7 Essential Credit Card Tips for Beginners – Build Credit & Save

Table of Contents

A Credit Card Guide for Beginners is an essential resource for anyone looking to navigate the often complex world of personal finance. For many, a credit card represents their first significant step into managing credit, offering both incredible convenience and potential pitfalls. Understanding how credit cards function, their benefits, and their associated risks is paramount to building a strong financial foundation. Used wisely, a credit card can be a powerful tool for financial flexibility, emergency preparedness, and establishing a positive credit history, which is crucial for future financial endeavors like securing loans for a home or car. However, misused, it can lead to accumulating debt, high interest charges, and a damaged credit score, making sound financial decisions much harder in the long run. This comprehensive guide aims to demystify credit cards, providing beginners with all the knowledge they need to use them responsibly and effectively from the very beginning.

What is a Credit Card and How Does It Work?

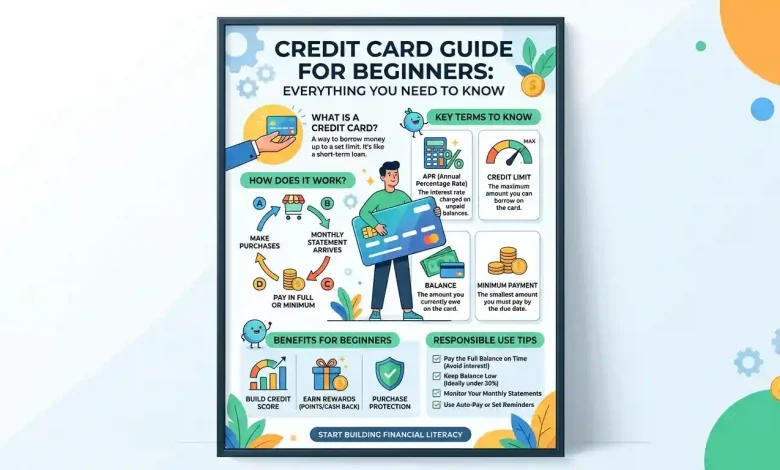

At its core, a credit card is a payment card that grants you access to a revolving line of credit extended by a financial institution, such as a bank or credit union. Unlike a debit card, which directly draws funds from your checking account, a credit card allows you to borrow money up to a pre-set limit to make purchases, pay bills, or even get cash advances. When you use your credit card, the amount of your purchase is added to your outstanding balance, reducing your available credit. You are essentially making a short-term loan that you commit to repay.

The mechanics behind a credit card transaction involve several key players: you (the cardholder), the merchant, the acquiring bank (the merchant’s bank), the payment network (e.g., Visa, Mastercard, American Express, Discover), and the issuing bank (your credit card provider). When you swipe, tap, or enter your card details, your account information is sent to the merchant’s bank, then to the payment network, and finally to your issuing bank for authorization. If approved, the funds are transferred to the merchant, and the purchase amount is added to your credit card balance.

Each month, you receive a statement detailing your purchases, current balance, minimum payment due, and payment due date. You have a grace period, typically between the end of your billing cycle and the payment due date, during which you can pay your full balance without incurring interest charges. If you pay the entire statement balance by the due date, you pay no interest on those purchases. However, if you carry a balance – meaning you pay less than the full amount – interest is charged on the remaining balance. This interest is typically expressed as an Annual Percentage Rate (APR) and can be quite high, causing your debt to grow quickly if not managed carefully. Responsible use, characterized by on-time, full payments, is crucial for leveraging the benefits of credit cards.

Understanding Your Credit Score: The Foundation of Credit

Your credit score is a numerical representation of your creditworthiness, essentially a grade reflecting your credit report. It’s a three-digit number, typically ranging from 300 to 850, that lenders use to assess the risk of lending you money. A higher credit score indicates to lenders that you are a reliable borrower who is likely to repay debts on time, which can lead to better loan terms, lower interest rates, and higher credit limits. Conversely, a low credit score can make it difficult to obtain loans, secure favorable interest rates, or even rent an apartment.

Several factors contribute to your credit score, with payment history being the most significant, accounting for approximately 35% of your FICO Score, the most widely used credit scoring model. Making payments on time, every time, is paramount to building and maintaining good credit. Another crucial factor is your credit utilization ratio (CUR), which is the amount of credit you’re using compared to your total available credit. Experts generally recommend keeping your credit utilization below 30% of your credit limit to positively impact your score. Length of credit history, credit mix (having different types of credit like revolving and installment loans), and new credit inquiries also play a role in your score.

Building a good credit score takes time and consistent responsible behavior. It’s advisable to regularly check your credit report for errors and to monitor your score. You can obtain one free credit report each year from each of the three major credit reporting agencies: Equifax, Experian, and TransUnion, through AnnualCreditReport.com. Understanding and proactively managing these elements will set a strong financial foundation.

Types of Credit Cards: Finding the Right Fit

For beginners, selecting the right credit card is a critical decision that can significantly influence their credit-building journey. There isn’t a one-size-fits-all answer, as different cards cater to different needs and financial situations. Understanding the various types available for first-time cardholders can help you choose wisely.

Secured Credit Cards

Secured credit cards are often recommended for those with no credit history or poor credit. These cards require a refundable security deposit, which typically becomes your credit limit. For example, a $200 deposit would mean a $200 credit limit. This deposit acts as collateral, reducing the risk for the card issuer and making it easier for individuals with limited credit to qualify. By using a secured card responsibly – making on-time payments and keeping balances low – you can establish a positive credit history, often leading to an upgrade to an unsecured card and the return of your deposit over time.

Student Credit Cards

Designed specifically for enrolled college students, student credit cards often come with benefits tailored to student life, such as cash back on everyday purchases and sometimes lower annual fees. These cards aim to help students build healthy credit habits early on, often with more lenient income requirements than standard unsecured cards. While some may require a limited credit history, many are accessible to those just starting out.

Unsecured Starter Cards

These are standard credit cards that do not require a security deposit. While generally harder to qualify for without an existing credit history, some issuers offer unsecured starter cards specifically for first-time cardholders or those with fair credit. They typically come with lower credit limits (e.g., $300-$500) and may have higher APRs compared to cards for individuals with established good credit. Responsible use of an unsecured starter card is crucial for demonstrating creditworthiness and can pave the way for more premium cards in the future.

Authorized User Status

Becoming an authorized user on a parent’s or guardian’s existing credit card account is another way to begin building credit history. As an authorized user, you receive a card to use, and the account activity is typically reported to your credit report. The primary account holder remains legally responsible for all payments, but their responsible usage can positively impact your credit score. This option can be a valuable stepping stone, allowing you to benefit from someone else’s good credit practices without the full responsibility of a primary account.

When choosing your first credit card, consider your financial goals. Look for cards with low or no annual fees, reasonable interest rates (especially if you anticipate carrying a balance), and features like rewards programs that align with your spending habits.

| Credit Card Type | Description | Best For | Key Feature for Beginners |

|---|---|---|---|

| Secured Credit Card | Requires a refundable security deposit that acts as your credit limit. | Individuals with no credit history or bad credit. | Easiest to get approved for, helps build credit safely. |

| Student Credit Card | Designed for college students; may offer student-friendly rewards and terms. | Enrolled college students with limited or no credit. | Lower income eligibility, focuses on building credit habits. |

| Unsecured Starter Card | Standard credit card, no deposit, but often has lower limits. | Beginners with some, albeit limited, credit history or steady income. | No deposit required, can offer basic rewards. |

| Authorized User | Added to someone else’s existing account; benefits from their credit history. | Young individuals (under 18 or 21) or those wanting to piggyback on good credit. | Builds credit without full primary responsibility. |

Applying for Your First Credit Card: Steps and Tips

Applying for your first credit card is an important financial milestone. While the process is generally straightforward, it’s crucial to approach it strategically, especially when you have limited or no credit history.

Before You Apply

Before submitting an application, take some time to assess your financial situation. Ensure you have a stable source of income, as card issuers will require proof that you can make payments. If you’re under 21, issuers typically require proof of independent income, or you may need a cosigner. It’s also wise to understand your goals: are you primarily looking to build credit, earn rewards, or have a card for emergencies? This will help you narrow down the best card type.

The Application Process

You can apply for a credit card through your bank, credit union, or directly with credit card companies online. Many beginners find success starting with their current bank or credit union, as they may have existing relationships that could aid in approval. The application form will typically ask for your full legal name, date of birth, current address, Social Security number, gross annual income, and employer information.

When you apply, the issuer will perform a “hard inquiry” on your credit report, which can cause a minor, temporary dip in your credit score. For this reason, it’s advisable to limit the number of applications you submit within a short period. Research thoroughly and apply for the card you believe you have the best chance of being approved for. Some issuers offer pre-qualification or pre-approval tools that involve a “soft inquiry” (which doesn’t affect your score) to give you an idea of your likelihood of approval before a formal application.

Tips for Success

- Start with a Beginner-Friendly Card: As discussed, secured cards or student cards are often the most accessible for those with no credit history.

- Be Honest About Your Income: Provide accurate income information. Inflating your income can lead to issues later.

- Review Terms and Conditions: Understand the APR, annual fees, and any other charges before you commit.

- Consider a Cosigner: If you’re struggling to get approved on your own, a trusted individual with good credit (like a parent) can cosign, increasing your chances of approval.

Managing Your Credit Card Responsibly: Best Practices

Once you’ve obtained your first credit card, the real work begins: learning to manage it responsibly. Responsible credit card management is key to building a strong credit history and avoiding the pitfalls of debt.

Pay Your Bills On Time, Every Time

This is arguably the most critical aspect of credit card management. Your payment history accounts for 35% of your FICO score, making on-time payments paramount. Late payments can incur hefty fees, increase your interest rate, and severely damage your credit score, potentially staying on your report for up to seven years. To ensure timely payments, consider setting up automatic payments through your bank or the card issuer.

Pay Your Full Balance to Avoid Interest

If you pay your entire statement balance by the due date each month, you can avoid paying any interest on your purchases. This is the ideal scenario for using a credit card. Interest is the cost of borrowing money, and credit card APRs can be very high, causing your debt to snowball quickly if you only make minimum payments. While making the minimum payment keeps your account in good standing, it will prolong your debt and cost you significantly more in interest over time.

Keep Your Credit Utilization Low

As mentioned, your credit utilization ratio (CUR) is the amount of credit you use compared to your total available credit. Lenders prefer to see this ratio below 30%. For instance, if your credit limit is $1,000, try to keep your balance below $300. A low CUR demonstrates that you are not overly reliant on borrowed money and can manage your credit effectively. One way to maintain a low ratio is to make multiple payments throughout the billing cycle, rather than waiting for the statement due date.

Monitor Your Statements and Credit Report

Regularly review your monthly statements for any unauthorized transactions or errors. Promptly report any suspicious activity to your credit card issuer, as most cards offer fraud protection, meaning you won’t be liable for unauthorized charges. Additionally, regularly checking your credit report (which you can do for free annually) allows you to catch errors or potential signs of identity theft that could negatively impact your score.

Set a Budget and Stick to It

A credit card limit is not a spending target. Create and adhere to a personal budget to ensure you only spend what you can afford to pay back. Credit cards can make it easy to overspend, as the money doesn’t feel “real” until the bill arrives. Use your credit card as a convenient payment tool, not as an extension of your income or a means to buy things you cannot afford.

Common Credit Card Fees and How to Avoid Them

While credit cards offer numerous benefits, they also come with various fees that can quickly add up if you’re not careful. Understanding these common charges and how to avoid them is an essential part of responsible credit card management.

Annual Fees

Some credit cards, particularly premium rewards cards or certain secured cards, charge a yearly fee for the privilege of using the card. These fees can range from modest amounts to several hundred dollars.

How to avoid: Many excellent credit cards have no annual fees. If you choose a card with an annual fee, ensure the benefits (like rewards or travel perks) outweigh the cost. You can also try calling your issuer to ask if they can waive the fee or offer a retention bonus.

Interest/Finance Charges

These are the fees charged on any outstanding balance you carry from one billing cycle to the next. Your Annual Percentage Rate (APR) determines how much interest you pay.

How to avoid: The most effective way is to pay your entire statement balance in full by the due date every month. Many cards also offer introductory 0% APR periods, which can be useful if you need to finance a large purchase, but remember that the regular APR will kick in after the promotional period ends.

Late Payment Fees

If you fail to make at least the minimum payment by your card’s due date, you will be charged a late fee. These fees can range from $25 to nearly $40, and consistent late payments can also lead to a penalty APR.

How to avoid: Always pay your bills on time. Set up automatic payments or calendar reminders to ensure you never miss a due date.

Cash Advance Fees

A cash advance is when you use your credit card to withdraw cash from an ATM or get cash over the counter. These transactions typically incur a fee, often 3% to 5% of the amount, and interest often starts accruing immediately at a higher rate than for purchases.

How to avoid: Avoid cash advances whenever possible. Use an emergency fund or savings account for cash needs instead.

Foreign Transaction Fees

Some credit cards charge a fee (typically 1-3% of the transaction amount) when you make a purchase in a foreign currency or if the transaction is processed by a foreign bank, even if you’re shopping online from your home country.

How to avoid: If you travel internationally or shop frequently from foreign websites, choose a credit card that specifically advertises no foreign transaction fees.

Balance Transfer Fees

When you transfer a balance from one credit card to another, usually to consolidate debt or take advantage of a lower interest rate, you’ll often be charged a balance transfer fee, typically 3% to 5% of the transferred amount.

How to avoid: Compare balance transfer offers carefully. Some cards occasionally offer promotional periods with no balance transfer fees, or you might find a card with a lower fee. Always calculate if the savings from lower interest outweigh the transfer fee.

Building Good Credit Habits for a Strong Financial Future

Beyond understanding the mechanics and avoiding fees, cultivating sound financial habits is what truly transforms a credit card from a potential burden into a powerful asset. These habits contribute significantly to a healthy credit score and overall financial well-being.

- Budgeting and Mindful Spending: Develop a strict budget and stick to it. Only charge what you can comfortably afford to pay off in full each month. This prevents overspending and ensures you don’t accumulate expensive interest.

- Automate Payments: Set up automatic payments for at least the minimum amount due. This safeguards your payment history, the most impactful factor in your credit score, against accidental oversight. Ideally, automate the full statement balance if your income allows.

- Keep Credit Utilization Low: As previously emphasized, maintaining your credit utilization ratio below 30% is critical. If your limit is $500, try to keep your balance under $150. Consider making multiple smaller payments throughout the month to keep your balance consistently low.

- Regularly Check Your Credit Reports and Statements: Be proactive in monitoring your financial health. Review your monthly statements for accuracy and any fraudulent activity. Annually, pull your free credit reports from all three bureaus to check for errors or signs of identity theft.

- Avoid Opening Too Many New Accounts: While a credit mix is beneficial, applying for too many credit cards in a short period can negatively impact your score due to multiple hard inquiries and potentially a shorter average age of accounts. Only open new credit lines when necessary and when you are confident you can manage them responsibly.

- Build an Emergency Fund: Having an emergency fund provides a financial cushion, reducing the temptation to rely on your credit card for unexpected expenses. This helps prevent accumulating debt when unforeseen costs arise.

- Understand Interest Rates: Always be aware of your card’s APR, especially if you anticipate carrying a balance. Knowledge of how interest is calculated empowers you to make informed decisions and avoid unnecessary costs.

By integrating these habits into your financial routine, you can effectively harness the power of credit cards to build a robust credit history, enhance your financial flexibility, and achieve long-term financial stability. Credit cards, when used wisely, are not just for spending; they are tools for demonstrating financial responsibility and opening doors to future opportunities.

Conclusion

Embarking on your credit card journey as a beginner can feel daunting, but with the right knowledge and a commitment to responsible financial practices, it can be an incredibly rewarding experience. This Credit Card Guide for Beginners has illuminated the fundamental concepts, from how a credit card operates and its impact on your credit score, to the diverse types of cards available and the application process. We’ve also delved into the critical practices of managing your card responsibly, emphasizing the importance of on-time, full payments and maintaining a low credit utilization ratio.

The benefits of using credit cards wisely extend far beyond mere purchasing power; they include enhanced fraud protection, the ability to build a positive credit history essential for future loans, and often valuable rewards programs. Conversely, the risks of high interest rates and accumulating debt underscore the importance of vigilance and discipline. By understanding common fees and actively working to avoid them, you can maximize the advantages of your credit card while minimizing its potential drawbacks.

Ultimately, a credit card is a powerful financial instrument. Approaching it with education, caution, and a dedication to sound money management will enable you to build a strong credit foundation, paving the way for greater financial freedom and security in your future. Remember, every on-time payment and responsible spending decision contributes to your financial reputation, making your credit card a true tool for success.