6 Smart Reasons to Love Zero Percent Credit Cards – Save on Interest

Table of Contents

Zero percent credit cards with introductory APR offers have become a cornerstone of modern personal finance, promising a temporary reprieve from interest charges on purchases, balance transfers, or both. These cards present a compelling opportunity for consumers to manage debt more effectively, finance large expenses without immediate added cost, or simply gain some breathing room in their budget. However, like any powerful financial tool, they come with a crucial set of terms, conditions, and best practices that dictate their true value. Understanding the intricacies of these offers is paramount to leveraging them for financial advantage rather than falling into common pitfalls. This comprehensive guide will delve into what 0% APR credit cards entail, how they function, their potential benefits and risks, and provide actionable strategies for their responsible and effective use.

Understanding Zero Percent APR Introductory Offers

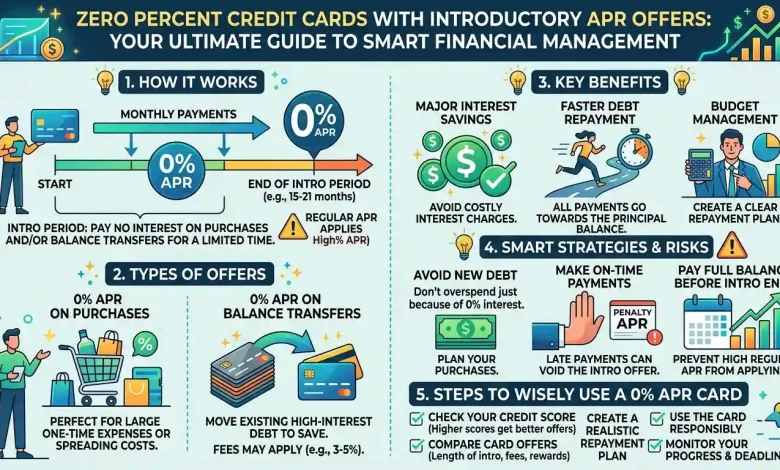

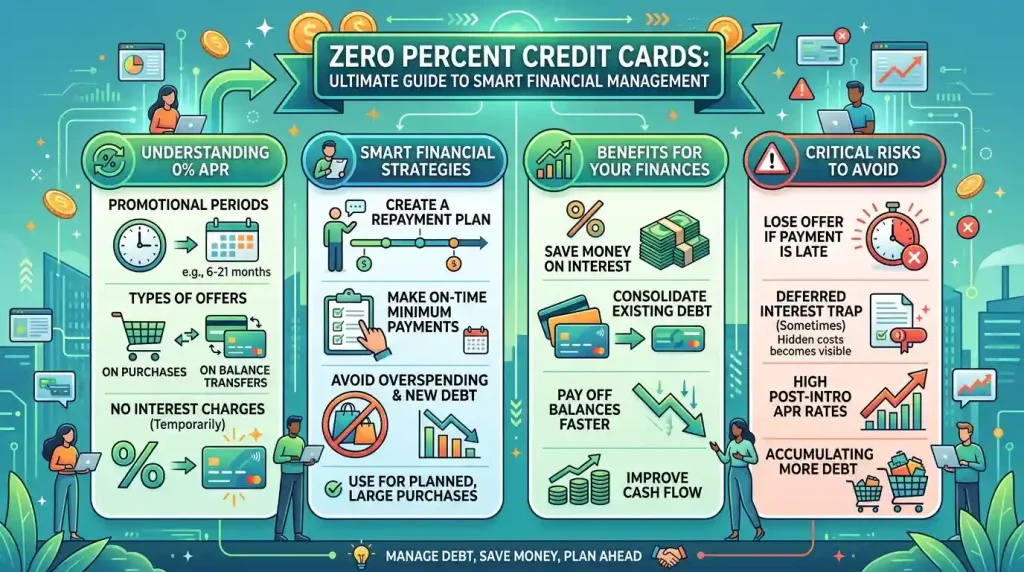

At its core, a 0% APR credit card means that for a specified “introductory” or “promotional” period, you will not be charged interest on qualifying transactions. APR stands for Annual Percentage Rate, which is the yearly cost of borrowing money. During this promotional window, typically ranging from 6 to 21 months, every dollar you pay towards your balance goes directly to the principal, allowing for faster debt reduction or interest-free financing.

The ubiquity of these offers in the U.S. credit card market is significant, with studies indicating that approximately 25% of all credit card debt has been associated with an introductory promotional offering, most of which were 0% APR. Credit card issuers extend these promotions to attract eligible applicants, often those with good to excellent credit scores, as a sign-up incentive. It’s a strategic marketing tactic designed to expand their customer base and, ultimately, profit from transaction fees and potential interest revenue once the promotional period concludes.

The Multifaceted Benefits of Zero Percent APR Credit Cards

When used judiciously, 0% APR credit cards offer several distinct advantages that can significantly bolster your financial health.

Debt Consolidation and Interest Savings

One of the most popular uses for a 0% APR credit card is consolidating high-interest debt from other credit cards. By transferring existing balances to a new card with a 0% introductory APR on balance transfers, you can effectively “pause” the accumulation of interest, allowing more of your payments to go towards the principal. This can lead to paying off debt faster and saving a substantial amount of money in interest charges. While balance transfers usually incur a fee (typically 3% to 5% of the transferred amount), the savings from avoiding high interest rates often outweigh this upfront cost.

Financing Large Purchases Without Immediate Interest

Another compelling benefit is the ability to finance significant purchases without accruing interest for an extended period. Whether it’s a new appliance, home improvements, or unexpected medical expenses, a 0% APR on purchases allows you to break down the cost into manageable monthly payments over the introductory period. For example, if you purchase a $1,200 item with a 12-month 0% APR offer, you’d need to pay $100 per month to clear the balance before interest kicks in, assuming no other charges. This strategy can help you avoid depleting your savings or emergency fund for a major expense.

How Zero Percent APR Offers Function

The mechanism behind 0% APR cards is relatively straightforward but requires attention to detail. Upon approval, the credit card issuer waives interest charges on specific types of transactions for a predetermined period. This period can range from a few months to over two years, with many offers falling between 12 to 21 months.

It’s critical to understand that the 0% APR may apply differently depending on the card. Some cards offer 0% APR exclusively on new purchases, while others focus solely on balance transfers. Many, however, extend the promotional rate to both. Cash advances are almost never included in 0% APR offers and typically accrue interest immediately at a higher rate.

Crucially, even during the 0% APR period, you are still required to make at least the minimum monthly payment on time. Failing to do so can result in late fees, and more significantly, may cause you to lose your introductory APR offer, triggering the standard variable APR or even a higher penalty APR on your remaining balance.

Choosing the Right Zero Percent APR Card for Your Needs

Selecting the ideal 0% APR credit card involves careful consideration of your financial goals and the specific terms of different offers. Not all 0% APR cards are created equal, and what works for one person may not be suitable for another.

Balance Transfer Cards vs. Purchase Cards

The primary distinction lies in whether the 0% APR applies to purchases, balance transfers, or both. If your main objective is to pay down existing high-interest debt, a card with a strong balance transfer offer is essential. Look for cards with a long 0% APR period for balance transfers and be mindful of any associated balance transfer fees. Conversely, if you plan a large upcoming expense, a card offering 0% APR on new purchases would be more appropriate. Some cards offer a dual benefit, providing 0% APR on both, which can be highly versatile.

Understanding Fees and Post-Introductory APRs

Beyond the introductory rate, always examine the balance transfer fees, annual fees, and especially the regular APR that will apply once the promotional period ends. The post-introductory APR can be significantly higher, often in the range of 15% to 29% or more, and will apply to any remaining balance. This information is typically detailed in the cardmember agreement and is vital for planning your repayment strategy.

| Feature/Consideration | Details to Evaluate | Importance |

|---|---|---|

| Introductory APR Period Length | Duration of 0% APR for purchases, balance transfers, or both (e.g., 12, 15, 18, 21 months). | Longer periods offer more time to pay off debt interest-free. |

| Applicability of 0% APR | Does it apply to purchases, balance transfers, or both? | Crucial for aligning the card with your specific financial goal (debt payoff vs. new spending). |

| Balance Transfer Fees | Percentage charged on transferred balances (typically 3-5%). | Factor into total cost savings; a lower fee is better. |

| Annual Fee | Is there a yearly fee for the card? | Avoid if possible, or ensure rewards/benefits justify the cost. |

| Standard Variable APR | The interest rate after the introductory period ends. | Crucial for understanding potential future costs if a balance remains. |

| Credit Score Requirements | Minimum credit score generally required for approval (often good to excellent). | Determines your eligibility and prevents unnecessary hard inquiries. |

| Penalty APR | A higher APR applied if you miss a payment or violate terms. | Highlights the importance of on-time payments. |

| Rewards Program | Are there cash back or points rewards on purchases? | An added benefit, but shouldn’t overshadow the primary 0% APR goal. |

Strategies for Maximizing the Benefits of 0% APR Cards

To truly harness the power of a 0% APR credit card, a strategic approach is necessary. Merely getting the card is only the first step; effective management is what yields real savings and financial progress.

- Create a Detailed Repayment Plan: Before making any purchases or transfers, calculate exactly how much you need to pay each month to clear the balance before the 0% APR period expires. This structured approach ensures you avoid incurring interest.

- Prioritize Payments to Principal: Since no interest is accruing during the introductory period, every payment directly reduces your principal balance. Maximize this opportunity by paying as much as you can.

- Avoid New Purchases on Balance Transfer Cards: If you’re using a card for a balance transfer, it’s generally best to avoid making new purchases on that card. Some credit card companies apply payments to the lowest interest balance first, meaning new purchases could start accruing interest while your transferred balance remains interest-free. Consider using a separate rewards card for everyday spending.

- Set Up Automatic Payments: Ensure you never miss a minimum payment by setting up automatic payments from your bank account. This protects your 0% APR offer and avoids late fees and potential penalty APRs.

- Monitor Your Progress: Regularly check your statements to ensure your payments are on track and that you’re adhering to your payoff plan.

Navigating Potential Pitfalls and Avoiding Common Mistakes

While 0% APR offers are attractive, they are not without risks. Credit card companies design these offers to be profitable, often relying on consumer behavior that leads to interest accumulation after the promotional period. Awareness of these pitfalls is key to avoiding them.

Impact on Your Credit Score

Applying for a new credit card results in a hard inquiry on your credit report, which can cause a slight, temporary dip in your credit score. However, if managed responsibly, a 0% APR card can ultimately benefit your credit score. Consolidating debt to a single card can lower your credit utilization ratio, a major factor in credit scoring, especially if your previous cards show lower balances. The key is to avoid “card flipping”—repeatedly opening new 0% APR cards and transferring balances—as this can negatively impact your credit score by increasing hard inquiries and lowering the average age of your accounts. For a more comprehensive understanding of credit scores, you can refer to Wikipedia’s Credit Score page.

The Dangers of Missing Payments

As mentioned, missing even a single minimum payment can have severe consequences. You could lose your introductory 0% APR, face late fees, and potentially be hit with a penalty APR. This penalty APR is often much higher than the standard variable rate and could apply to your entire existing balance. Setting up autopay is a simple yet effective way to mitigate this risk.

Key Considerations Before Applying

Before you jump into applying for a 0% APR credit card, take a moment to assess your situation and the specific terms of the offers available. Thoughtful preparation can make all the difference in whether these cards truly help or hinder your financial journey.

Credit Score Requirements

Most of the best 0% APR credit cards are offered to consumers with good to excellent credit scores. Before applying, check your credit score to gauge your eligibility. Applying for a card you’re unlikely to get approved for will only result in a hard inquiry on your credit report, which can temporarily lower your score without providing any benefit.

The Importance of Reading the Terms and Conditions

This cannot be overstated. The fine print contains crucial details about the length of the introductory period, what types of transactions qualify, any balance transfer fees, the standard APR after the promotional period, and specific actions that could revoke your 0% APR. Pay close attention to the difference between a 0% intro APR offer and a “deferred interest” offer. With deferred interest, if you don’t pay off the entire balance by the end of the promotional period, you could be charged interest retroactively on the entire original purchase amount, not just the remaining balance. This distinction is critical to avoid unexpected costs.

Budgeting and Repayment Strategies

A 0% APR card is a tool for focused debt repayment or planned financing, not an invitation to overspend. Develop a realistic budget and a strict repayment plan that ensures you can pay off the entire balance before the introductory period ends. If you’re using it for purchases, consider whether you would have made that purchase if interest were being charged from day one. Similarly, if you’re transferring a balance, commit to not accumulating new debt on your old cards.

Monitoring Your Progress and Future Financial Health

Regularly review your credit card statements and track your payments against your repayment plan. Staying proactive ensures you’re on schedule to clear your balance before interest charges begin. Beyond the immediate goal, consider how this card fits into your long-term financial health. The aim is to reduce debt and improve your credit profile, which can open doors to better financial products and opportunities in the future. Maintaining a low credit utilization ratio across all your accounts is a good practice.

Comparing Different Offers

The market for 0% APR credit cards is competitive, with many issuers offering varying lengths of introductory periods and different benefits. Take the time to compare offers from multiple credit card companies. Look for cards that align with your specific needs, whether it’s the longest 0% APR period for balance transfers or a good rewards program alongside an introductory purchase APR. Some cards may offer extended 0% APR periods for both purchases and balance transfers, offering maximum flexibility.

What Happens When the Introductory Period Ends?

Once the 0% APR period concludes, any remaining balance on the card will begin to accrue interest at the card’s standard variable APR. If you haven’t paid off your balance by this point, you could face significant interest charges. Options at this stage include paying off the remaining balance in a lump sum, continuing to make payments at the standard APR, or, in some cases, applying for another 0% APR card to transfer the balance again (though this “card flipping” strategy comes with its own risks and potential negative impacts on your credit score).

Seeking Professional Financial Advice

If you find yourself overwhelmed by debt or unsure about the best way to utilize a 0% APR credit card, consider consulting a financial advisor. They can provide personalized guidance and help you develop a comprehensive financial plan that addresses your specific situation. This can be particularly beneficial if you have a large amount of debt or are struggling to manage your finances.

Responsible Use for Long-Term Gain

Ultimately, 0% APR credit cards are powerful short-term tools that demand responsible usage for long-term financial gain. They are not a substitute for a solid financial foundation, which includes building an emergency fund and consistently living within your means. Used strategically and with a clear repayment plan, a 0% APR card can be an excellent way to save money, pay down debt faster, or make large purchases more manageable. However, without discipline and a thorough understanding of the terms, they can quickly lead to more debt and financial stress. For those considering debt consolidation, exploring best balance transfer credit cards might be a logical next step to compare various offers.

Conclusion: Harnessing the Power of 0% APR

Zero percent credit cards with introductory APR offers are more than just a promotional gimmick; they are a sophisticated financial instrument that, when wielded correctly, can unlock significant savings and provide invaluable flexibility. From strategically consolidating high-interest debt to financing substantial purchases without the immediate burden of interest, these cards empower consumers to take proactive steps towards their financial goals. However, their true potential is only realized through careful planning, diligent adherence to repayment schedules, and a keen understanding of the fine print. By choosing the right card for your specific needs, creating a robust payoff strategy, and meticulously avoiding common pitfalls such as missed payments or overspending, you can transform a temporary interest holiday into a powerful catalyst for enduring financial well-being. Approaching these offers with knowledge and discipline ensures that you are truly in control, leveraging them to your advantage and paving the way for a more secure financial future.