6 Must-Know Credit Card Fees Before You Apply – Avoid Hidden Charges

Table of Contents

Credit card fees are an inevitable part of the financial landscape for anyone utilizing credit. While the convenience and benefits of credit cards are undeniable, a myriad of associated fees can quickly erode those advantages if you’re not fully informed. Before you apply for a new credit card, or even if you’re already a cardholder, understanding the various charges that can impact your finances is crucial. From upfront costs to penalties for certain transactions or missed payments, these fees can significantly influence the true cost of your credit card. Being aware of these potential expenses allows you to choose the right card for your needs, manage your account more effectively, and ultimately save money.

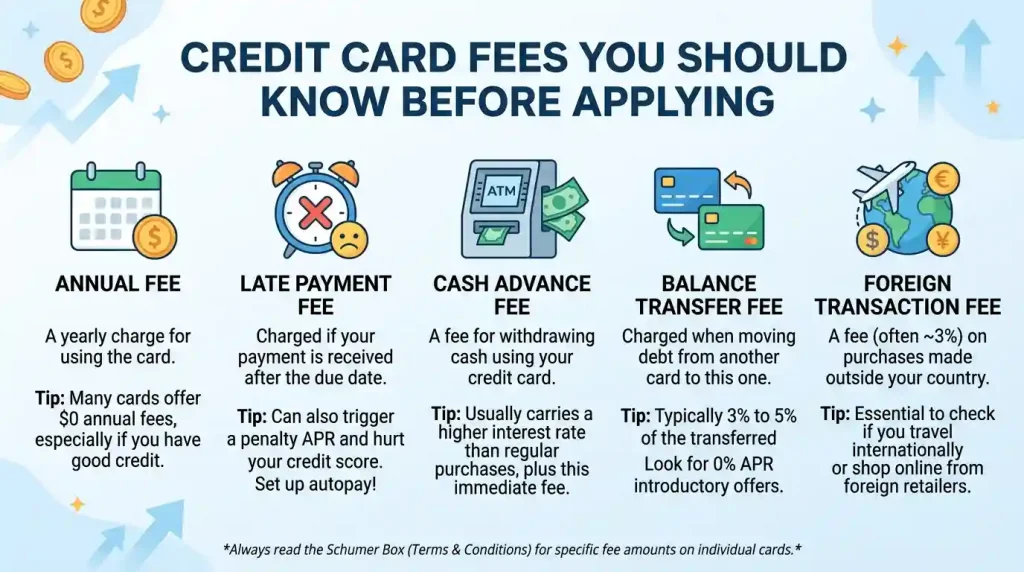

Understanding Annual Fees

An annual fee is a recurring charge levied by some credit card issuers simply for the privilege of holding the card. Think of it as a membership fee for access to the card’s features, rewards programs, and benefits. Not all credit cards come with an annual fee; in fact, many popular options, particularly entry-level cards or those designed for building credit, offer no annual fee. However, cards with more lucrative rewards, premium perks (like airport lounge access or travel credits), or those geared towards specific niches often carry an annual fee.

The amount of an annual fee can vary significantly. According to WalletHub’s data, the average credit card annual fee is $28.25. Other sources indicate that average annual fees can range from $94 to $157, depending on the size of the issuer, and some premium cards can charge hundreds of dollars, even up to $895. For business credit cards, the average annual fee in the U.S. can be around $135, with a median of $111. These fees are typically charged when you first open the account and then annually on your cardholder anniversary. Some issuers might even offer promotions that waive the annual fee for the first year to attract new applicants.

To determine if an annual fee is worth it, it’s essential to weigh the cost against the benefits and rewards you receive. If the value of the rewards (cash back, travel points, exclusive access) or the specific features of the card outweigh the annual charge, then paying the fee might be a sensible financial decision. For example, a cash back card with a $95 annual fee that offers 2% back on all purchases could potentially earn you $200 in cash back if you spend $10,000 annually, thus offsetting the fee and providing an additional $105. However, if you don’t utilize the card’s benefits enough to recoup the fee, a no-annual-fee option would likely be more cost-effective.

Interest Rates and APRs: The Cost of Borrowing

Interest charges, also known as finance charges, represent the cost of borrowing money on your credit card. This is expressed as an Annual Percentage Rate (APR), which is the yearly rate of interest you’ll pay on any outstanding balance. Credit card interest is primarily charged when you carry a balance from one billing cycle to the next, meaning you don’t pay your full statement balance by the due date. If you consistently pay your balance in full and on time each month, you can often avoid paying any interest on new purchases, thanks to a grace period typically offered by issuers. The Credit Card Accountability Responsibility And Disclosure (CARD) Act of 2009 set the minimum grace period at 21 days.

Interest on credit cards accrues daily, based on a daily periodic rate (DPR). This DPR is calculated by dividing your APR by 365. For example, if your APR is 16%, your daily rate would be approximately 0.044% (16% / 365 days). This daily interest is then multiplied by your average daily balance, and these charges can quickly compound, meaning you start paying interest on previously accrued interest.

It’s important to note that many credit cards have different APRs for various types of transactions. The purchase APR is the standard rate for everyday purchases. However, cash advances and balance transfers often come with higher, separate APRs, and interest on these types of transactions may begin accruing immediately without a grace period. Variable interest rates, which are more common, can fluctuate over time based on benchmarks like the Federal Reserve Prime Rate. Fixed interest rates, while less common, remain relatively consistent unless the issuer notifies you of a change. Understanding how interest is calculated and applied is fundamental to managing your credit card debt effectively and avoiding unnecessary costs.

Late Payment Fees: A Costly Oversight

Late payment fees are penalties charged by your credit card issuer when you fail to make at least the minimum payment by the due date on your billing statement. This is one of the most common and easily avoidable fees, yet it can be quite costly. Historically, these fees could be significant, ranging from around $25-$30 for a first late payment and increasing for subsequent late payments within a six-month period. In 2024, the Consumer Financial Protection Bureau (CFPB) finalized a rule to cap most credit card late fees for large issuers at $8, though the rule’s status has been subject to legal challenges. Despite this, some smaller issuers and subprime cards may still charge higher fees, potentially up to $32 for a first late fee and $43 for subsequent ones.

The impact of a late payment extends beyond just the fee itself. Missing a payment, especially if it goes 30 days or more past due, can be reported to credit bureaus and significantly harm your credit score. This negative mark can remain on your credit report for years, affecting your ability to obtain new credit or favorable interest rates in the future. Late fees disproportionately affect younger, lower-income, and lower-credit-score individuals. For instance, Gen Z is three times more likely than baby boomers to incur late fees, and low-income households pay them at roughly 3.5 times the rate of high earners.

To avoid late payment fees, the most effective strategies include setting up automatic payments or payment reminders. Many issuers will also waive a first late fee if you call and request it as a courtesy. Ensuring you have sufficient funds in your linked bank account to cover the payment is also critical to prevent returned payment fees, which are often charged when a payment is rejected due to insufficient funds.

Balance Transfer Fees: Moving Debt Strategically

A balance transfer fee is a charge incurred when you move existing debt from one credit card to another, typically to consolidate debt or take advantage of a lower, often 0% introductory Annual Percentage Rate (APR) on the new card. This strategy can be highly effective for paying off high-interest debt, as it allows more of your payment to go towards the principal rather than interest during the promotional period.

These fees are almost always a percentage of the total balance you transfer, commonly ranging from 3% to 5%. For example, transferring a $5,000 balance with a 3% fee would incur a $150 charge, which is typically added to your new card’s total balance. Most balance transfer fees also come with a minimum charge, often $5 or $10, whichever is greater than the percentage calculation.

While a 0% introductory APR on balance transfers can lead to significant savings on interest, it’s crucial to calculate whether the potential interest savings outweigh the balance transfer fee. Some credit cards offer no balance transfer fees, especially if the transfer is made within a specific introductory timeframe, but these are less common. When considering a balance transfer, you should also look at how long the introductory APR period lasts, what the APR will be after the promotional period ends, and any other fees the card might charge, such as annual fees. Additionally, the transferred balance, including the fee, will utilize part of your new card’s credit limit.

Cash Advance Fees: Expensive Convenience

A cash advance fee is a charge incurred when you use your credit card to obtain cash, rather than making a purchase. This typically happens by withdrawing cash from an ATM, visiting a bank, or cashing checks provided by your credit card company. While it offers quick access to funds, cash advances are an exceptionally expensive way to get cash and should generally be avoided unless absolutely necessary.

The fee for a cash advance is usually a percentage of the amount withdrawn, typically ranging from 3% to 5%, often with a minimum flat fee of $5 or $10, whichever is greater. For example, a $100 cash advance with a 5% fee would add $5 to your bill, meaning you’d owe $105 for the $100 you received. The average cash advance fee is around 4.03%.

Beyond the upfront fee, cash advances come with other significant drawbacks. Interest on cash advances typically starts accruing immediately, without any grace period, and often at a higher APR than your standard purchase rate. This means the fee compounds with daily interest from day one. Certain transactions that you might not consider a direct cash withdrawal can also be classified as cash advances, such as peer-to-peer money transfers, purchasing cryptocurrencies, making loan payments, buying money orders or traveler’s checks, or engaging in gambling. To avoid these high costs, consider alternatives like using an emergency fund, a personal loan, or borrowing from friends or family.

Foreign Transaction Fees: International Spending Costs

Foreign transaction fees are surcharges applied to purchases made with your credit card outside of your home country, or when making purchases online from an international merchant. These fees are designed to cover the costs associated with processing international transactions and currency conversion.

The typical range for foreign transaction fees is between 1% and 3% of the total transaction amount. While a small percentage, these charges can quickly accumulate, especially if you travel frequently or make many international online purchases. For instance, a 3% fee on a $100 purchase means an extra $3, which adds up significantly over a trip or multiple online transactions. The average foreign fee is roughly 1.5%. These fees can be a combination of charges from both the card issuer and the network (e.g., Visa, Mastercard).

A common pitfall to be aware of while traveling is Dynamic Currency Conversion (DCC). This occurs when a merchant offers to process your transaction in your home currency instead of the local currency. While seemingly convenient, it often comes with an unfavorable exchange rate set by the merchant’s bank, and your card issuer may still apply its standard foreign transaction fee. To avoid this, always choose to pay in the local currency when offered the option.

The best way to circumvent foreign transaction fees is to use a credit card that specifically advertises no foreign transaction fees. Several major card issuers, such as Capital One, Discover, and USAA, do not charge foreign transaction fees on any of their cards. Many travel rewards cards also forgo these fees, making them ideal for international use.

Other Miscellaneous Credit Card Fees

Beyond the major categories of fees, credit card issuers can impose several other charges that cardholders should be aware of. While some are less common due to regulations, others can still catch you off guard.

Over-Limit Fees

An over-limit fee is charged when your account balance exceeds your assigned credit limit. While once more common, the Credit Card Accountability Responsibility and Disclosure (CARD) Act of 2009 significantly regulated how these fees are charged. Now, you can only be charged an over-limit fee if you explicitly opt-in to allow transactions that exceed your credit limit. If you don’t opt-in, transactions that would push you over your limit will simply be declined. If you do opt-in, fees can typically reach as high as $35, but cannot exceed the amount by which you went over your limit. To avoid this, always keep track of your spending and stay well within your credit limit.

Returned Payment Fees

A returned payment fee is charged when a payment you make to your credit card issuer is rejected, typically due to insufficient funds in your linked bank account. These fees usually range from $25 to $40. To avoid this, always ensure your checking or savings account has enough money to cover your credit card payments.

Authorized User Fees

Some credit card issuers charge a fee for adding an authorized user to your account. While not universal, it’s worth checking if you plan to share your credit line with a family member or trusted individual.

Card Replacement Fees

If your credit card is lost, stolen, or damaged, some issuers may charge a fee for a replacement card. However, many companies provide replacement cards for free.

Expedited Shipping or Payment Fees

If you need a new card quickly, some issuers offer expedited shipping for a fee. Similarly, if you make certain expedited credit card payments over the phone through a customer service agent, a fee might apply.

Monthly Fees or Program Fees

While less common with mainstream credit cards, some secured or subprime cards, or those issued by credit unions, might impose monthly fees instead of or in addition to an annual fee. There can also be upfront “program fees” that you pay before even getting the card.

How to Avoid and Minimize Credit Card Fees

Understanding credit card fees is the first step; actively working to avoid or minimize them is where the real savings happen. By adopting smart financial habits and being strategic about your card choices, you can significantly reduce the overall cost of using credit.

- Pay Your Balance in Full and On Time: This is arguably the most crucial step. Paying your statement balance in full before the due date allows you to avoid interest charges entirely due to the grace period. Setting up automatic payments or calendar reminders can help ensure you never miss a due date and thus avoid late payment fees.

- Choose No-Annual-Fee Cards: If you don’t anticipate utilizing the premium benefits of a card that charges an annual fee, opt for a card with no annual fee. There are many excellent no-annual-fee options available, including those with rewards programs.

- Avoid Cash Advances: As discussed, cash advances are an expensive way to get cash due to high fees and immediate interest accrual. Explore other options like an emergency fund, a personal loan, or drawing from a savings account instead.

- Use Cards with No Foreign Transaction Fees for International Spending: If you travel abroad frequently or make international online purchases, ensure your credit card doesn’t charge foreign transaction fees. Many cards specifically designed for travelers or those from certain issuers (like Capital One and Discover) offer this benefit. Always choose to pay in the local currency when given the option overseas to avoid unfavorable dynamic currency conversion rates.

- Be Mindful of Balance Transfers: While beneficial for debt consolidation, always calculate if the interest savings outweigh the balance transfer fee. Look for cards with 0% introductory balance transfer fees if possible, especially within a limited timeframe.

- Stay Within Your Credit Limit: Unless you’ve explicitly opted in for over-limit transactions, your card issuer will generally decline purchases that exceed your limit. To avoid any potential over-limit fees or transaction denials, keep a close eye on your balance and stay well below your credit limit. A low credit utilization ratio (ideally below 30%) is also beneficial for your credit score.

- Review Your Credit Card Statements Regularly: Periodically checking your statements can help you identify any unexpected fees, erroneous charges, or even fraudulent activity. The Credit Card Accountability Responsibility and Disclosure Act (CARD Act) of 2009 requires all fees to be disclosed in the card’s terms and conditions, often in a “Schumer box”.

- Communicate with Your Issuer: If you incur a fee inadvertently, especially a late payment fee for the first time, don’t hesitate to call your credit card company. Many issuers are willing to waive certain fees as a one-time courtesy, particularly for good customers.

- Understand Your Card’s Terms and Conditions: Before applying for any credit card, take the time to read and understand the fine print regarding all fees, interest rates, and terms. This proactive approach can prevent costly surprises down the road.

| Fee Type | Description | Typical Cost/Range | How to Avoid/Minimize |

|---|---|---|---|

| Annual Fee | Recurring charge for holding the card. | $0 to $895+ (average ~$28 – $178) | Choose no-annual-fee cards; ensure benefits outweigh the cost. |

| Interest/Finance Charges | Cost for carrying a balance (APR). | Varies by APR (e.g., 16%-28%) | Pay your statement balance in full each month. |

| Late Payment Fee | Penalty for not making minimum payment by due date. | Up to $32-$43 (recent cap for large issuers at $8) | Pay on time; set up auto-pay; request waiver for first offense. |

| Balance Transfer Fee | Charge for moving debt to a new card. | 3% to 5% of transferred amount (min $5-$10) | Calculate if interest savings outweigh fee; look for 0% transfer fee offers. |

| Cash Advance Fee | Charge for withdrawing cash with your credit card. | 3% to 5% of advance (min $5-$10) | Avoid cash advances; use emergency funds or personal loans. |

| Foreign Transaction Fee | Surcharge for international purchases/transactions. | 1% to 3% of transaction amount | Use cards with no foreign transaction fees; pay in local currency abroad. |

| Returned Payment Fee | Charged when a payment is rejected (e.g., insufficient funds). | $25 to $40 | Ensure sufficient funds in linked bank account. |

| Over-Limit Fee | Charged for exceeding credit limit (if opted-in). | Up to $35, not exceeding overage amount | Do not opt-in; stay within credit limit. |

Conclusion

Credit card fees are a significant aspect of credit card ownership that can profoundly impact your financial health. From the recurring cost of annual fees to the potentially high penalties of late payments, and the often-overlooked charges like balance transfer and foreign transaction fees, each one represents an additional expense that can make credit more costly than anticipated. Interest rates, while not always a “fee” in the same sense, are the most substantial cost of borrowing if you carry a balance.

The key to navigating the world of credit cards successfully lies in informed decision-making and diligent management. By thoroughly researching a credit card’s terms and conditions before applying, you can select a product that aligns with your spending habits and financial goals. Furthermore, by adopting responsible practices such as paying your balance in full and on time, avoiding cash advances, and choosing cards appropriate for international travel, you can proactively minimize or eliminate many of these fees. Being vigilant about your account activity and understanding the nuances of how and when these charges apply will empower you to use credit cards as a valuable financial tool without falling victim to unnecessary costs. Remember, a well-managed credit card can be a powerful asset, but an unmanaged one can quickly become a liability. For more information on managing your credit responsibly, consider resources from reputable financial education organizations, such as the Consumer Financial Protection Bureau (CFPB).