7 Shocking Aspire Card Truths – Better Credit Building Alternatives

Table of Contents

Aspire Credit Card, specifically the Aspire® Cash Back Rewards Mastercard, stands as a notable option for individuals looking to build or rebuild their credit history. In the complex landscape of personal finance, establishing good credit is paramount for unlocking various opportunities, from securing loans at favorable rates to renting an apartment or even getting certain jobs. For those with less-than-perfect credit, navigating the world of credit cards can be challenging, often requiring security deposits or facing high fees and restrictive terms. The Aspire Credit Card aims to bridge this gap, offering an unsecured credit card designed for individuals with bad or fair credit, generally defined as a FICO score of 300 or higher, or below 640.

This comprehensive review will delve into the intricacies of the Aspire Credit Card, exploring its features, benefits, potential drawbacks, and how it can serve as a tool for credit improvement. Furthermore, we will provide actionable credit-building tips that, when combined with responsible use of a card like Aspire, can pave the way to a healthier financial future. Understanding how to leverage such a card effectively, coupled with sound financial habits, is crucial for anyone on the journey to creditworthiness.

Introduction to the Aspire Credit Card

The Aspire Credit Card, primarily offered as the Aspire® Cash Back Rewards Mastercard, is an unsecured credit card tailored for consumers with bad or limited credit history. Unlike secured credit cards, which require an upfront security deposit to establish a credit limit, the Aspire card provides a credit line without this initial capital outlay. This makes it an attractive option for those who may not have several hundred dollars readily available for a deposit but still need a mechanism to start building credit. Issued by The Bank of Missouri, the Aspire Mastercard is accepted wherever Mastercard is, offering broad usability for everyday purchases.

The card is particularly marketed towards individuals who have struggled with credit in the past or are new to credit altogether, providing a pathway to demonstrate responsible financial behavior. Its primary utility lies in its ability to report payment activity to all three major credit bureaus—Equifax, Experian, and TransUnion. Consistent, on-time payments reported to these bureaus are fundamental to improving one’s credit score over time. However, it’s important for prospective cardholders to thoroughly understand its terms, conditions, and fee structure to determine if it aligns with their financial goals and capacity for responsible management.

Key Features and Benefits of the Aspire Credit Card

The Aspire Credit Card comes with several features designed to appeal to its target audience: individuals seeking to build or rebuild credit. Understanding these features is key to maximizing the card’s potential benefits.

- No Security Deposit Required: One of the most significant advantages of the Aspire Mastercard is that it is an unsecured card, meaning no upfront security deposit is needed. This removes a common barrier for many people with poor credit who may not have the funds for a deposit.

- Cash Back Rewards: The card offers cash back rewards, specifically 3% cash back on eligible gas, grocery purchases, and utility bill payments, and 1% cash back on all other eligible purchases. This reward structure can help offset some of the card’s associated costs if utilized strategically for everyday spending.

- Accessibility for Bad Credit: Aspire accepts applicants with bad credit, often defined as a FICO score of 300 or higher, or generally below 640. This broadens access to credit for those who might be denied by traditional credit card issuers.

- Credit Reporting to All Three Bureaus: Crucially, Aspire reports account activity to Equifax, Experian, and TransUnion. This comprehensive reporting is vital for building a positive credit history across the board, which is essential for improving one’s overall credit score.

- Prequalification Option: Aspire offers a prequalification tool that allows potential applicants to check their approval odds without affecting their credit score. This “soft pull” on their credit report gives applicants an idea of their eligibility before committing to a full application, which would involve a “hard pull” that can temporarily ding their score.

- Credit Limit Potential: Approved applicants may receive credit limits up to $1,000, with a guaranteed minimum of at least $350. The exact limit depends on creditworthiness and income.

- Additional Benefits: Depending on the specific Aspire card product (e.g., Aspire Protect Mastercard), cardholders may also receive benefits such as cell phone protection, 24-hour roadside assistance, and identity theft expense reimbursement coverage. The standard Aspire card also offers zero fraud liability and a free monthly credit score viewable after 60 days of account opening.

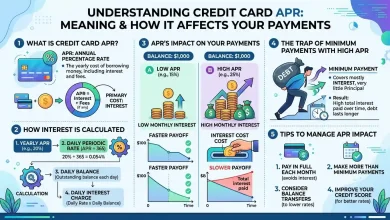

Understanding Aspire’s Fees and Interest Rates

While the Aspire Credit Card offers pathways to credit building, it’s essential to be aware of its fee structure and interest rates, which can be considerable. These costs are a significant factor in determining the card’s overall value and should be carefully considered before applying.

- Annual Fee: The annual fee for the Aspire Credit Card can range from $85 to $175 for the first year. After the first year, this fee may drop to $49, though some sources indicate it could be as high as $229 in subsequent years depending on the specific card product. This variability necessitates checking the specific offer terms.

- Monthly Maintenance Fee: A notable feature of the Aspire card’s fee structure is the introduction of a monthly maintenance fee starting in the second year. This fee can be up to $15 per month ($180 annually). Combined with the annual fee, the total cost in the second year and beyond can be substantial.

- High APR: The Aspire Mastercard carries a very high fixed Annual Percentage Rate (APR) for purchases, typically ranging from 29.99% to 36.00%. This high APR means that carrying a balance on this card can quickly accumulate significant interest charges, making it crucial to pay the balance in full each month.

- Other Potential Fees: Cardholders may also encounter other fees, including a cash advance fee (typically 5% of the amount, with a minimum of $10), a foreign transaction fee (around 3% of each transaction), and late payment or returned payment fees (up to $41). There might also be a fee for an authorized user.

Given these fees, the Aspire Credit Card is best utilized by disciplined individuals who intend to make small purchases and pay their balance in full every month to avoid interest and minimize fee accumulation. If balances are carried, the high APR can quickly erode any cash back rewards earned and make credit building an expensive endeavor.

How the Aspire Card Facilitates Credit Building

The core purpose of the Aspire Credit Card for many users is to build or rebuild credit. It achieves this through several key mechanisms, primarily by allowing cardholders to establish a positive payment history.

- Reporting to All Major Credit Bureaus: As mentioned, Aspire reports payment activity to Equifax, Experian, and TransUnion. Payment history is the most significant factor in calculating a credit score, accounting for about 35% of the total. By consistently making on-time payments, cardholders can demonstrate reliability and positively impact their credit file.

- Demonstrating Credit Utilization: Credit utilization, which is the amount of credit you’re using compared to your total credit limit, is another critical factor, typically accounting for 30% of a credit score. By using the Aspire card for small, manageable purchases and paying the balance in full, cardholders can keep their utilization low (ideally below 30% of their credit limit). This shows lenders that they can manage available credit responsibly without becoming overly reliant on it.

- Establishing a Credit Mix (Over Time): While Aspire is just one type of credit, using it responsibly helps establish a foundation. As credit improves, individuals may qualify for other types of credit, diversifying their credit mix, which is another factor in credit scoring models.

- Opportunity for Credit Limit Increases: Some credit card issuers, including those similar to Aspire, may periodically review accounts for credit limit increases based on responsible usage. A higher credit limit, while maintaining low balances, can further improve the credit utilization ratio.

For individuals starting with a limited or poor credit history, the Aspire card offers an opportunity to demonstrate creditworthiness. The key lies in diligent and responsible usage, prioritizing on-time payments and low credit utilization over carrying a balance or maximizing cash back rewards.

Eligibility Requirements and Application Process

Understanding the criteria for the Aspire Credit Card and the application steps can help prospective cardholders prepare and increase their chances of approval.

Eligibility Requirements: The Aspire Credit Card is designed for individuals with bad or limited credit. While specific criteria can vary, general requirements include:

- Credit Score: Applicants with bad credit, generally a FICO score of 300 or higher, or below 640, may be considered. Some sources suggest a minimum credit score of 500.

- Age: Applicants must be at least 18 years old.

- Income: Enough income to make monthly minimum payments is required. Income verification, possibly through bank account information, may be requested.

- Identification: A Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) is usually necessary.

- Residency: A physical address in the U.S. is typically required.

Application Process: The application for the Aspire Credit Card is primarily done online and is generally straightforward.

- Prequalification: Start by utilizing the online prequalification tool on the Aspire website or through partner sites. This involves a soft credit inquiry, which does not impact your credit score, and provides instant offers.

- Full Application: If you receive and accept an offer, you will proceed with the full application. This step involves providing detailed personal and financial information, such as your name, address, phone number, SSN, date of birth, income, sources of income, employment status, and housing status.

- Hard Inquiry: Submitting the full application will trigger a “hard pull” on your credit report, which may temporarily affect your credit score.

- Decision and Card Issuance: A decision may be received immediately, or it could take a few business days. If approved, the card is typically mailed within 7-10 business days.

It’s crucial to ensure all information provided is accurate and complete, as knowingly reporting false information is a federal crime. While prequalification offers a strong indication of approval, final approval is not guaranteed.

| Feature | Aspire Cash Back Rewards Mastercard | Typical Secured Credit Card |

|---|---|---|

| Security Deposit Required | No | Yes (Refundable) |

| Target Credit Score | Bad to Fair (300-640 FICO) | No Credit/Poor Credit |

| Annual Fee (Year 1) | $85-$175 | Often $0-$39 |

| Monthly Maintenance Fee | Up to $15/month (after Year 1) | Rare |

| Purchase APR | 29.99%–36.00% Fixed | Often high (e.g., 20-25%) |

| Cash Back Rewards | Up to 3% on select categories | Typically none, or very limited |

| Credit Bureau Reporting | All 3 major bureaus | All 3 major bureaus (most reputable) |

| Credit Limit Range | $350-$1,000 | Equals deposit amount (e.g., $200-$2,500) |

Essential Strategies for Building and Improving Credit

While a credit card like Aspire can be a valuable tool, successful credit building hinges on adopting sound financial habits. Here are essential strategies to help improve and maintain a healthy credit score:

- Pay All Bills on Time, Every Time: This is arguably the most crucial factor in your credit score, accounting for about 35% of it. Timely payments for credit cards, loans, utility bills, and even rent (if reported) demonstrate reliability to lenders. Setting up automatic payments can help ensure you never miss a due date.

- Keep Credit Utilization Low: Aim to keep your credit utilization ratio below 30%—meaning you should use no more than 30% of your available credit at any given time. The lower, the better. For example, if your total credit limit is $1,000, try to keep your balance below $300. This shows that you are not over-reliant on credit.

- Pay Off Balances in Full: If possible, pay your credit card balance in full each month. This not only helps keep your utilization low but also avoids incurring high interest charges, especially with cards like Aspire that have high APRs.

- Monitor Your Credit Report Regularly: Regularly check your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) for errors or fraudulent activity. You are entitled to a free copy of your credit report from each bureau annually. Correcting inaccuracies can positively impact your score.

- Limit New Credit Applications: While it might be tempting to open multiple credit accounts, too many applications in a short period can negatively impact your credit score. Each “hard inquiry” from an application can cause a temporary dip in your score. Apply for new credit only when necessary.

- Maintain a Mix of Credit (Over Time): As your credit improves, having a mix of credit types, such as installment loans (e.g., car loans, student loans) and revolving credit (credit cards), can be beneficial. However, this should be done gradually and responsibly, not by taking on unnecessary debt.

- Consider Becoming an Authorized User: If you have a trusted family member with an excellent credit history, they might add you as an authorized user on one of their credit card accounts. This can allow you to benefit from their positive payment history, though it’s crucial that the primary cardholder maintains good habits.

- Be Patient: Building good credit is a marathon, not a sprint. It takes time and consistent responsible behavior to see significant improvements in your credit score. Stick to good habits, and your score will gradually rise.

Comparing Aspire with Other Credit-Building Options

While the Aspire Credit Card offers an unsecured option for building credit, it’s beneficial to consider it in the context of other available credit-building tools. Understanding the landscape can help consumers make informed decisions.

- Secured Credit Cards: These cards require a refundable security deposit, which typically becomes your credit limit. They are often easier to obtain for those with no credit or very poor credit because the deposit mitigates risk for the lender. Many secured cards have lower annual fees, and some even offer paths to graduate to an unsecured card and get the deposit back. Examples include Discover it® Secured Card or Capital One Platinum Secured Credit Card. For individuals who can afford the deposit, secured cards often present a more cost-effective way to build credit due to potentially lower fees and APRs compared to some unsecured options for bad credit.

- Credit Builder Loans: Offered by some credit unions and community banks, a credit builder loan works differently. You make payments into a savings account, which is then released to you after the loan term. The payments are reported to credit bureaus, helping to establish a positive payment history and build savings simultaneously.

- Student Credit Cards: For students with limited or no credit history, student-specific credit cards can be an option. They often have lower credit limits and may offer rewards, providing an entry point into credit with more favorable terms than some cards for bad credit.

- Authorized User Status: As discussed, being added as an authorized user on a financially responsible person’s account can help establish credit history, particularly if that account has a long history of on-time payments and low utilization.

- Rent and Utility Reporting Services: Services exist that report your on-time rent and utility payments to credit bureaus, which traditionally are not included in credit reports unless delinquent. These can be valuable for individuals without traditional credit accounts.

The Aspire Card’s main differentiator is being an unsecured card accessible to those with bad credit and offering cash back rewards, without requiring a deposit. However, its high fees and APR mean that alternatives, especially secured cards or credit builder loans, might be more suitable for some, particularly if they are sensitive to costs or struggle with impulse spending. Comparing the total cost (fees + potential interest) against the benefits is crucial for making the best choice.

Responsible Credit Card Management with Aspire

Owning any credit card, especially one designed for credit building like the Aspire Mastercard, requires a commitment to responsible financial management. This is not just about avoiding debt, but about strategically using the card to improve your credit standing.

- Budgeting is Key: Before making any purchases, have a clear budget. Know exactly what you can afford to pay back in full each month. The Aspire card’s high APR means that carrying a balance is very costly, so treat it like a debit card by only spending what you already have.

- Use for Small, Regular Purchases: Instead of large, impulse buys, use the Aspire card for small, predictable expenses like a portion of your gas or grocery budget, or a recurring utility bill. This ensures regular activity on the account, which is necessary for building payment history, while keeping balances manageable.

- Set Up Payment Reminders: Given the importance of on-time payments, set up reminders through your bank, the Aspire mobile app, or personal calendar. Consider automatic payments for at least the minimum amount to avoid late fees and negative marks on your credit report. Remember, even a few days late can hurt your score.

- Monitor Spending and Account Activity: Regularly check your account statements and transactions through Aspire’s online portal or mobile app. This helps you track your spending, detect any fraudulent activity, and stay aware of your credit utilization.

- Understand Your Credit Limit: Be clear about your credit limit and strive to keep your balance well below it to maintain a low credit utilization ratio. A lower utilization percentage is favorable for your credit score.

- Review Fees Annually: With Aspire’s changing fee structure after the first year (annual fee adjustment and introduction of a monthly maintenance fee), regularly review the costs. Evaluate if the credit-building benefits and cash back rewards continue to outweigh the total annual cost, especially as your credit score improves and you might qualify for cards with better terms.

- Avoid Cash Advances: Cash advances typically come with immediate interest charges (no grace period), higher APRs, and additional fees. Avoid them unless absolutely necessary.

By adhering to these responsible management practices, the Aspire Credit Card can serve as an effective stepping stone towards a stronger credit profile, opening doors to more favorable financial products in the future.

Conclusion

The Aspire Credit Card, particularly the Aspire® Cash Back Rewards Mastercard, presents a viable option for individuals with bad or limited credit who are committed to improving their financial standing. Its key appeal lies in being an unsecured card that reports to all three major credit bureaus, offering a direct path to establish a positive payment history and credit utilization. The added benefit of cash back rewards on everyday spending categories like gas, groceries, and utilities can, to some extent, help offset its associated costs.

However, prospective cardholders must approach the Aspire card with a clear understanding of its significant fees, including a variable annual fee and a monthly maintenance fee that commences in the second year, alongside a notably high APR. For the Aspire card to be a truly effective credit-building tool, it demands rigorous financial discipline: paying balances in full and on time every month, and maintaining low credit utilization to avoid escalating interest charges. Failure to do so can quickly make the card an expensive endeavor, hindering rather than helping credit improvement.

Ultimately, while Aspire provides a crucial entry point for many into the credit world without the need for a security deposit, it’s not without its caveats. For those who can manage its fee structure and high APR through diligent payments, it can be an instrumental step towards a healthier credit score. Yet, exploring alternative credit-building products like secured credit cards or credit builder loans, especially for those who can afford a deposit, might offer a more cost-effective long-term solution. Responsible credit management, regardless of the card chosen, remains the cornerstone of financial wellness. For further insights into managing credit effectively and understanding your consumer rights, resources like the Consumer Financial Protection Bureau website offer valuable guidance.