cash. They are widely accepted online and in physical stores, making transactions seamless, especially for travel or online shopping.

- Fraud Protection: Credit cards generally offer robust fraud protection, safeguarding you from unauthorized charges if your card is stolen or used fraudulently. Many issuers offer zero-liability policies, limiting your responsibility for fraudulent activity.

- Emergency Fund: A credit card can serve as a financial backup for unexpected expenses, like car repairs or medical bills, providing a safety net when cash reserves are low.

- Rewards and Perks: Many credit cards offer rewards programs, such as cashback, points, or airline miles, on eligible purchases. While beginners’ cards might have less generous rewards, they can still provide a small return on your everyday spending.

- Record Keeping: Credit card statements provide an easy-to-track record of your spending, which can be helpful for budgeting and financial management.

Potential Risks for New Cardholders

- Debt Accumulation: The primary risk of credit cards is the temptation to overspend and accumulate debt, especially if you treat the card like “free money.” High balances, particularly if only minimum payments are made, can quickly spiral due to high interest rates, making it difficult to pay off the debt.

- High Interest Rates and Fees: Credit cards, especially starter cards, often come with relatively high APRs. If you carry a balance, the interest charges can significantly increase the cost of your purchases. Additionally, various fees like annual fees, late payment fees, and foreign transaction fees can add to the overall cost if not managed carefully.

- Damage to Credit Score: Irresponsible use, such as missed or late payments, exceeding your credit limit, or constantly carrying high balances, can severely damage your credit score. This negative impact can hinder your ability to secure future loans or other financial products.

- Complexity: The various terms, conditions, and fee structures associated with credit cards can be complex and overwhelming for beginners. It’s crucial to read and understand the fine print to avoid surprises.

Choosing Your First Credit Card: Key Factors to Consider

Selecting the right first credit card is crucial for setting yourself up for financial success. There isn’t a one-size-fits-all answer, as the best card depends on your personal financial situation and goals. Here are the key factors beginners should evaluate:

Annual Percentage Rate (APR)

The APR is the interest rate you’ll pay on any balance you carry over from month to month. For beginners, APRs can be higher, making it even more important to aim to pay your balance in full each month to avoid interest charges. Some cards offer introductory 0% APR periods, but these are often temporary and can revert to a high rate after the promotional period. Focusing on cards with no or low annual fees is often a better strategy for first-time users.

Fees to Watch Out For

Be aware of various fees that can erode your financial health.

- Annual Fee: This is a yearly charge for simply having the card. Many excellent starter cards have no annual fee, which is ideal for beginners.

- Late Payment Fees: Missing a payment due date will almost certainly result in a late fee and can negatively impact your credit score.

- Foreign Transaction Fees: If you plan to use your card abroad, look for cards that don’t charge a fee for transactions made in foreign currencies, typically 2-3% of the transaction amount.

- Cash Advance Fees: Avoid using your credit card for cash advances, as they typically come with high fees and interest accrues immediately.

Credit Limit and Credit Utilization

Your credit limit is the maximum amount you can borrow. For beginners, credit limits are often lower, typically a few hundred to a few thousand dollars. More important than the limit itself is your “credit utilization ratio,” which is the amount of credit you’re using compared to your total available credit. Lenders prefer to see this ratio kept below 30% (e.g., if your limit is $1,000, keep your balance under $300). A low utilization ratio signals responsible credit management and can positively impact your credit score.

Rewards Programs

While attractive, rewards should be a secondary consideration for a beginner’s card. Focus on cards that help you build credit responsibly with low fees first. Simple cash-back cards are generally good options, offering a percentage back on all purchases or specific categories. Ensure that any rewards earned do not encourage overspending.

Credit Reporting

A crucial feature for any starter card is that it reports your payment activity to all three major credit bureaus: Experian, Equifax, and TransUnion. This is how your responsible use translates into building a credit history and score. If a card doesn’t report to all three, its effectiveness in helping you build comprehensive credit is limited.

Types of Starter Credit Cards: A Detailed Comparison

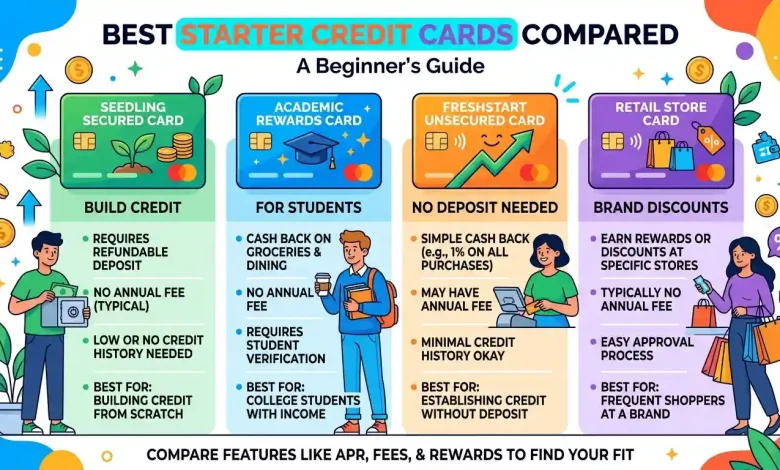

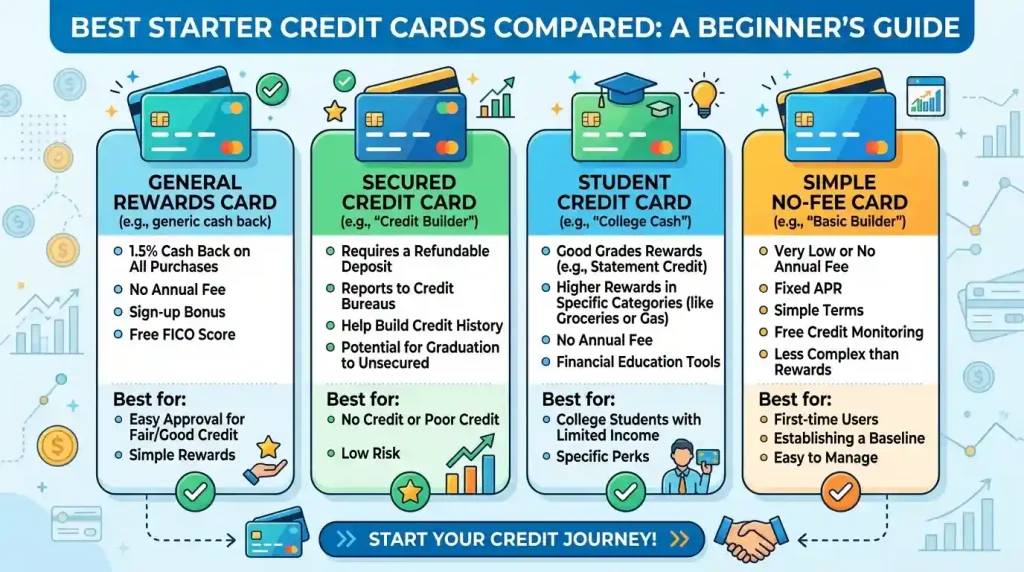

For individuals with no or limited credit history, specific types of credit cards are designed to facilitate credit building. These “starter cards” often have different requirements and features tailored to new users.

- Secured Credit Cards: Often considered the best choice for those with no credit history, a secured credit card requires a refundable security deposit, typically equal to your credit limit. This deposit acts as collateral, minimizing risk for the issuer and making them easier to get approved for. Secured cards function much like unsecured cards, reporting your payment activity to credit bureaus and helping you build a positive credit history. Many secured cards offer a path to an unsecured card and a refund of your deposit after a period of responsible use.

- Student Credit Cards: These cards are specifically designed for college students, recognizing that they often have limited income and no credit history. Student cards are typically easier to qualify for than standard unsecured cards and may offer student-friendly rewards or lower interest rates. They serve as an excellent tool for students to begin building credit while in school.

- Unsecured Starter Cards (or Credit-Builder Cards): Some issuers offer traditional unsecured credit cards specifically for individuals with limited or fair credit. These cards do not require a security deposit but may come with lower credit limits and higher APRs compared to cards for those with established credit. They can be a good option if you don’t want to tie up a deposit, but approval can be slightly more challenging than for secured cards.

- Authorized User Status: While not a credit card you apply for independently, becoming an authorized user on a parent’s or trusted family member’s credit card can be an effective way to begin building credit. Your credit report will reflect the primary cardholder’s responsible payment history, as long as they manage the account well. This allows you to benefit from their good credit practices without the full responsibility of a primary account. However, it’s crucial that the primary cardholder is financially responsible, as their missteps can also affect your credit.

- Retail Store Cards: These cards are often easier to obtain for beginners, but they are typically limited to purchases at a specific retailer and may come with higher interest rates. While they can offer discounts at that store, they are generally not the best choice for initial credit building due to their limited utility and potentially high costs.

Here’s a comparison of the main types of starter credit cards:

| Card Type | Security Deposit Required? | Ease of Approval for Beginners | Typical Credit Limit | Main Benefit for Beginners | Common Drawbacks |

|---|---|---|---|---|---|

| Secured Credit Card | Yes (Refundable) | Very Easy (High approval chance with no credit) | Equal to Deposit (e.g., $200-$2,500) | Guaranteed path to building credit safely | Requires upfront cash, limited initial credit |

| Student Credit Card | No | Easy (Designed for students with limited income/credit) | Often Low ($500-$1,500) | Build credit without deposit, student-friendly rewards | Requires student status, limits may be low |

| Unsecured Starter Card | No | Moderate (May require some credit history or fair credit) | Often Low ($300-$1,000) | Build credit without deposit, potential for graduation to better cards | Harder to qualify for than secured, higher APRs typical |

| Authorized User Status | No | Immediate (No application needed) | Inherits primary card’s limit | Builds credit without direct responsibility | Dependent on primary cardholder’s responsibility |

| Retail Store Card | No | Easy (Often offered at point-of-sale) | Varies | Discounts at specific store | Limited use, often high APR, may not report to all bureaus |

Building a Strong Credit History: Best Practices for Beginners

Once you’ve chosen your first credit card, the real work of building a positive credit history begins. Responsible usage is key. Here are essential practices to follow:

- Make On-Time Payments, Every Time: Your payment history is the single most important factor in your credit score, accounting for about 35% of your FICO score. Missing a payment can severely damage your credit. Set up automatic payments or calendar reminders to ensure you never miss a due date.

- Keep Your Credit Utilization Ratio Low: Aim to keep your credit card balance below 30% of your available credit limit. For optimal credit building, keeping it under 10% is even better. If your credit limit is $500, try to keep your balance below $150. Paying off your balance in full each month is the best way to maintain a low utilization ratio and avoid interest.

- Pay Your Balance in Full (If Possible): While making the minimum payment keeps your account in good standing, paying your full statement balance each month allows you to avoid interest charges entirely and is the fastest way to build positive credit. Treat your credit card like a debit card, only spending what you can afford to pay back immediately.

- Don’t Close Old Accounts: The length of your credit history also impacts your score (about 15%). Your first credit card will likely become your oldest account, so keeping it open, even if you don’t use it frequently, helps maintain a longer credit history.

- Monitor Your Account Activity: Regularly check your credit card statements and online account for any unauthorized transactions or errors. Setting up alerts can help you catch unusual activity promptly.

- Be Wary of Multiple Applications: While it’s tempting to apply for several cards, each application results in a “hard inquiry” on your credit report, which can temporarily lower your score. Focus on one or two starter cards and allow time for your credit to grow.

- Regularly Check Your Credit Report: You are entitled to a free credit report from each of the three major credit bureaus annually. Review these reports for accuracy and to identify any potential fraud. This helps you understand your credit health and dispute any errors. You can learn more about managing your credit and understanding credit reports through official government resources such as the Consumer Financial Protection Bureau.

Common Credit Card Terminology: A Glossary for New Users

Navigating the credit card landscape requires familiarity with common terms. Understanding these will empower you to make more informed decisions.

- Annual Fee: A yearly charge for having a credit card account. Many starter cards aim for $0 annual fees.

- Annual Percentage Rate (APR): The yearly interest rate charged on any unpaid balance that carries over from month to month.

- Balance: The total amount of money you owe on your credit card at any given time.

- Billing Cycle: The period of time (usually 28-31 days) between statement closing dates. All purchases, payments, and fees made during this period appear on your statement.

- Cash Advance: Withdrawing cash using your credit card. This typically incurs high fees and interest begins accruing immediately.

- Credit Bureau (or Credit Reporting Agency): Companies that collect and maintain your credit history, including Experian, Equifax, and TransUnion.

- Credit Limit: The maximum amount you are allowed to charge on your credit card.

- Credit Score: A three-digit number that summarizes your creditworthiness, based on information in your credit report. Lenders use it to assess risk.

- Credit Utilization Ratio: The amount of credit you are currently using compared to your total available credit. Keeping this ratio low is good for your credit score.

- Due Date: The date by which your credit card payment must be received by the issuer to avoid late fees and negative credit reporting.

- Grace Period: The time between the end of your billing cycle and your payment due date, during which no interest is charged on new purchases if you pay your full statement balance.

- Interest: The cost of borrowing money, charged as a percentage of your outstanding balance if you don’t pay in full.

- Minimum Payment: The smallest amount you must pay by the due date to keep your account in good standing.

- Statement Balance: The total amount owed on your credit card as of the closing date of your billing cycle.

Conclusion: Laying the Foundation for a Healthy Financial Future

Starting with your first credit card is an important financial milestone that, when approached thoughtfully, can pave the way for a strong financial future. By understanding what a credit card is, weighing its pros and cons, carefully considering factors like APR and fees, and choosing the right type of starter card for your situation, you are already on the right track. Remember that responsible usage—especially making on-time payments and keeping credit utilization low—is paramount to building a healthy credit history. Take the time to educate yourself on credit card terminology and continuously monitor your financial health. With careful management and a commitment to responsible habits, your first credit card will serve as a valuable tool, unlocking greater financial opportunities and helping you achieve your long-term goals.