6 Smart Reasons to Love 0% Interest Credit Cards for Balance Transfers & Purchases

Table of Contents

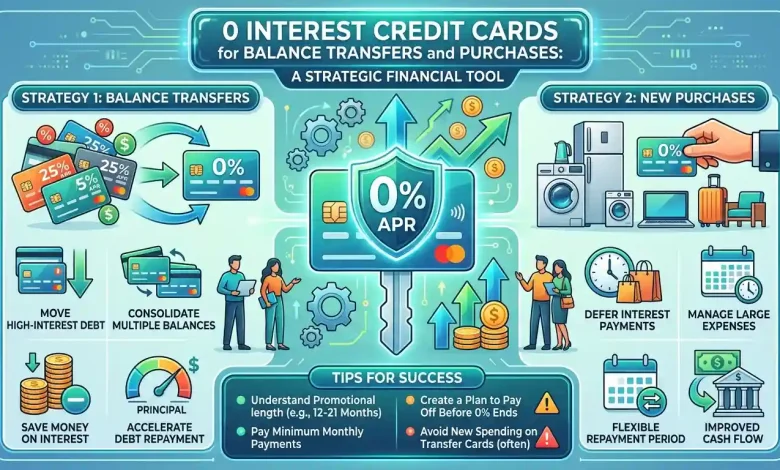

0 interest credit cards, often referred to as 0% APR (Annual Percentage Rate) credit cards, represent a powerful financial tool for consumers looking to manage debt, save money on interest, or finance large purchases without incurring immediate interest charges. These cards offer an introductory period, typically ranging from 6 to 21 months, during which no interest is charged on either new purchases, balance transfers, or sometimes both. Understanding how to effectively utilize these cards can lead to significant financial advantages, but it’s crucial to grasp their mechanics, potential pitfalls, and the strategic planning required to maximize their benefits.

What Are 0% APR Credit Cards?

At their core, 0 interest credit cards provide a temporary reprieve from interest payments. This introductory period, known as the promotional APR, allows cardholders to carry a balance without the typical interest accrual that can quickly escalate debt. After this period expires, the standard variable APR, which can be significantly higher, takes effect. These cards are primarily categorized by whether their 0% APR offer applies to balance transfers, new purchases, or both. For individuals struggling with high-interest credit card debt, a 0% APR balance transfer card can be a lifeline, offering a window to pay down debt principal without the burden of accumulating interest. Similarly, for those planning a large purchase, a 0% APR purchase card can provide flexibility, allowing them to pay off the item over several months without extra cost.

The allure of 0% interest is undeniable, but it’s essential to recognize that these are not “free money” cards. They are a tool for strategic financial management. Mismanaging a 0% APR card, such as failing to pay off the balance before the promotional period ends, can negate any potential savings and lead to substantial interest charges. Therefore, careful planning and disciplined repayment are paramount to leveraging these cards successfully. The terms and conditions, including the length of the introductory period, any balance transfer fees, and the post-promotional APR, are critical details that consumers must meticulously review before applying.

The Power of Balance Transfers: Escaping High-Interest Debt

One of the most compelling uses for a 0 interest credit card is for a balance transfer. A balance transfer involves moving debt from one or more high-interest credit cards to a new card that offers a 0% introductory APR. This strategy can be incredibly effective for individuals looking to consolidate debt and save a substantial amount of money on interest payments. The primary goal is to pay down as much of the principal as possible during the interest-free period.

For example, if you have a credit card with an outstanding balance of $5,000 and an APR of 20%, you could be paying hundreds of dollars in interest over a year. Transferring this balance to a card with a 0% introductory APR for 15 months means that every payment you make goes directly towards reducing your principal. This allows for faster debt repayment and significant savings. However, it’s crucial to be aware of balance transfer fees. Most 0% APR balance transfer cards charge a fee, typically ranging from 3% to 5% of the transferred amount. While this fee might seem like an added cost, it is often a small price to pay compared to the interest saved over many months.

Here’s a breakdown of how balance transfers work and what to consider:

- The Process: You apply for a new 0% APR balance transfer card. Once approved, you request to transfer balances from your existing credit cards. The new card issuer will typically pay off your old balances, and you will then owe the new card issuer.

- Introductory Period: This is the window (e.g., 12, 18, or 21 months) during which no interest accrues on the transferred balance.

- Balance Transfer Fees: As mentioned, expect a fee, usually 3-5% of the amount transferred. Factor this into your calculations to ensure the transfer is still beneficial.

- New Purchases: Some balance transfer cards only offer 0% APR on transfers, while new purchases may accrue interest at the standard rate immediately. It’s vital to check if the 0% APR applies to both or only transfers. If it doesn’t apply to purchases, it’s often advisable to avoid using the card for new spending to prevent mixing interest-bearing debt with your interest-free transferred balance.

- Repayment Plan: Develop a concrete plan to pay off the transferred balance before the introductory period ends. Divide the total balance by the number of months in the promotional period to determine your required monthly payment.

The strategic use of balance transfers demands discipline. If the balance isn’t paid off entirely by the end of the promotional period, the remaining amount will be subject to the card’s standard variable APR, which can be quite high. This can negate the initial savings and potentially leave you in a worse financial position if not managed effectively.

Navigating 0% APR on Purchases: Smart Spending and Saving

Beyond balance transfers, many 0 interest credit cards also offer a 0% introductory APR on new purchases. This feature can be incredibly advantageous for consumers planning significant expenditures, such as home appliances, medical bills, or holiday shopping. Instead of paying for these items outright or incurring immediate interest on a standard credit card, a 0% APR purchase card allows you to spread out the payments over several months without any additional cost.

Consider a situation where you need to buy a new refrigerator costing $1,500. With a 0% APR purchase card for 12 months, you could pay $125 per month for a year and pay no interest. On a regular credit card with a 20% APR, carrying that balance could cost you a significant amount in interest charges. This flexibility can help manage cash flow, especially for unexpected expenses or planned large purchases that might otherwise strain your budget.

Key aspects to consider for 0% APR on purchases:

- Budgeting for Repayment: Just like with balance transfers, it’s crucial to have a solid repayment plan. Calculate how much you need to pay each month to clear the balance before the promotional period ends.

- Avoiding Overspending: The temptation to spend more when there’s no immediate interest can be strong. However, remember that any unpaid balance will accrue interest at the standard rate once the promotional period expires. Stick to your budget and only purchase what you can realistically afford to pay off.

- Combined Offers: Some cards offer 0% APR on both balance transfers and purchases. These can be particularly versatile, but it’s important to understand if the promotional periods are the same length for both categories. Often, the purchase APR might differ or be shorter than the balance transfer APR.

- Minimum Payments: Always make at least the minimum payment on time. Missing a payment can not only incur late fees but also sometimes revoke your promotional APR, immediately subjecting your entire balance to the standard, higher interest rate.

Using a 0% APR purchase card wisely requires foresight and discipline. It’s an excellent tool for planned, budgetable expenses, but not a license for reckless spending. The goal is always to pay off the balance within the introductory period to avoid any interest charges.

Eligibility and the Application Process

To qualify for the best 0 interest credit cards, applicants generally need a strong credit score. Lenders typically look for individuals with a good to excellent credit history, which usually means a FICO score of 670 or higher. A robust credit score demonstrates to lenders that you are a reliable borrower who manages debt responsibly. Factors influencing your eligibility include your credit utilization ratio, payment history, length of credit history, and types of credit accounts.

When applying, lenders will perform a hard inquiry on your credit report, which can temporarily ding your credit score by a few points. Therefore, it’s advisable to apply for a card only when you are reasonably confident of approval. Before applying, consider checking your credit score and report to identify any inaccuracies and get a clear picture of your creditworthiness. Many credit card companies and financial websites offer pre-qualification tools that allow you to see if you’re likely to be approved without a hard inquiry, providing a useful preliminary check.

The application process itself typically involves:

- Researching Cards: Compare different 0% APR cards, focusing on introductory periods, balance transfer fees, and standard APRs after the promotional period.

- Gathering Information: You’ll need personal details like your name, address, Social Security number, income, and employment information.

- Submitting the Application: Most applications can be completed online in a few minutes.

- Approval and Activation: If approved, your card will be mailed to you. You’ll then need to activate it and, if applicable, initiate any balance transfers.

Remember that even with excellent credit, approval is not guaranteed, and the terms offered may vary based on the issuer’s assessment of your credit profile. Always read the fine print of the cardholder agreement carefully before accepting any offer.

| Feature/Card Type | 0% APR Balance Transfer Card | 0% APR Purchase Card | 0% APR Hybrid Card (BT & Purchases) |

|---|---|---|---|

| Primary Benefit | Debt consolidation, interest savings on existing debt | Interest-free financing for new expenses | Combines both benefits |

| Introductory Period (Avg.) | 12-21 months | 6-18 months | Often 12-18 months (may differ for BT vs. Purchases) |

| Typical Fees | 3-5% balance transfer fee | No purchase fee | 3-5% balance transfer fee |

| Ideal User For | High-interest debt holders | Those planning large purchases | Individuals with debt and upcoming large expenses |

| Key Warning | Must pay off before promo ends to avoid high APR on remaining balance | Avoid overspending; pay off before promo ends | Understand separate promo periods; avoid mixing interest-bearing debt |

Common Pitfalls and How to Avoid Them

While 0 interest credit cards offer significant advantages, they are not without their risks. Many consumers fall into common traps that can negate the benefits and even worsen their financial situation. Being aware of these pitfalls is the first step toward avoiding them.

- Missing the Repayment Deadline: The most significant pitfall is failing to pay off the balance before the 0% APR introductory period expires. Once this period ends, any remaining balance will be subject to the card’s standard variable APR, which can be as high as 20-30% or even more. To avoid this, mark your calendar with the end date of your promotional period and set up automatic reminders. Create a strict repayment plan and stick to it.

- Balance Transfer Fees: While small in comparison to long-term interest, these fees (typically 3-5%) can still add up, especially on large transfers. For a $10,000 transfer, a 3% fee is $300. Always factor this fee into your calculations to ensure the balance transfer is truly cost-effective.

- Using the Card for New Purchases (When 0% Doesn’t Apply): Some 0% APR balance transfer cards do not extend the promotional rate to new purchases. If you use such a card for new spending, those purchases will start accruing interest immediately at the standard (often high) APR. This can create a confusing and costly mix of interest-free and interest-bearing debt. If your card doesn’t offer 0% on purchases, consider using a different card for everyday spending or avoid new purchases altogether during the promotional period.

- Minimum Payments Only: While paying only the minimum payment keeps your account in good standing, it will likely not be enough to pay off your balance before the 0% APR period ends. This leaves you vulnerable to high interest charges on the remaining balance. Always aim to pay more than the minimum, ideally enough to clear the debt entirely.

- Late Payments: A single late payment can have severe consequences. Many card issuers will revoke your promotional 0% APR if you make a late payment, immediately applying the standard variable APR to your entire balance. This can also incur late fees and negatively impact your credit score. Set up automatic payments to ensure you never miss a deadline.

- New Debt Accumulation: For those using a balance transfer card, it’s crucial to stop using the old, high-interest cards for new purchases. If you transfer a balance only to rack up new debt on your old cards, you haven’t solved the underlying problem, and you’ll find yourself deeper in debt. Cut up or lock away the old cards until the transferred balance is paid off.

Choosing the Right 0% Interest Card: Factors to Consider

Selecting the optimal 0 interest credit card requires careful consideration of your specific financial situation and goals. Not all 0% APR cards are created equal, and the “best” card for one person might be entirely unsuitable for another. Here are the critical factors to evaluate:

- Your Goal (Balance Transfer vs. Purchases):

- If your primary goal is to pay down existing high-interest debt, prioritize cards with long 0% APR periods on balance transfers.

- If you plan a large purchase and want to spread out payments without interest, focus on cards offering a long 0% APR on new purchases.

- If you need both, look for a hybrid card, but be mindful that the promotional periods for transfers and purchases might differ.

- Length of the Introductory Period: This is arguably the most crucial factor. A longer 0% APR period gives you more time to pay off your balance interest-free. Introductory periods can range from 6 months to 21 months or even longer. Choose a period that realistically allows you to meet your repayment goals.

- Balance Transfer Fees: If you’re planning a balance transfer, compare the fees. While most are 3-5%, some cards occasionally offer lower fees or even no balance transfer fee (though these are rarer and often come with shorter introductory periods). Calculate the total cost, including the fee, to ensure it’s still a net saving over your current interest payments.

- Standard APR After the Promotional Period: While you aim to pay off your balance before the 0% APR ends, it’s wise to know what the regular APR will be. If you anticipate carrying a small balance past the introductory period, a lower standard APR will be beneficial.

- Credit Score Requirements: Different cards cater to different credit profiles. Be realistic about your credit score and apply for cards for which you have a strong chance of approval. Applying for too many cards or cards for which you are underqualified can negatively impact your credit score.

- Annual Fee: Most 0% APR cards do not have an annual fee, but some premium cards might. If a card has an annual fee, ensure the benefits (e.g., longer 0% APR period, rewards) outweigh this cost.

- Rewards Programs: Some 0% APR cards also offer rewards (cash back, points, miles). While rewards are a nice bonus, they should be secondary to the primary goal of interest-free debt repayment or purchase financing. Don’t let rewards distract you from your main objective.

- Other Perks: Look for additional features that might be valuable, such as extended warranty protection, purchase protection, or travel benefits, although these are typically less common on basic 0% APR cards.

Utilize online comparison tools and read reviews from reputable financial publications to help narrow down your choices. Always review the cardholder agreement thoroughly before committing.

Maximizing the Benefits of Your 0% APR Period

Once you’ve secured a 0 interest credit card, the real work begins. Strategic management during the introductory period is key to fully realizing its financial advantages. Here’s how to maximize your benefits:

- Create a Strict Repayment Plan:

- For balance transfers: Divide the total transferred balance (plus any transfer fee) by the number of months in your 0% APR period. This gives you the minimum amount you need to pay each month to clear the debt interest-free. For instance, a $5,000 balance with a 3% fee ($150) and an 18-month promotional period means you need to pay approximately $286 per month ($5150 / 18).

- For purchases: Estimate your total planned purchases and divide by the number of months in the 0% APR purchase period.

- Aim to pay more than this calculated amount if possible, to build a buffer or pay it off even faster.

- Set Up Automatic Payments: This is crucial. Automating your monthly payments for at least the calculated amount ensures you never miss a payment. Missing a payment can revoke your promotional APR and incur late fees, undermining your entire strategy.

- Avoid New Debt (Especially on Balance Transfer Cards): If you’ve transferred a balance, resist the urge to use your old cards or even the new 0% APR card for new purchases unless the 0% APR explicitly covers them. The goal is to eliminate existing debt, not add to it.

- Monitor Your Progress: Regularly review your credit card statements and track your repayment progress. Ensure you’re on track to pay off the balance before the promotional period ends.

- Understand the End Date: Clearly mark the end date of your 0% APR period on a calendar or set multiple reminders. Knowing this date precisely will help you make final large payments if necessary or prepare for the standard APR.

- Consider a Second Balance Transfer (If Necessary): If you find you won’t be able to pay off the entire balance before the 0% APR period ends, and you still have a significant amount remaining, you might consider applying for another 0% APR balance transfer card. However, this should be a last resort and carefully considered, as it incurs another balance transfer fee and extends the debt repayment cycle. This is generally not recommended as a primary strategy and should only be undertaken if your financial situation has genuinely improved and you’re committed to paying off the new transfer.

By diligently adhering to these strategies, consumers can transform 0 interest credit cards from a temporary relief into a powerful instrument for achieving financial freedom from high-interest debt and managing large expenses effectively. For additional reliable insights on credit card management and consumer finance, the Consumer Financial Protection Bureau’s (CFPB) credit card tools offer valuable information and guidance.

Conclusion

0 interest credit cards for balance transfers and purchases are more than just a marketing gimmick; they are sophisticated financial tools that, when used correctly, can provide immense value. They offer a unique opportunity to save significant amounts on interest, consolidate high-interest debt, and manage large purchases without immediate financial strain. However, their effectiveness hinges entirely on responsible usage and meticulous planning. Understanding the terms, avoiding common pitfalls, and diligently executing a repayment strategy are paramount. By doing so, individuals can strategically leverage these cards to improve their financial health, reduce debt burdens, and build a stronger foundation for their future. The key lies not just in acquiring such a card, but in mastering its disciplined application to achieve your financial objectives.