6 Powerful Secured Credit Card Tips – Build Your Credit History Fast

Table of Contents

Secured credit cards serve as a crucial financial tool for individuals looking to establish or rebuild their credit history. Many people find themselves in a position where they have no credit history, perhaps due to being young and new to the financial system, or they may have a poor credit score from past financial missteps. In either scenario, traditional unsecured credit cards can be difficult to obtain, leaving individuals searching for an accessible pathway to financial credibility. This comprehensive guide will explore the intricacies of secured credit cards, how they function as credit-building instruments, and the best practices for leveraging them to achieve a strong financial standing.

What is a Secured Credit Card?

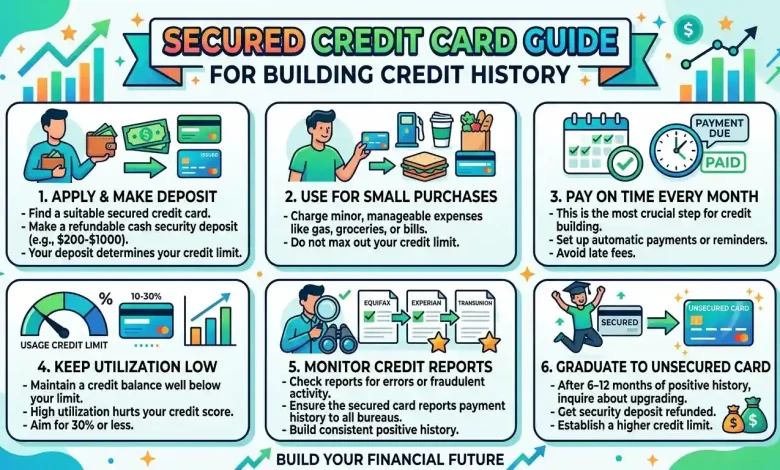

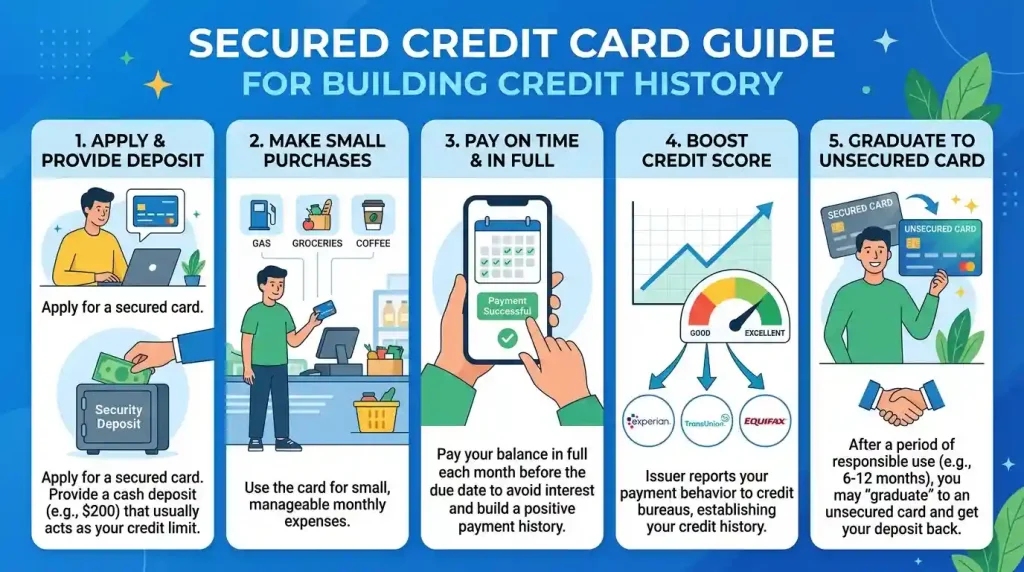

A secured credit card operates much like a traditional credit card, with one fundamental difference: it requires a security deposit. This deposit, typically ranging from $200 to $500, serves as collateral for the credit card issuer. In most cases, the amount of your deposit directly determines your credit limit. For example, if you deposit $300, your credit limit will generally be $300. This deposit mitigates the risk for the lender, making secured cards more accessible to individuals with limited or poor credit histories.

Unlike a debit card, where you spend your own money directly, a secured credit card still allows you to borrow against a credit line, even though it’s backed by your own funds. You receive monthly statements and are expected to make payments towards your balance, just as you would with an unsecured card. The critical aspect of a secured card for credit building is that its activity is usually reported to the major credit bureaus: Equifax, Experian, and TransUnion. This reporting is what enables you to build a payment history and establish a credit profile. The security deposit is typically refundable when you close the account or transition to an unsecured card, provided your balance is paid in full.

How Secured Credit Cards Build Credit

The power of a secured credit card in building credit lies primarily in how your usage is reported to credit bureaus. Credit scores are influenced by several factors, with payment history and credit utilization being the most significant.

- Payment History (35% of FICO Score): Making on-time payments consistently is paramount. Each month you pay your bill by the due date, a positive entry is added to your credit report. Over time, this establishes a reliable payment history, which is a strong indicator of your creditworthiness to future lenders. Conversely, late or missed payments can severely damage your credit score.

- Credit Utilization (30% of FICO Score): This refers to the amount of credit you are using compared to your total available credit, expressed as a percentage. Keeping your credit utilization ratio low, ideally below 30%, demonstrates responsible credit management. For instance, if your secured card has a $300 credit limit, you should aim to keep your balance below $90. A lower utilization ratio indicates that you are not overly reliant on borrowed funds, which lenders prefer to see.

- Length of Credit History: While a secured card is often a starting point, the longer you maintain the account in good standing, the more positively it impacts your credit score. It contributes to the overall length of your credit history, which is another factor in credit scoring.

- Types of Credit Used: Having a mix of credit types, such as revolving credit (like credit cards) and installment loans, can also be beneficial. A secured credit card provides that initial revolving credit experience.

- New Credit: While opening new accounts can sometimes temporarily ding your score, a secured card is a strategic move to initiate positive credit building, and its benefits often outweigh any minor initial impact.

Most people can begin to see improvements in their credit score within three to six months of responsible use, with FICO scores typically requiring at least six months of history to be generated if starting from scratch.

Secured vs. Unsecured: Understanding the Difference

The primary distinction between secured and unsecured credit cards lies in the collateral requirement. Unsecured credit cards, which are what most people think of as “traditional” credit cards, do not require an upfront security deposit. Instead, approval for an unsecured card is based on your creditworthiness, income, and debt-to-income ratio. Lenders take on more risk with unsecured cards, hence the stricter approval criteria, which often demand a good to excellent credit score.

Here’s a comparison of key differences:

| Feature | Secured Credit Card | Unsecured Credit Card |

|---|---|---|

| Security Deposit | Required (acts as collateral) | Not required |

| Approval Criteria | Easier to qualify; suitable for no credit or poor credit | Harder to qualify; generally requires good credit history and income |

| Credit Limit | Typically equals the security deposit | Based on creditworthiness and income; can be much higher |

| Risk to Lender | Low (deposit covers potential defaults) | Higher (no collateral) |

| Features/Rewards | Often fewer rewards; some may offer basic perks | More generous rewards, perks, and benefits (e.g., cash back, travel miles) |

| Interest Rates | Can be higher, especially for those with lower credit scores | Generally lower for those with excellent credit |

| Transition Potential | Can often graduate to an unsecured card with responsible use | No “graduation” needed; already an unsecured card |

While unsecured cards often come with more attractive benefits and lower interest rates, they are out of reach for many who are just starting their credit journey. This is precisely where secured cards become invaluable, offering a stepping stone to eventually qualify for those better terms.

Benefits of Using a Secured Credit Card

The advantages of a secured credit card extend beyond simply gaining access to a credit line. They are specifically designed to facilitate credit building and provide financial literacy.

- Accessibility: One of the biggest benefits is that secured cards are significantly easier to get approved for, especially if you have no credit history or a less-than-perfect one. The security deposit minimizes the risk for lenders, making them more willing to extend credit.

- Credit Building: As discussed, consistent and responsible use, including on-time payments and low credit utilization, helps establish a positive payment history that is reported to major credit bureaus. This is the direct path to improving your credit score and building a solid credit file.

- Financial Discipline: Secured cards encourage responsible spending habits. Since your credit limit is tied to your deposit, you are less likely to overspend, making it an excellent tool for learning budget management. Paying off your balance in full each month also helps you avoid interest charges.

- Stepping Stone to Unsecured Credit: With a track record of responsible use, many secured card issuers will offer an upgrade to an unsecured card. This allows you to get your security deposit back and enjoy the benefits of a traditional credit card.

- Fraud Protection: Secured credit cards generally offer the same fraud protection as unsecured cards, such as $0 liability for unauthorized charges, providing peace of mind.

- Online Account Management: Like most modern financial products, secured cards often come with digital tools for managing your account, checking balances, and setting alerts, which can further aid in responsible usage.

A 2021 Consumer Financial Protection Bureau (CFPB) report highlighted that nearly one-third of consumers with subprime credit scores (below 600) in the U.S. had at least one secured credit card account in 2020, underscoring their importance in credit rehabilitation.

How to Choose the Right Secured Credit Card

Not all secured credit cards are created equal. When selecting one, it’s essential to consider various factors to ensure it aligns with your credit-building goals.

- Reports to All Three Major Credit Bureaus: This is arguably the most critical factor. For a secured card to be effective, it must report your payment activity to Equifax, Experian, and TransUnion. Some cards may only report to one or two, which can limit the impact on your overall credit profile. Always confirm this before applying.

- Security Deposit Requirements: Understand the minimum and maximum deposit amounts. Most cards require between $200 and $500, but some can go higher. Choose a card with a deposit you can comfortably afford to tie up, as these funds will be held by the issuer.

- Annual Fees and Other Charges: Look for cards with low or no annual fees. Some secured cards may also have application fees, processing fees, or high interest rates. While interest rates might be higher than unsecured cards, you can avoid interest by paying your balance in full each month.

- Upgrade/Graduation Path: Many secured cards offer a path to “graduate” to an unsecured card after a period of responsible use, typically 6-12 months. This means your deposit is returned, and you receive an unsecured card with potentially better terms. Inquire about the issuer’s policy on this and what criteria you need to meet. Some issuers may automatically review your account, while others might require you to apply separately.

- Credit Limit Flexibility: Some cards may allow you to increase your credit limit by making an additional deposit over time. This can be beneficial as it allows you to lower your credit utilization ratio as your spending habits evolve.

- Additional Features: While less common than with unsecured cards, some secured cards offer basic rewards programs, free FICO score access, or other benefits. These can be a nice bonus if all other primary criteria are met.

Taking the time to compare offers and read the fine print can save you from unexpected fees and ensure the card serves its intended purpose of credit building effectively.

Responsible Usage for Maximum Credit Building

Simply having a secured credit card isn’t enough; responsible usage is the key to unlocking its credit-building potential. Adhering to these habits will significantly accelerate your progress:

- Pay On Time, Every Time: This cannot be stressed enough. Your payment history is the single most important factor in your credit score. Set up payment reminders, automatic payments, or mark your calendar to ensure you never miss a due date.

- Keep Your Credit Utilization Low: As mentioned, aim for a utilization ratio of 30% or less. If your credit limit is $500, try to keep your balance below $150. Even better, pay off your full balance each month to avoid interest and demonstrate excellent financial management.

- Use the Card Regularly: Don’t let the card sit unused. Regular, small purchases that you pay off immediately show consistent activity and responsible management. Consider linking a small, recurring subscription to the card and paying it off promptly.

- Monitor Your Credit Report: Periodically check your credit reports from all three major bureaus (you can get free annual reports from AnnualCreditReport.com). This helps ensure that your card activity is being reported correctly and allows you to dispute any errors. Also, monitor your credit score to track your progress.

- Avoid Opening Too Many Accounts: While building credit, focus on responsibly managing your existing accounts rather than opening multiple new ones in a short period. Multiple hard inquiries can negatively impact your score.

- Understand Rates and Fees: Be aware of the annual percentage rate (APR) and any fees associated with your card. While avoiding interest by paying in full is ideal, understanding the APR is crucial if you occasionally carry a balance.

By diligently practicing these habits, you’ll not only build a robust credit history but also cultivate sound financial behaviors that will serve you well in the long term.

Graduating to an Unsecured Card

The ultimate goal for many secured credit card holders is to “graduate” to an unsecured card. This significant milestone indicates that you’ve successfully demonstrated responsible credit management and are now eligible for more traditional credit products.

The timeline for graduation varies by issuer but typically ranges from 6 to 18 months of responsible use. During this period, the issuer will evaluate your payment history, credit utilization, and overall credit behavior. Some issuers may automatically review your account for an upgrade, while others might require you to request it. When you graduate, your security deposit is typically returned to you, either as a statement credit or a direct refund, and your card becomes an unsecured credit card.

Benefits of graduating to an unsecured card often include:

- Deposit Refund: You get your security deposit back, freeing up those funds.

- Higher Credit Limits: Unsecured cards often come with higher credit limits, increasing your purchasing power and potentially lowering your credit utilization ratio if your spending remains consistent.

- Better Rewards and Perks: Unsecured cards typically offer more attractive rewards programs, such as cash back, travel miles, or other benefits that secured cards might lack.

- Lower Interest Rates: With improved creditworthiness, you may qualify for lower interest rates on your new unsecured card.

If your current secured card issuer doesn’t offer a clear path to graduation, or if you’re not seeing the progress you expect, you can always apply for unsecured cards from other lenders once your credit score has improved. Look for issuers that offer pre-approval checks that don’t involve a hard inquiry on your credit report, which can help you gauge your eligibility without affecting your score.

Conclusion

A secured credit card is a powerful and accessible tool for anyone aiming to build or rebuild their credit history. By understanding how these cards work, choosing the right one for your needs, and committing to responsible usage, you can lay a strong foundation for your financial future. Consistent on-time payments, low credit utilization, and diligent monitoring of your credit report are the cornerstones of successful credit building with a secured card. Embrace this strategic financial product, and you’ll soon be on your way to a robust credit profile, opening doors to better financial opportunities and greater financial freedom.