6 Powerful Credit Card Transfer Tips – Manage Balances & Payments Smartly

Table of Contents

Credit card transfer, commonly known as a balance transfer, is a powerful financial tool designed to help consumers manage and reduce high-interest credit card debt. In essence, it involves moving an existing debt from one or more credit card accounts to a new credit card, typically one offering a lower or 0% introductory Annual Percentage Rate (APR) for a limited period. This strategy can be particularly appealing given the current financial landscape; according to the Federal Reserve Bank of New York, total credit card debt in the U.S. stood at $1.25 trillion in the first quarter of 2026. With the average credit card interest rate on accounts assessing interest at 21.52% in February 2026, finding ways to reduce interest payments is more crucial than ever. This comprehensive guide will walk you through everything you need to know about credit card balance transfers, from understanding their mechanics to effectively utilizing them for debt management.

Understanding Credit Card Balance Transfers

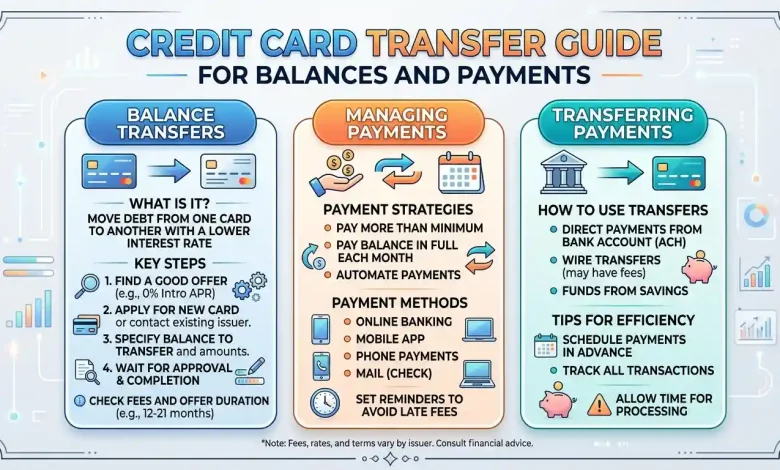

A credit card balance transfer allows you to consolidate existing credit card or loan balances onto a new credit card account. The primary motivation behind such a transfer is to take advantage of a lower interest rate, often an introductory 0% APR, offered by the new card. This promotional period, which can range from 6 to 21 months or even longer, provides a window during which your payments go almost entirely towards reducing the principal balance, rather than being eroded by interest charges.

It’s important to understand that a balance transfer does not eliminate your debt; it merely relocates it. The goal is to create a more manageable repayment environment, allowing you to pay off your debt faster and save a significant amount of money on interest.

Why Consider a Balance Transfer?

There are several compelling reasons why a balance transfer might be a smart financial move, particularly if you’re grappling with high-interest credit card debt.

- Save on Interest: This is arguably the biggest benefit. By transferring a high-interest balance to a card with a 0% introductory APR, you can halt the accrual of new interest for the promotional period. This means every dollar you pay goes directly towards chipping away at your principal debt, accelerating your payoff journey and potentially saving you hundreds or even thousands of dollars.

- Consolidate Debt: If you’re juggling multiple credit card payments with different due dates and varying interest rates, a balance transfer can simplify your financial life. Consolidating several balances onto one card means you only have one monthly payment to track, reducing the risk of missed payments and the associated fees and credit score damage.

- Faster Debt Payoff: Without interest eating into your payments, you can pay down your principal balance much more quickly. This psychological boost can be incredibly motivating, helping you stay committed to your debt repayment plan.

- Financial Reset: A balance transfer can offer a fresh start, providing the breathing room needed to implement better financial habits and budgeting strategies. It gives you an opportunity to re-evaluate your spending and ensure you don’t accumulate new debt.

How Does a Balance Transfer Work?

The process of a credit card balance transfer typically involves a few key steps:

- Identify Your Debt: First, pinpoint the high-interest credit card balances you wish to transfer. Note down the current balances, account numbers, and the Annual Percentage Rates (APRs) of these cards.

- Find a Balance Transfer Card: Research and compare credit cards specifically designed for balance transfers. Look for cards offering a low or 0% introductory APR for a substantial period, and carefully review any associated balance transfer fees. Many cards offer 0% intro APR for 15-21 months on balance transfers.

- Check Your Credit Score: To qualify for the most favorable balance transfer offers, typically those with long 0% APR periods and lower fees, you’ll generally need good to excellent credit (a FICO score of 670 or higher). Checking your score beforehand gives you an idea of your approval odds.

- Apply for the New Card: Once you’ve chosen a card, submit an application. You’ll need to provide personal and financial information, including your Social Security number, income, and details of the accounts you intend to transfer. The credit card company will perform a hard inquiry on your credit report, which can cause a slight, temporary dip in your credit score.

- Request the Transfer: If approved, you can then initiate the balance transfer. This typically involves providing the new credit card issuer with the account numbers, creditor names, and the amounts you wish to transfer from your old cards. Some issuers may provide checks that you can use to pay off your old balances, while others will directly transfer the funds to your previous lenders.

- Continue Payments on Old Card: It is crucial to continue making at least the minimum payments on your old accounts until you verify that the balance transfer is complete and the funds have been credited. This prevents late fees and protects your credit score.

- Monitor and Pay Down: Once the transfer is complete, your new card will show the consolidated balance, along with any balance transfer fees. Now, your focus should be on diligently paying down the transferred amount before the introductory APR period expires.

Finding the Right Balance Transfer Offer

Selecting the appropriate balance transfer card is critical to the success of your debt reduction strategy. Several factors come into play:

- Introductory APR Period: This is the most attractive feature. Look for cards offering the longest possible 0% or low introductory APR on balance transfers. Periods can range from 12 to 21 months, providing ample time to tackle your debt.

- Balance Transfer Fees: Most balance transfer cards charge a fee, typically ranging from 3% to 5% of the transferred amount, with a minimum fee (e.g., $5 or $10). For example, transferring a $10,000 balance with a 3% fee would add $300 to your new balance. Some rare offers might have no balance transfer fee, but these often come with shorter intro periods. Always calculate if the interest saved outweighs the fee.

- Regular APR: While the introductory rate is important, don’t overlook the standard APR that kicks in after the promotional period. If you anticipate not paying off the entire balance within the intro period, a lower regular APR will save you money in the long run.

- Credit Limit: Ensure the new card offers a credit limit sufficient to cover the balance you intend to transfer. Some issuers may cap balance transfers at a certain percentage of your credit limit.

- No Same-Issuer Transfers: A crucial rule to remember is that most banks do not allow you to transfer a balance from one card they own to another card they also own. You’ll typically need to transfer debt between cards from different issuers.

Here’s a comparison of some hypothetical balance transfer card features to illustrate the considerations:

| Card Feature | Card A: “Long Horizon” | Card B: “Low Fee” | Card C: “Hybrid Rewards” |

|---|---|---|---|

| Introductory 0% APR on Balance Transfers | 21 months | 12 months | 15 months |

| Balance Transfer Fee | 5% ($5 minimum) | 3% ($5 minimum) | 3% ($5 minimum) |

| Standard APR (Variable) | 17.49% – 28.24% | 18.99% – 27.99% | 18.24% – 27.74% |

| Introductory 0% APR on Purchases | 21 months | 6 months | 15 months |

| Additional Perks | Cellphone Protection (hypothetical) | No Annual Fee | Cash Back Rewards (e.g., 1.5% – 5%) |

| Best For | Maximizing interest-free time on large balances | Saving on upfront transfer costs | Balancing debt payoff with new purchases & rewards |

The Application Process

Applying for a balance transfer credit card is similar to applying for any new credit card. You’ll submit an application form, either online or in person, providing your personal and financial details. The issuer will then evaluate your creditworthiness, including your credit reports and credit scores.

As mentioned, a hard inquiry will be placed on your credit report. This inquiry can cause a temporary, minor dip in your credit score, usually by a few points, and typically remains on your report for up to two years. While a single inquiry usually isn’t a major concern, multiple hard inquiries in a short period could signal higher risk to lenders and further impact your score.

If your application is approved, the new credit card company will guide you through initiating the balance transfer. Ensure you have all the necessary information for your existing accounts readily available to streamline this process.

Navigating the Balance Transfer Period

Once your balance has been successfully transferred to the new card, the real work begins. To maximize the benefits of your balance transfer, it’s crucial to have a clear and disciplined repayment strategy.

- Make a Payoff Plan: Calculate how much you need to pay each month to eliminate the transferred balance entirely before the introductory APR expires. This amount will likely be higher than the minimum payment requested by the card issuer, but adhering to it will save you significant interest. Many online calculators can help you determine the ideal monthly payment.

- Avoid New Purchases: Resist the temptation to use your new balance transfer card for new purchases, especially if the 0% APR only applies to transfers and not new spending. Even if new purchases also have a promotional APR, adding new debt can defeat the purpose of the transfer and make it harder to pay off your original balance. Focus solely on paying down the transferred debt.

- Don’t Close Old Accounts Immediately: While it might seem intuitive to close the old credit card accounts once their balances are transferred, doing so can actually negatively impact your credit score. Keeping old accounts open, even with a zero balance, helps maintain a longer credit history and can keep your credit utilization ratio (the amount of credit you’re using compared to your total available credit) low. A lower utilization rate generally benefits your credit score.

- Set Reminders: Mark the end date of your introductory APR period prominently in your calendar. Knowing exactly when the standard APR kicks in will help you adjust your payments accordingly or explore other options if you haven’t paid off the entire balance.

- Automate Payments: Setting up automatic monthly payments ensures you never miss a due date. Late payments can result in fees and, more importantly, could cause you to lose your promotional APR, reverting to a much higher interest rate.

Potential Pitfalls and How to Avoid Them

While a balance transfer can be an excellent debt management tool, it’s not without its risks. Being aware of these potential pitfalls can help you navigate the process successfully.

- Accruing New Debt: One of the biggest dangers is viewing the balance transfer as a “get out of jail free” card. If you transfer a balance only to accumulate new debt on either the old or new card, you could end up in a worse financial position than before. The key is discipline and a commitment to changing spending habits.

- Balance Transfer Fees: As discussed, these fees can add to your total debt. Always factor the fee into your calculations to ensure the transfer is genuinely cost-effective. A $5,000 transfer with a 3% fee means you start with a $5,150 balance.

- Expiration of Introductory APR: The low or 0% APR is temporary. If you still have a balance when the promotional period ends, the remaining debt will start accruing interest at the much higher standard APR. This could lead to higher minimum payments and erase any savings you initially gained.

- Credit Score Impact: While a balance transfer can eventually help your credit score by reducing your credit utilization and making on-time payments easier, the initial hard inquiry and potentially reduced average age of accounts can cause a temporary dip. Repeatedly opening new credit cards and transferring balances without paying them down can damage your credit score long-term.

- Limited Transfer Amounts: Your new credit card may not offer a high enough credit limit to transfer your entire debt, leaving you with residual high-interest balances on your old cards. Plan for this possibility and prioritize transferring the highest-APR balances first.

- Missing Payments: Missing a payment on your new balance transfer card can trigger penalties, including the loss of your promotional APR and the imposition of a penalty APR, which is often very high. This would negate the primary benefit of the transfer.

To mitigate these risks, a solid repayment plan and disciplined spending habits are paramount. Understanding your financial situation and being realistic about your ability to pay off the debt within the promotional period is key to a successful balance transfer. For more general advice on managing credit and debt responsibly, resources like Wikipedia offer broad insights into credit cards and financial literacy. Wikipedia

Conclusion

A credit card balance transfer can be a highly effective strategy for taking control of high-interest debt and achieving financial freedom. By moving your balances to a card with a lower or 0% introductory APR, you create a crucial window to pay down your principal without the burden of accumulating interest. This can lead to significant savings and a faster path to becoming debt-free.

However, the success of a balance transfer hinges on careful planning and disciplined execution. It requires thorough research into card offers, understanding the associated fees, and, most importantly, a commitment to a strict repayment plan. Avoid the temptation to accrue new debt and use the promotional period strategically to eliminate your existing obligations. When utilized wisely, a credit card balance transfer is not just a temporary fix but a powerful step towards building a healthier financial future. Remember, the goal is not merely to move debt, but to make a deliberate plan to pay it off entirely.