6 Best Credit Card Processing Solutions for Businesses & Online Stores

Table of Contents

Credit card processing is an essential function for nearly every modern business, whether operating from a physical storefront or solely online. In today’s digital economy, consumers increasingly rely on credit and debit cards for their purchases, making robust and reliable payment processing capabilities non-negotiable for business growth and customer satisfaction. This comprehensive guide will demystify the intricacies of credit card processing, offering businesses and online stores the knowledge needed to make informed decisions, optimize operations, and ensure secure transactions.

The Foundation: Understanding Credit Card Processing

At its core, credit card processing is the intricate system that facilitates the transfer of funds from a customer’s bank account to a merchant’s bank account when a credit or debit card is used for payment. It’s far more than just swiping a card; it involves a complex network of financial institutions and technologies working in harmony to authorize, clear, and settle transactions securely and efficiently. For businesses, understanding this foundation is critical to selecting the right partners and technologies.

The ability to accept credit cards expands a business’s customer base, increases sales potential, and projects a professional image. Without this capability, businesses risk losing customers who prefer cashless transactions, especially in an era where digital payments are becoming the norm. Efficient credit card processing can also streamline accounting, reduce the risks associated with handling large amounts of cash, and provide valuable data insights into customer spending habits.

The Anatomy of a Credit Card Transaction: A Step-by-Step Breakdown

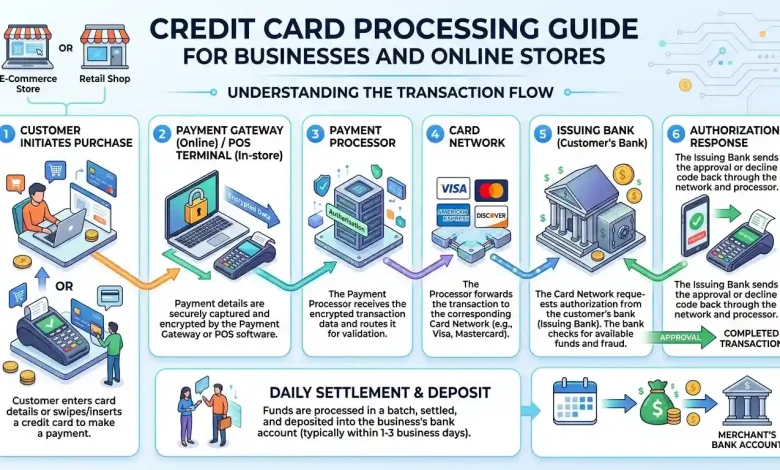

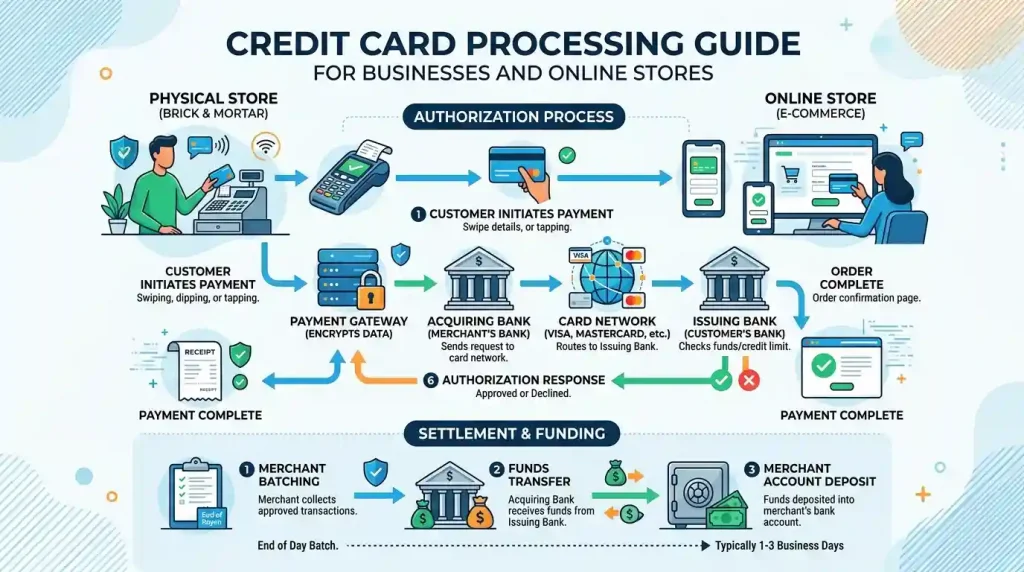

A typical credit card transaction involves several key players and a series of steps that occur in mere seconds. Understanding this flow helps businesses appreciate the value and complexity of the services their payment processor provides.

- Cardholder: The customer initiating the purchase with their credit or debit card.

- Merchant: The business selling goods or services that accepts the credit card payment.

- Point-of-Sale (POS) System/Payment Gateway: The device or software used by the merchant to capture card information. This could be a physical terminal in a store or an online payment gateway for e-commerce.

- Acquiring Bank (Merchant Bank): The financial institution that provides the merchant with a merchant account and processes credit card transactions on their behalf.

- Card Networks (e.g., Visa, Mastercard, American Express, Discover): These global networks act as intermediaries, routing transaction information between the acquiring bank and the issuing bank. They also set interchange rates and processing standards.

- Issuing Bank: The financial institution that issued the credit card to the cardholder.

- Payment Processor: A company that acts as a go-between for the merchant and the acquiring bank, handling the technical aspects of processing credit card transactions. Many acquiring banks also offer processing services directly.

Here’s how a transaction typically unfolds:

- Authorization: The customer presents their card. The POS system or payment gateway captures the card data and sends it to the payment processor. The processor then forwards the request, via the card network, to the issuing bank to verify funds/credit availability and authenticity.

- Authentication: The issuing bank receives the request, checks for fraud, and verifies that the cardholder has sufficient funds or credit. It then sends an approval or denial message back through the card network to the processor, and finally to the merchant’s POS system or payment gateway. This entire step usually takes less than 2-3 seconds.

- Batching: At the end of the business day (or at a set time), the merchant sends all authorized transactions as a “batch” to their acquiring bank via the payment processor. This officially initiates the transfer of funds.

- Clearing and Settlement: The acquiring bank forwards the batch to the card networks, which then request funds from the respective issuing banks. The issuing banks transfer the funds, minus interchange fees, to the card networks. The card networks then transfer the funds, minus their assessment fees, to the acquiring bank. Finally, the acquiring bank deposits the total amount, minus all applicable processing fees, into the merchant’s bank account. This settlement process can take anywhere from 1-3 business days.

Exploring Payment Processing Methods for Every Business Type

The method a business uses to accept credit card payments depends largely on its operational model. Understanding the options available is crucial for selecting the most suitable and cost-effective solutions.

- Traditional Point-of-Sale (POS) Systems: Ideal for brick-and-mortar stores, restaurants, and service-based businesses. These systems can range from simple terminals that swipe or tap cards to integrated systems that manage inventory, sales, and customer data. Many modern POS systems are cloud-based and offer advanced features.

- Online Payment Gateways: Essential for e-commerce businesses. A payment gateway securely connects a website’s shopping cart to the payment processor and acquiring bank. It encrypts sensitive card data and ensures secure transmission, providing a seamless checkout experience for online customers. Popular examples include Stripe, PayPal, and Authorize.net.

- Mobile Payment Processing: Perfect for businesses on the go, such as food trucks, contractors, or market vendors. These solutions often involve a mobile card reader that attaches to a smartphone or tablet, transforming it into a portable POS device. Companies like Square and Zettle (formerly iZettle) are prominent in this space.

- Virtual Terminals: A web-based application that allows businesses to process credit card payments manually using a computer with an internet connection. This is useful for businesses that take orders over the phone or mail, as it eliminates the need for a physical terminal.

- In-App Payments: For businesses that have their own mobile applications, in-app payment solutions allow customers to make purchases directly within the app, often using stored payment information for a quick checkout.

Deciphering Credit Card Processing Costs: Fees and Pricing Models

Credit card processing is not free. Businesses pay various fees for the privilege of accepting card payments. These fees can be complex and vary significantly between processors and card types. Transparency in understanding these costs is vital to managing expenses effectively.

The primary components of credit card processing fees typically include:

- Interchange Fees: These are set by the card networks (Visa, Mastercard, etc.) and paid by the acquiring bank to the issuing bank for each transaction. They are the largest component of processing costs and vary based on card type (rewards, corporate, debit), transaction type (card-present, card-not-present), and industry. Interchange fees are non-negotiable for merchants.

- Assessment Fees: Also set by the card networks, these are paid by the acquiring bank directly to the networks for using their infrastructure and branding. These are typically a small percentage of the transaction volume plus a small per-transaction fee.

- Processor Markup Fees: These are the fees charged by the payment processor or acquiring bank for their services. This is where competition among processors occurs, and where businesses can negotiate. These fees can cover services like fraud detection, customer support, and gateway access.

Payment processors offer various pricing models:

- Interchange-Plus Pricing: Considered the most transparent model, it adds a fixed markup (e.g., +0.20% + $0.10) to the raw interchange and assessment fees. This allows merchants to see exactly what they are paying to the networks and what their processor is charging.

- Tiered Pricing: This model categorizes transactions into different “tiers” (e.g., qualified, mid-qualified, non-qualified), each with its own rate. While seemingly simple, it can be less transparent as processors decide which transactions fall into which tier, often leading to higher rates for mid-qualified and non-qualified transactions.

- Flat-Rate Pricing: A single, fixed percentage (and sometimes a per-transaction fee) is charged for all transactions, regardless of card type or interchange cost. This is popular with smaller businesses and online-only merchants due to its simplicity and predictability, though it may not be the most cost-effective for high-volume businesses. Examples include Square and PayPal, often charging around 2.6% + $0.10 for card-present and 2.9% + $0.30 for online transactions.

- Subscription/Membership Pricing: Merchants pay a flat monthly fee plus a very low, near-interchange-rate percentage per transaction. This can be cost-effective for businesses with high average ticket sizes and significant processing volumes.

Here’s a simplified comparison of common processing fee structures:

| Pricing Model | Description | Pros for Businesses | Cons for Businesses | Best Suited For |

|---|---|---|---|---|

| Interchange-Plus | Processor charges a fixed markup over actual interchange and assessment fees. | Most transparent, potentially lowest cost for high volume. | Requires understanding of interchange rates, complex statements. | Medium to large businesses with predictable volume. |

| Tiered Pricing | Transactions categorized into “qualified,” “mid-qualified,” and “non-qualified” rates. | Simpler than interchange-plus initially. | Less transparent, can lead to unexpected higher costs. | Very small businesses with low volume. |

| Flat-Rate Pricing | A single, fixed percentage (and per-transaction fee) for all transactions. | Predictable and easy to understand. | May be more expensive for high-volume or low-risk transactions. | Small businesses, startups, online stores with lower volume. |

| Subscription/Membership | Monthly fee plus very low percentage per transaction. | Potentially very low overall cost for high volume. | Monthly fee might not be justified for low volume. | Large businesses with high transaction volume and average ticket size. |

Choosing the Right Payment Processor: Key Considerations

Selecting the ideal payment processor is a critical decision that can impact a business’s operational efficiency, profitability, and customer experience. Several factors should guide this choice:

- Cost and Fees: As discussed, thoroughly understand the pricing model and all associated fees (setup, monthly, transaction, PCI compliance, chargeback fees, gateway fees). Request a detailed breakdown and compare it across multiple providers.

- Security Features: Ensure the processor offers robust security measures like encryption, tokenization, and fraud detection tools (e.g., AVS, CVV verification). Adherence to PCI DSS standards is non-negotiable.

- Payment Methods Accepted: Confirm they support all relevant payment types your customers use, including major credit cards, debit cards, and potentially alternative payment methods like digital wallets (Apple Pay, Google Pay).

- Integration Capabilities: For online stores, ensure the payment gateway integrates seamlessly with your e-commerce platform (Shopify, WooCommerce, Magento). For brick-and-mortar, check compatibility with your POS system.

- Customer Support: Evaluate the quality and availability of customer service. Responsive and knowledgeable support is crucial when technical issues or transaction disputes arise.

- Contract Terms: Read the fine print carefully. Look for long-term contracts, early termination fees, and automatic renewals. Flexible, month-to-month agreements are often preferable.

- Reporting and Analytics: Good processors provide detailed reporting tools that help track sales, analyze transaction data, and reconcile accounts.

- Chargeback Management: Understand their policies and tools for handling chargebacks, which can be costly and time-consuming for businesses.

- Scalability: Choose a processor that can grow with your business, handling increased transaction volumes and offering additional features as your needs evolve.

Security and Compliance: Protecting Your Business and Customers

In the realm of credit card processing, security is paramount. Businesses are entrusted with sensitive customer financial data, and protecting this information is not only a legal and ethical obligation but also crucial for maintaining customer trust and avoiding costly data breaches.

- PCI DSS Compliance: The Payment Card Industry Data Security Standard (PCI DSS) is a set of security standards designed to ensure that all companies that process, store, or transmit credit card information maintain a secure environment. Compliance is mandatory for all merchants, regardless of size or transaction volume. Non-compliance can result in hefty fines, loss of processing privileges, and severe reputational damage. The PCI Security Standards Council provides detailed guidelines on achieving and maintaining compliance. Businesses should consult the official PCI SSC website for the latest requirements and best practices: PCI Security Standards Council Official Site.

- Data Encryption: All sensitive credit card data should be encrypted both in transit (when it’s being sent) and at rest (when it’s stored). Encryption scrambles the data, making it unreadable to unauthorized parties.

- Tokenization: This process replaces sensitive credit card data with a unique, non-sensitive identifier called a “token.” If a system storing tokens is breached, the tokens are useless to criminals because they don’t contain any actual card information.

- Fraud Prevention Tools: Implement tools like Address Verification Service (AVS), Card Verification Value (CVV/CVC) checks, and 3D Secure (e.g., Verified by Visa, Mastercard SecureCode) for online transactions. These tools add layers of authentication to verify the cardholder’s identity.

- Regular Security Audits: Periodically review and update security protocols, conduct vulnerability scans, and ensure all software and systems are patched and up-to-date.

- Employee Training: Train employees on best practices for handling credit card information, recognizing phishing attempts, and understanding security procedures.

Advanced Features and Considerations for Optimizing Your Processing

Beyond the basics, various advanced features and considerations can further enhance a business’s credit card processing capabilities and overall financial health.

- Chargeback Management: A chargeback occurs when a cardholder disputes a transaction with their issuing bank, leading to a forced reversal of funds. Chargebacks can be costly due to fees and lost revenue. Businesses should have a clear strategy for preventing them (e.g., clear billing descriptors, prompt customer service, proof of delivery) and for disputing illegitimate chargebacks with compelling evidence.

- Recurring Billing: For subscription services or businesses that offer installment plans, recurring billing features automate the process of charging customers at predefined intervals. This streamlines operations and improves customer retention.

- Omnichannel Payments: For businesses operating both online and offline, an omnichannel payment solution provides a unified platform to manage all transactions, inventory, and customer data seamlessly across different sales channels.

- Alternative Payment Methods: While credit cards are dominant, offering alternative payment methods like PayPal, buy now, pay later (BNPL) services (e.g., Afterpay, Klarna), or even cryptocurrencies can appeal to a broader customer base and enhance convenience.

- Level 2 and Level 3 Data Processing: For B2B transactions, providing Level 2 and Level 3 data (more detailed transaction information beyond the basic Level 1) can qualify merchants for lower interchange rates, especially for corporate or government cards.

- Integration with Accounting Software: Seamless integration with accounting platforms (e.g., QuickBooks, Xero) can automate reconciliation, reduce manual data entry, and improve financial reporting accuracy.

Conclusion: Empowering Your Business with Smart Payment Solutions

Credit card processing is a multifaceted but indispensable aspect of running a successful business in the modern economy. From understanding the fundamental transaction flow and various processing methods to navigating complex fee structures and ensuring robust security, making informed choices is crucial. By diligently evaluating payment processors, prioritizing PCI DSS compliance, and leveraging advanced features, businesses and online stores can optimize their payment operations. This not only streamlines financial management but also builds customer trust, reduces operational risks, and ultimately fuels sustainable growth in a competitive marketplace. Investing time in selecting the right credit card processing guide and solutions today will undoubtedly pay dividends in the future.