7 Best Secured Credit Cards to Build Credit Fast & Safely

Table of Contents

Credit cards to build credit score quickly and safely are indispensable tools for anyone looking to establish or improve their financial standing. A strong credit score is not merely a number; it’s a gateway to significant financial opportunities, including securing loans for homes and cars at favorable interest rates, renting apartments, and even setting up utility services without hefty deposits. Understanding how credit cards impact your credit score and utilizing them strategically can pave the way for a more secure financial future. This comprehensive guide will delve into the mechanisms of credit building with credit cards, offering actionable strategies to help you achieve a robust credit score both quickly and safely.

Understanding Credit Scores and Why They Matter

Before diving into how credit cards can help, it’s crucial to grasp what a credit score is and why it holds such importance. A credit score is a numerical representation of your creditworthiness, based on your credit history. Lenders, landlords, and insurance companies use these scores to assess the risk of doing business with you.

What is a Credit Score?

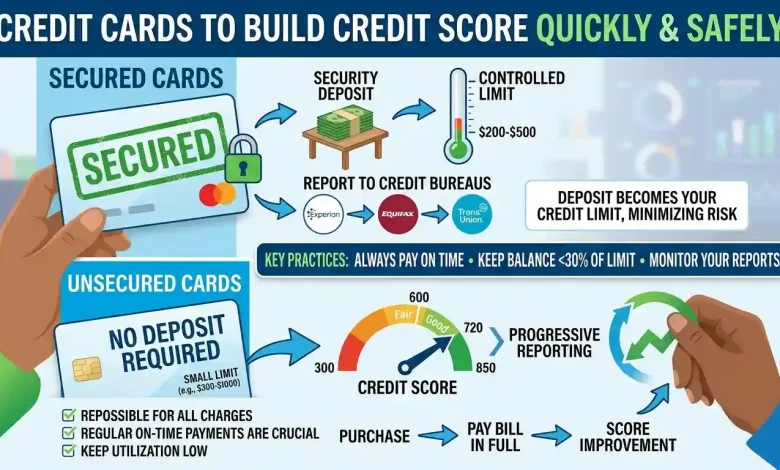

The most commonly used credit scores are FICO scores, which range from 300 to 850. VantageScore is another popular model, also ranging from 300 to 850. Generally, scores are categorized as follows:

- Excellent: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

A good FICO score is typically considered to be 670 to 739. As of January 2024, the average credit score in the United States was 701, which falls into the “Fair” range according to some models.

The Impact of Good and Bad Credit

Your credit score is a key factor in determining your financial opportunities. A higher score signifies lower risk to lenders, making you more likely to qualify for loans and receive favorable terms, such as lower interest rates and flexible repayment periods. For instance, a good credit score can significantly reduce the interest paid on a mortgage or auto loan, saving you substantial money over time. Conversely, a low credit score can lead to denied applications, higher interest rates, and difficulty securing various financial services.

The Foundation: How Credit Cards Influence Your Score

Credit card activity can affect multiple factors that influence credit scores. Credit scoring models like FICO and VantageScore analyze various aspects of your credit history to generate your score. Understanding these factors is paramount to effectively use credit cards for building credit.

Payment History (35% of FICO Score)

Payment history is the single most important factor contributing to your credit scores, accounting for about 35% of your FICO Score and 41% of the latest VantageScore credit model. It demonstrates your ability to manage debt payments over time. Consistently making at least the minimum required payment on time every month generates positive payment history, which can significantly boost your score. Even one payment that’s 30 days or more late can cause a significant drop in your credit score.

Credit Utilization (30% of FICO Score)

Your credit utilization rate is the second most critical factor in your credit score, typically accounting for about 30% of your FICO score and 20% of your VantageScore. This ratio compares how much you owe on your credit cards to your total available credit limit. Lenders generally prefer to see a credit utilization ratio of 30% or lower. Keeping your utilization below this threshold signals responsible financial management and can help improve your score. Many people with excellent credit scores keep their balances even lower, often under 10%.

Length of Credit History (15% of FICO Score)

The length of your credit history, or the average age of your accounts, also plays a role in your credit score. The longer your accounts are open and in good standing, the better it looks to lenders. Closing old credit card accounts, even if unused, can shorten your average credit history and potentially hurt your score.

New Credit (10% of FICO Score)

Each time you apply for new credit, a “hard inquiry” is made on your credit report, which can cause a slight, temporary dip in your score. While necessary when seeking new credit, applying for too many credit cards in a short period can signal financial risk to lenders.

Credit Mix (10% of FICO Score)

Having a healthy mix of different types of credit, such as credit cards, installment loans (like car loans or mortgages), and other lines of credit, can positively impact your score. It demonstrates your ability to manage various forms of debt responsibly.

Choosing the Right Credit Card for Building Credit

For individuals with limited or no credit history, or those looking to rebuild their credit, certain types of credit cards are particularly effective.

Secured Credit Cards

Secured credit cards are often the easiest to qualify for and are an excellent starting point for building credit. To open a secured card, you typically provide a refundable security deposit, which usually becomes your credit limit. This deposit minimizes the lender’s risk, making approval more accessible. Many secured cards report to all three major credit bureaus (Experian, Equifax, and TransUnion), helping you establish a positive payment history. With responsible use, many secured cards offer an upgrade path to an unsecured card and even the return of your security deposit.

Unsecured Cards for Fair/Limited Credit

Some unsecured credit cards are designed for individuals with fair or limited credit. These cards do not require a security deposit, but they may come with lower credit limits and higher interest rates compared to cards for excellent credit. Examples include cards from Capital One, Prosper, and Indigo that consider applicants with fair or bad credit. While potentially harder to obtain than secured cards, they offer a direct path to building credit without tying up cash.

Store Credit Cards

Retail or store credit cards can sometimes be easier to obtain than general-purpose credit cards, especially if you have limited credit. They typically have lower credit limits, which can help prevent overspending while still allowing you to build payment history. However, their usage is often restricted to specific retailers, and interest rates can be high.

Becoming an Authorized User

Becoming an authorized user on a trusted family member’s credit card can be an effective way to begin building credit, particularly for younger individuals. When the primary cardholder uses the card responsibly, their positive payment history can reflect on your credit report. However, it’s crucial that the primary cardholder maintains good credit habits, as their irresponsible actions could also negatively impact your score.

Strategies for Rapid and Safe Credit Building

Once you have a credit card, adopting disciplined habits is key to building your credit score quickly and safely.

| Strategy for Credit Building | Description | Impact on Credit Score Factors |

|---|---|---|

| Pay Bills On Time, Every Time | Ensure all credit card payments are made by or before their due dates. Consider setting up automatic payments. | Payment History: Most significant positive impact (35% of FICO score). Prevents negative marks. |

| Keep Credit Utilization Low | Aim to use less than 30% of your available credit across all cards, ideally under 10% for optimal results. | Credit Utilization: Second most significant impact (30% of FICO score). Low utilization signals responsible management. |

| Don’t Close Old Accounts | Keep older credit card accounts open, even if you don’t use them frequently, to maintain a longer credit history. | Length of Credit History: Contributes to a longer average age of accounts. |

| Monitor Your Credit Report Regularly | Check your credit reports from all three major bureaus for errors or fraudulent activity at least once a year. | Accuracy of Information: Correcting errors can prevent negative impacts and potentially boost your score. |

| Limit New Credit Applications | Only apply for new credit when genuinely needed, spacing out applications to avoid multiple hard inquiries in a short period. | New Credit: Reduces the number of hard inquiries, which can temporarily lower your score. |

| Automate Payments | Set up automatic minimum payments to avoid missing due dates, and consider paying the full balance manually. | Payment History: Ensures consistent on-time payments, the most crucial factor. |

| Use Your Card for Small, Manageable Purchases | Make small purchases you can easily afford to pay off in full each month. | Payment History & Credit Utilization: Builds positive payment history and keeps utilization low. |

Pay Bills On Time, Every Time

This cannot be stressed enough: timely payments are the cornerstone of good credit. Your payment history is the most important factor in your FICO Score. Set up reminders or, even better, automate your payments for at least the minimum amount due to ensure you never miss a deadline. Even if you can only make the minimum payment, staying current is crucial to protect your credit score.

Keep Credit Utilization Low

As mentioned, keeping your credit utilization ratio below 30% is generally recommended. To achieve this, try to pay off your credit card balances in full each month. If that’s not possible, aim to pay significantly more than the minimum payment to reduce your outstanding balance. Knowing when your card issuer reports your balance to the credit bureau can also help; paying your balance down before that date can ensure a lower reported utilization.

Don’t Close Old Accounts

The length of your credit history contributes to your score. Closing old credit card accounts can shorten this history, especially if they are your oldest accounts, and thus negatively impact your score. Unless an old card has a high annual fee that outweighs its benefits, it’s generally best to keep it open, even if you rarely use it.

Monitor Your Credit Report

Regularly reviewing your credit reports from Experian, TransUnion, and Equifax is vital. You can obtain a free credit report from each bureau once a year. Look for any errors, unauthorized accounts, or outdated information. Disputing inaccuracies can lead to corrections that may positively impact your score.

Patience and Consistency

Building a strong credit score is a marathon, not a sprint. While credit cards can help quickly, consistent responsible behavior over time yields the best results. Most people see meaningful improvement within 6-12 months of consistent on-time payments and low utilization. Going from poor credit to good credit typically takes 1-3 years.

Key Features to Look for in a Credit Card

When selecting a credit card for building credit, consider the following features:

- Reports to All Major Credit Bureaus: Ensure the card issuer reports your payment activity to Experian, Equifax, and TransUnion. This is essential for your efforts to reflect across all scoring models.

- Low or No Annual Fee: Especially for starter cards, a low or zero annual fee helps keep costs down while you build credit. Many secured cards, like the Capital One Platinum Secured Credit Card, have no annual fee.

- Credit Limit Increases: Some cards automatically review your account for a credit limit increase after a period of responsible use, such as six months. A higher credit limit, assuming your spending doesn’t increase proportionally, can help lower your credit utilization ratio.

- Upgrade Path: For secured cards, an upgrade path to an unsecured card is a significant benefit, allowing you to transition without a new application.

- Educational Resources: Some card issuers provide tools and resources to help you understand and monitor your credit score, such as free FICO score access.

Common Pitfalls to Avoid

Even with the best intentions, certain mistakes can derail your credit-building efforts. Avoiding these common pitfalls is as important as implementing positive strategies.

Missing Payments

As the most impactful factor on your credit score, missing payments can severely damage your credit. Even a single late payment (30 days or more overdue) can cause a significant drop.

Maxing Out Cards (High Credit Utilization)

Consistently using a high percentage of your available credit signals financial distress to lenders, even if you pay on time. Aim to keep your utilization well below 30% on each card and overall.

Applying for Too Many Cards Too Quickly

Each credit card application results in a hard inquiry on your credit report, which can temporarily lower your score. Spacing out your applications (e.g., waiting at least six months between applications) is a wise approach.

Not Checking Statements Regularly

Regularly reviewing your credit card statements helps you spot errors, fraudulent charges, and track your spending. This vigilance is crucial for maintaining accurate credit reports and preventing potential financial harm.

Carrying a Balance to Build Credit

There’s a common misconception that carrying a small balance on your credit card helps build credit. In reality, carrying a balance only incurs interest charges and does not inherently improve your credit score more than paying it off in full. The key is responsible usage and on-time payments, not carrying debt.

Beyond Credit Cards: Other Ways to Boost Your Score

While credit cards are powerful tools, other financial products and habits can also contribute to a healthy credit score.

- Credit-Builder Loans: Offered by some banks and credit unions, these loans help you build credit and savings simultaneously. The loan amount is held in an account while you make small, regular payments. Once paid off, you receive the funds, and your payment history is reported to credit bureaus.

- Rent and Utility Reporting: Some services allow your rent and utility payments to be reported to credit bureaus, which can be beneficial, especially for those with limited credit history.

- Personal Loans: Once your credit has improved, a small personal loan, managed responsibly, can diversify your credit mix and further strengthen your score.

For more information on general financial health and responsible credit management, you can refer to reputable sources like the Consumer Financial Protection Bureau’s consumer tools.

Conclusion

Credit cards, when used wisely and strategically, are incredibly effective tools for building a strong credit score quickly and safely. By understanding how credit scores are calculated and focusing on timely payments, low credit utilization, and a long credit history, you can significantly enhance your financial standing. Choosing the right card, avoiding common mistakes, and complementing your efforts with other credit-building strategies will pave the way to better financial opportunities and peace of mind. Remember, consistent and responsible credit behavior is the ultimate key to unlocking a healthier financial future.