7 Best Credit Cards for Rewards & Cashback – Full Comparison Guide

Table of Contents

Credit card comparison is an essential exercise for anyone looking to maximize their financial benefits, especially when it comes to rewards and cashback. In today’s diverse financial landscape, credit cards are far more than just tools for making purchases; they are sophisticated instruments that, when used strategically, can offer significant value back to the consumer through various reward programs. From earning a percentage of your spending back as cash to accumulating points for travel or merchandise, the right credit card can turn everyday expenses into meaningful savings and enriching experiences.

However, navigating the vast array of options can be overwhelming. Understanding the nuances between different types of reward structures, annual fees, bonus categories, and redemption values is crucial for selecting a card that genuinely aligns with your spending habits and financial goals. This comprehensive guide aims to demystify credit card rewards and cashback programs, helping you compare the best cards on the market and develop a strategy to get the most out of every swipe.

Understanding Credit Card Rewards and Cashback

At its core, a credit card rewards program is designed to incentivize card usage by offering a kickback on eligible purchases. These incentives typically fall into broad categories: cashback, points, or miles. While all aim to provide value, their mechanisms and optimal use cases differ.

Cashback rewards are perhaps the most straightforward. With a cashback card, you earn a percentage of your spending back as actual cash. This can be redeemed as a statement credit, direct deposit to your bank account, or sometimes as a check or gift card. Cashback cards often come in two main forms: flat-rate cards that offer the same percentage back on all purchases (e.g., 1.5% or 2%) and tiered or rotating category cards that provide higher percentages (e.g., 3-5%) on specific spending categories that may change quarterly or annually.

Points and miles programs, while similar in principle, offer greater flexibility but often require more strategic redemption to maximize their value. Points can typically be redeemed for a variety of rewards, including cash back, statement credits, gift cards, merchandise, or travel. Travel miles are a specific type of point reward, generally associated with airline or hotel loyalty programs, and are best redeemed for flights, hotel stays, or travel upgrades. The value of points or miles can vary significantly depending on how you redeem them; a point might be worth one cent when used for travel but less when redeemed for a statement credit.

Types of Reward Programs: Points, Miles, and Cashback

The variety of reward programs means there’s a card suited for almost every spending style. Understanding these types is the first step in making an informed choice:

- Flat-Rate Cashback Cards: These cards offer a consistent percentage back on all purchases, simplifying the earning process. They are ideal for individuals who prefer not to track bonus categories or have varied spending habits. Cards like the Citi Double Cash Card, for example, offer 2% cash back on every purchase (1% when you buy, 1% when you pay).

- Bonus Category Cashback Cards (Fixed): Some cards offer elevated cashback rates in specific, fixed categories that align with common spending, such as groceries, gas, or dining. For example, the Blue Cash Preferred Card from American Express is known for its high rewards rate at U.S. supermarkets.

- Rotating Category Cashback Cards: These cards feature bonus categories that change, usually every quarter, offering high cashback rates (often up to 5%) in those activated categories, up to a spending cap. Examples include the Chase Freedom Flex and Discover it Cash Back. While offering significant earning potential, they require cardholders to activate new categories quarterly and adapt their spending.

- General Travel Rewards Cards: These cards earn points or miles that can be redeemed flexibly for travel expenses, often through the issuer’s travel portal or by transferring to airline and hotel partners. Cards like the Capital One Venture Rewards Credit Card offer a high flat rewards rate on all purchases that can be used for travel.

- Co-Branded Travel Cards: Issued in partnership with specific airlines or hotel chains, these cards offer accelerated earnings and exclusive perks directly related to that brand, such as free checked bags, priority boarding, or complimentary hotel status.

Key Factors to Consider When Choosing a Rewards or Cashback Card

Selecting the “best” credit card is highly personal, as it depends entirely on your individual financial habits and goals. Several key factors should influence your decision:

- Your Spending Habits: Analyze where you spend most of your money. Are you a frequent traveler, a grocery shopper, a dining enthusiast, or do you have diverse spending? Matching a card’s bonus categories to your highest spending areas is critical for maximizing rewards.

- Annual Fees vs. Rewards Value: Many premium rewards cards come with annual fees, which can range from tens to hundreds of dollars. It’s crucial to assess whether the value of the rewards and perks you’ll receive outweighs this annual cost. Cards with annual fees often offer better rewards rates and more valuable benefits, but zero-annual-fee options can still be highly rewarding.

- Welcome Bonuses/Sign-up Offers: Many cards offer generous sign-up bonuses for new cardholders who meet a certain spending threshold within the first few months. These can provide a significant boost to your rewards balance, but ensure you can meet the spending requirement without overspending.

- Redemption Options and Value: Understand how easily and flexibly you can redeem your rewards. Cashback is straightforward, but points and miles can have varying values depending on the redemption method. Some programs offer higher value when redeemed for travel through their portal or transferred to loyalty partners.

- Other Card Benefits: Beyond rewards, consider other perks like travel insurance, purchase protection, extended warranties, airport lounge access, or foreign transaction fee waivers, especially if they align with your lifestyle.

- Your Credit Score: Top-tier rewards cards typically require good to excellent credit. Knowing your credit score will help you narrow down suitable options.

- Introductory APR Offers: Some rewards cards also come with introductory 0% APR periods on purchases or balance transfers. While rewards are the focus, this can be a valuable feature if you anticipate a large purchase or need to consolidate debt.

Top Cashback Credit Cards: A Detailed Look

For those who prefer direct value back in their pockets, cashback cards are an excellent choice. Here are some of the top contenders frequently highlighted for their generous cashback programs:

Citi Double Cash Card:

- Rewards: Earns an unlimited 2% cash back on every purchase (1% when you buy, 1% when you pay your bill).

- Annual Fee: $0.

- Pros: Simple rewards structure, excellent for long-term use, and no rotating categories to track.

- Cons: No welcome bonus, and foreign transaction fees may apply.

- Best For: Individuals seeking straightforward, consistent cash back on all spending without managing bonus categories.

Chase Freedom Unlimited:

- Rewards: Offers 5% cash back on travel purchased through Chase Travel℠, 3% on dining (including takeout and eligible delivery services) and drugstores, and an unlimited 1.5% cash back on all other purchases.

- Annual Fee: $0.

- Pros: Strong bonus categories for everyday spending, flexible redemption through Chase Ultimate Rewards, and can be paired with other Chase cards for potentially higher value.

- Cons: Requires activation for some offers.

- Best For: Everyday spending, especially for those who dine out, purchase from drugstores, or book travel through Chase, and appreciate flexibility in rewards.

Chase Freedom Flex:

- Rewards: Earns 5% cash back on up to $1,500 in combined purchases in rotating bonus categories each quarter (activation required), 5% on travel purchased through Chase Travel℠, 3% on dining and drugstores, and 1% on all other purchases.

- Annual Fee: $0.

- Pros: High earning potential in bonus categories, diverse bonus categories (e.g., gas, groceries, online shopping, streaming services, home improvement stores, fitness centers), and part of the Chase Ultimate Rewards ecosystem.

- Cons: Requires quarterly activation of bonus categories, and categories might not always align with your spending.

- Best For: Strategic spenders willing to track and activate rotating categories to maximize their cashback.

Blue Cash Preferred Card from American Express:

- Rewards: Offers industry-leading rewards at U.S. supermarkets (often 6% on up to $6,000 in spending per year, then 1%), 6% on select streaming subscriptions, 3% on transit and at U.S. gas stations, and 1% on other purchases.

- Annual Fee: Has an annual fee (waived for the first year).

- Pros: Excellent for grocery spending, strong rewards on streaming and gas, and valuable welcome bonus.

- Cons: Annual fee after the first year, and the grocery bonus is capped.

- Best For: Families and individuals with high grocery and streaming expenses who can justify the annual fee through rewards.

Top Travel Reward Credit Cards: Maximizing Your Journeys

For avid travelers, credit cards that offer miles or points redeemable for travel can unlock significant value, often exceeding the value of cashback. Here are some top picks:

Capital One Venture Rewards Credit Card:

- Rewards: Earns an unlimited 2 miles per $1 spent on every purchase, plus 5 miles per $1 spent on hotels and rental cars booked through Capital One Travel.

- Annual Fee: Has an annual fee.

- Pros: Simple flat-rate earning on all purchases, flexible redemption for any airline or hotel, and a substantial sign-up bonus.

- Cons: Miles might be worth more when transferred to specific partners, requiring some strategy.

- Best For: Travelers who prefer a straightforward rewards structure for everyday spending and want flexibility in booking travel.

Chase Sapphire Preferred Card:

- Rewards: Earns 5x points on travel purchased through Chase Travel℠, 3x points on dining, select streaming services, and online groceries, 2x on all other travel purchases, and 1x on all other purchases. Points are worth 25% more when redeemed for travel through Chase Travel℠.

- Annual Fee: Has an annual fee.

- Pros: Versatile redemption options, strong bonus categories, valuable sign-up bonus, and travel protections like trip cancellation/interruption insurance.

- Cons: Annual fee, and not all grocery store purchases qualify for the bonus.

- Best For: Travelers new to rewards who want a strong foundation card with flexible redemption and good travel perks.

Chase Sapphire Reserve:

- Rewards: Earns 10x points on hotels and rental cars purchased through Chase Travel℠, 10x points on dining purchases through Chase Dining, 5x points on flights purchased through Chase Travel℠, and 3x points on other travel and dining expenses. Points are worth 50% more when redeemed for travel through Chase Travel℠.

- Annual Fee: Higher annual fee.

- Pros: Premium travel benefits, annual travel credit, airport lounge access, strong earning rates on travel and dining, and excellent travel protections.

- Cons: High annual fee that requires significant travel and benefit utilization to offset.

- Best For: Frequent travelers who can fully utilize the extensive travel credits and luxury perks to offset the annual fee.

Best All-Round Reward Credit Cards for Everyday Spending

Some cards excel at offering a good balance of rewards across various spending categories, making them great choices for general everyday use without specializing too heavily in one area. These are often flat-rate cards or those with broad bonus categories.

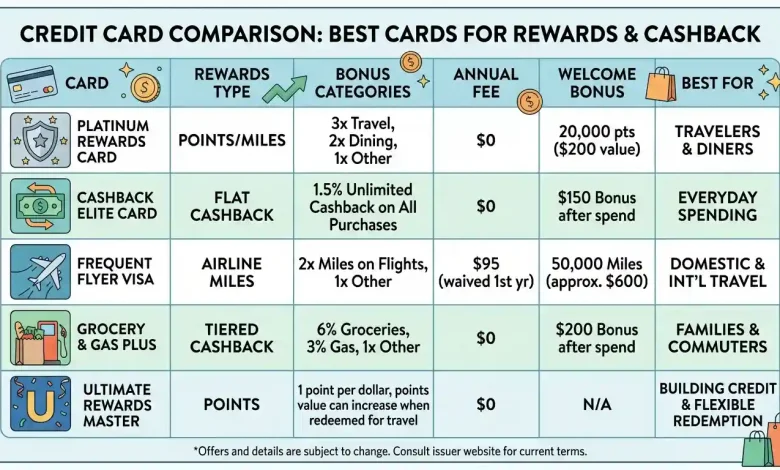

| Credit Card | Key Rewards Rate | Annual Fee | Best For |

|---|---|---|---|

| Citi Double Cash Card | 2% cash back on all purchases | $0 | Simple, unlimited cash back on everything |

| Chase Freedom Unlimited | 1.5% base, 3% dining/drugstores, 5% travel via Chase | $0 | Everyday spending with elevated rewards in common categories |

| Capital One Venture Rewards Credit Card | 2 miles per $1 on all purchases | $95 | Flexible travel rewards for general spending |

| American Express® Gold Card | 4x points on U.S. supermarkets & dining, 3x on flights | $250 | Foodies and frequent flyers who value premium perks |

| Discover it® Cash Back | 5% rotating categories, 1% everything else (with Cashback Match) | $0 | Maximizing rewards in rotating categories, especially for new cardholders |

The American Express® Gold Card, for example, is a strong contender for “foodies” and those who spend heavily on groceries. It typically offers 4x points on purchases at U.S. supermarkets (on up to $25,000 per calendar year, then 1x) and at restaurants worldwide. It also earns 3x points on flights booked directly with airlines or on amextravel.com. While it comes with an annual fee, the statement credits for dining and Uber/Uber Eats can help offset this cost, making it a valuable option for specific spending patterns.

Another excellent all-around card, especially for those who appreciate rotating categories but might want a flat rate for everything else, is the Discover it® Cash Back. This card offers 5% cash back on everyday purchases at different places each quarter, up to a quarterly maximum, when you activate. Plus, it matches all the cashback you’ve earned at the end of your first year, effectively doubling your rewards. This combination of rotating high-earning categories and a solid everyday rate, along with no annual fee, makes it highly attractive.

Optimizing Your Credit Card Strategy for Maximum Benefits

Simply owning a rewards credit card isn’t enough; strategic usage is key to unlocking its full potential. Here are several tips to help you maximize your credit card rewards:

- Match Cards to Purchases: If you have multiple rewards cards, use the one that offers the highest reward rate for a specific purchase. For instance, use your grocery card at the supermarket and your gas card at the pump. This “card-pairing” strategy can significantly boost your overall earnings.

- Activate Bonus Categories: For cards with rotating bonus categories (like Chase Freedom Flex or Discover it Cash Back), always remember to activate the new categories each quarter to earn the elevated rewards. Missing this step means you’ll only earn the base rate.

- Pay Your Balance in Full: This is arguably the most important rule. Any interest charges you incur will quickly negate the value of any rewards you earn. Always pay your statement balance in full each month to avoid interest and late fees. As Britannica Money emphasizes, carrying a balance with double-digit interest charges will “quickly outstrip the value of any rewards you get.”

- Leverage Sign-Up Bonuses: These can be incredibly lucrative. If you’re planning a large purchase, consider timing it with a new card application to meet the spending requirement for a sign-up bonus. However, avoid spending unnecessarily just to hit a bonus threshold.

- Understand Redemption Options: Know the value of your points or miles for different redemption methods. Sometimes, transferring points to travel partners offers a much higher value than redeeming for cash back or merchandise.

- Monitor Promotions: Credit card issuers frequently run special promotions for additional rewards, such as using mobile wallets or shopping at specific retailers. Keep an eye on these offers.

- Consider Annual Fee Justification: Regularly assess whether the benefits and rewards you receive from an annual fee card still outweigh its cost. If your spending habits change or perks are no longer valuable, it might be time to consider a different card or downgrade to a no-fee option.

- Budget and Track Spending: Use your credit card for purchases you would make anyway, and integrate it into your budget. Track your expenses to ensure you’re not overspending in pursuit of rewards. More information on smart credit card usage and avoiding overspending can be found in resources like Wikipedia’s Credit Card article.

Conclusion

The world of credit card rewards and cashback is rich with opportunities for consumers who approach it strategically. By carefully comparing different cards, understanding their reward structures, and aligning them with your personal spending habits, you can transform your everyday purchases into significant savings or memorable experiences. Whether you prioritize straightforward cashback, lucrative travel perks, or a balanced approach, there’s a credit card designed to meet your needs. The key is diligent research, responsible usage, and a commitment to maximizing the value offered by these powerful financial tools. With the right strategy, your wallet can work harder for you, making every transaction a step towards greater financial benefit.