6 Powerful Ways APR Affects Your Credit Card Payments – Smart Finance Guide

Table of Contents

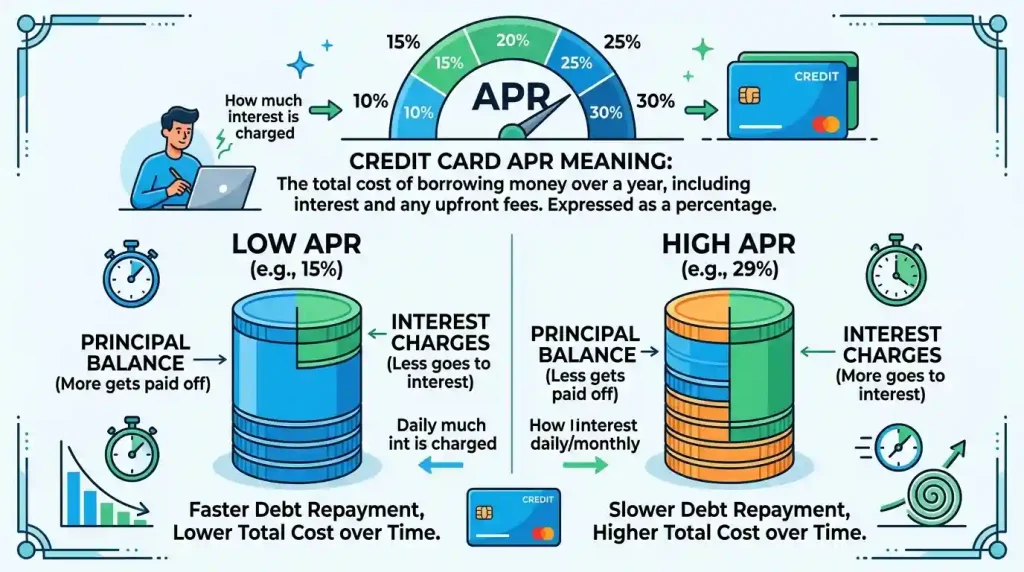

Credit Card APR, or Annual Percentage Rate, is a fundamental concept for anyone using a credit card. It represents the annual cost of borrowing money on your credit card, expressed as a percentage. While often confused with a simple interest rate, APR offers a more comprehensive view of the cost of borrowing by sometimes including certain fees alongside the interest rate itself, although for credit cards, APR and interest rate are typically synonymous. Understanding your credit card’s APR is crucial because it directly dictates how much interest you’ll pay if you carry a balance from month to month, significantly affecting your overall payments and financial health.

Ignoring this critical figure can lead to unexpected and substantial costs over time, turning the convenience of credit into a financial burden. This article will delve into what credit card APR truly means, explore its various types, explain how it’s calculated, and, most importantly, detail how it directly influences your monthly payments, equipping you with the knowledge to make informed financial decisions.

What is Credit Card APR?

APR stands for Annual Percentage Rate and, in the context of credit cards, it is essentially the yearly interest rate charged on any unpaid credit card balances you carry. Unlike other loans where APR might include additional fees like origination fees, for credit cards, the APR typically reflects only the interest rate. This rate is a key determinant of the cost of borrowing and directly impacts the amount you end up paying over time if you don’t clear your balance in full each month.

Every credit card comes with an APR, which card issuers are legally required to disclose to consumers during the application process. The specific APR you receive can vary widely, even for the same card from the same bank, largely depending on your creditworthiness, with higher credit scores generally qualifying for lower APRs. For example, WalletHub data from December 2024 showed that APRs for credit cards for excellent credit averaged 21%, while those for fair credit averaged 26%.

According to data from the Federal Reserve, the average APR on all credit card accounts assessed interest in February 2024 was 22.63%. More recent data indicates the average credit card interest rate was 19.57% as of May 27, 2026, though it hit a record high of 20.79% on August 14, 2024. This rate is often determined by adding a margin to the U.S. prime rate, which itself is tied to the federal funds rate set by the Federal Reserve.

APR vs. Interest Rate: Understanding the Nuance

While the terms “APR” and “interest rate” are often used interchangeably when discussing credit cards, it’s helpful to understand their specific meanings. For credit cards, the APR is generally the same as the interest rate, representing the percentage charged annually on unpaid balances. However, in other forms of lending, such as mortgages or personal loans, the APR can be higher than the stated interest rate because it incorporates additional fees like origination fees, closing costs, and mortgage insurance, providing a more complete picture of the total cost of borrowing. With credit cards, these types of upfront fees are less common, so the APR directly reflects the interest you’ll pay on your debt.

Types of Credit Card APR

Credit cards often come with multiple APRs, each applicable to different types of transactions. Familiarizing yourself with these can help you avoid unexpected costs.

Purchase APR

This is the most common and standard APR, applying to everyday transactions made with your credit card. It’s the rate you’ll pay on your purchases if you carry a balance beyond the grace period.

Cash Advance APR

When you use your credit card to withdraw cash, a separate, typically higher APR applies. Cash advances often incur immediate fees and interest starts accruing right away, without a grace period, making them an expensive form of borrowing.

Balance Transfer APR

This rate applies when you transfer a balance from one credit card to another, often to consolidate debt or take advantage of a lower promotional rate. Many cards offer introductory 0% APRs on balance transfers for a set period to incentivize debt consolidation. However, a balance transfer fee, usually 3% to 5% of the transferred amount, typically applies.

Penalty APR

An elevated rate that can be triggered by late payments or other breaches of your card’s terms and conditions. This rate is typically much higher than your standard purchase APR and can apply to your existing balance and future purchases for a certain amount of time. A typical penalty APR can be around 29.99%.

Introductory/Promotional APR

Many credit cards offer temporary low or 0% APR periods on purchases or balance transfers as an incentive for new cardholders. These promotional rates can be beneficial for reducing interest costs, but it’s crucial to understand that once the introductory period ends (which can range from 12 to 21 months), the standard APR will apply to any remaining balance. Planning your budget and making sure to pay off the balance before the promotional period expires is essential to fully leverage these offers.

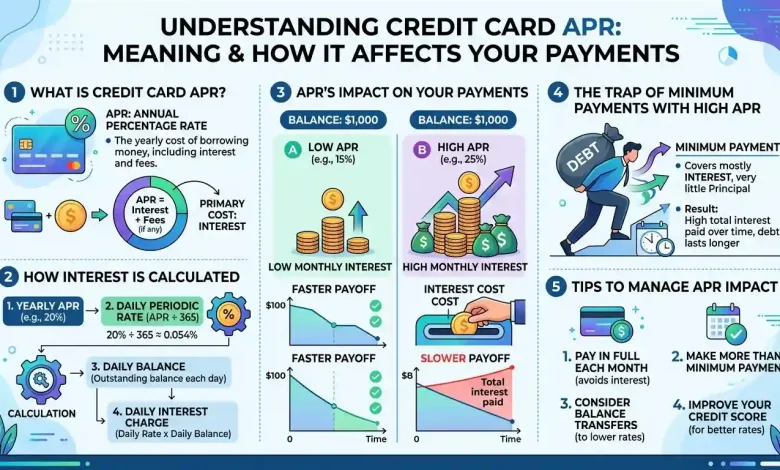

How Credit Card APR is Calculated

Despite its “annual” name, credit card interest is typically calculated on a daily basis and applied monthly. The most common method credit card companies use is the average daily balance method.

Here’s a general breakdown of how it works:

- Determine the Daily Periodic Rate: Your credit card’s APR is divided by 365 (the number of days in a year) to get the daily periodic rate. For example, if your APR is 20%, your daily rate would be approximately 0.0548% (20% / 365).

- Calculate the Average Daily Balance: The issuer takes your balance at the end of each day in your billing cycle, adds them all up, and then divides that sum by the number of days in the billing cycle. This gives you your average daily balance. It’s important to note that if your card uses compounding interest daily, the interest charged from the prior day is added to the balance of the current day for this calculation.

- Calculate Monthly Interest Charges: The average daily balance is then multiplied by the daily periodic rate, and that result is multiplied by the number of days in the billing cycle. This final figure represents the total interest charges you will be assessed for that billing period.

For instance, if you have a $1,000 balance for an entire 30-day billing cycle with a 20% APR:

- Daily Periodic Rate: 0.20 / 365 = 0.0005479

- Average Daily Balance: $1,000

- Monthly Interest: $1,000 x 0.0005479 x 30 = $16.44 (approximately)

This interest amount is then added to your outstanding balance. Understanding this calculation highlights why carrying a balance can lead to your debt growing quickly, especially if only minimum payments are made.

The Impact of APR on Your Payments

The APR is a critical factor in determining how much you pay on your credit card debt and how quickly you can pay it off. A higher APR means a larger portion of your monthly payment will go towards interest rather than reducing your principal balance, making it harder to pay off debt over time. Conversely, a lower APR means more of your payment reduces the principal, allowing you to pay down your debt more efficiently and minimize overall interest costs.

Let’s consider an example: Imagine a credit card with a 20% APR and a balance of $1,000. If you only make the minimum payments, it could take years to pay off, and you would end up paying a significant amount in interest alone. According to one scenario, a $1,000 balance at 20% APR, with minimum payments of $26.67/month, could take 5 years to pay off, incurring $582.23 in interest. However, if you committed to paying it off in 12 months with higher payments of $92.63/month, you would only pay $111.61 in interest. This illustrates the profound impact APR, coupled with payment habits, has on the total cost of borrowing.

The average credit card balance among U.S. consumers was $6,730 as of Q3 2024, with the average APR being 23.37% at that time, which was the highest it had ever been. This high APR environment means that consumers carrying balances are paying more interest, further accelerating debt growth.

| APR Scenario | Balance | Monthly Payment (Example) | Estimated Payoff Time | Total Interest Paid (Approx.) |

|---|---|---|---|---|

| 20% APR | $1,000 | Minimum ($26.67) | 5 Years | $582.23 |

| 20% APR | $1,000 | $92.63 | 12 Months | $111.61 |

| 28% APR | $1,000 | Approx. $45 | ~30 Months | ~ $350 |

| 0% Introductory APR | $1,000 | $83.33 | 12 Months | $0 (during intro period) |

Understanding the Grace Period

A credit card grace period is an interest-free window between the end of your billing cycle and your payment due date. This period allows you to pay off your credit card balance without incurring interest charges on new purchases. As long as you pay your full statement balance by the due date each month, you can continue making purchases on your credit card without paying interest until the next statement due date.

Most credit card issuers offer a grace period of at least 21 days, and often between 21 to 25 days. Some grace periods can even stretch longer, especially if you consistently pay your previous balance in full. However, it’s crucial to understand that grace periods generally only apply to new purchases and usually not to transactions like cash advances or balance transfers, where interest may start accruing immediately. If you fail to pay your full balance by the due date, you may lose your grace period, and interest could be charged from the date of purchase, not just from the due date.

Strategies to Minimize APR Costs

Effectively managing your credit card’s APR can save you a significant amount of money over time, especially with credit card interest rates at high levels. Here are several strategies to keep interest costs in check:

- Pay Your Balance in Full: The most effective way to avoid interest charges is to pay your credit card balance in full each month before the due date. This makes the APR irrelevant for your purchases, saving you from borrowing costs entirely.

- Pay More Than the Minimum: If paying the full balance isn’t feasible, always aim to pay more than the minimum required. Making larger monthly payments reduces your principal balance more quickly, thereby reducing the amount of interest calculated in subsequent billing cycles. Even making multiple payments throughout the billing cycle can help reduce your average daily balance and thus the interest accrued.

- Utilize Balance Transfer Offers: Consider transferring high-interest balances to a new credit card offering a 0% introductory APR on balance transfers. These promotional periods, often lasting 12 to 21 months, can give you a window to pay down debt without accruing new interest. Be mindful of balance transfer fees (typically 3-5%) and ensure you pay off the balance before the introductory period ends.

- Negotiate with Your Issuer: Many card issuers are willing to lower your APR, especially if you have a good payment history, your credit score has improved, or you’ve been a long-term customer. It never hurts to call your credit card company and politely request a lower rate. Even a few percentage points can lead to significant savings over time.

- Improve Your Credit Score: A higher credit score typically translates to lower interest rates on both existing cards (after negotiation) and new credit offers. Responsible credit usage, such as making on-time payments and keeping credit utilization low, can help improve your score. To learn more about how your credit score impacts your financial life, you can refer to our guide on understanding credit scores.

- Avoid Cash Advances: As noted earlier, cash advances typically come with a higher APR and often begin accruing interest immediately. Avoid using your credit card for cash withdrawals unless absolutely necessary.

- Consider Debt Consolidation Loans: For substantial credit card debt spread across multiple cards, a personal loan for debt consolidation can combine balances into a single loan with a lower, fixed interest rate. This can lead to one predictable monthly payment and potentially lower overall interest compared to high-APR credit cards. For further strategies on managing revolving debt, consider reading our article on managing credit card debt effectively.

- Seek Credit Counseling: Non-profit credit counseling agencies can help by negotiating lower interest rates on your behalf through a debt management plan (DMP). These plans can significantly reduce your APR, sometimes even into single digits. More information on consumer finance and debt management can be found on resources like the Consumer Financial Protection Bureau (CFPB) website.

Conclusion

Credit card APR is a cornerstone of understanding the true cost of using your credit card. Far from being just a number, it directly determines how much extra you pay for the convenience of borrowing, profoundly impacting your financial health and the timeline for debt repayment. By comprehending the different types of APR, how interest is calculated, and the invaluable role of the grace period, consumers can navigate the complexities of credit cards with greater confidence. Implementing strategies like paying balances in full, leveraging balance transfers, and actively seeking lower rates can lead to significant savings and a more secure financial future. Empowering yourself with this knowledge is the first step toward mastering your credit card usage and ensuring that you control your finances, rather than your finances controlling you.