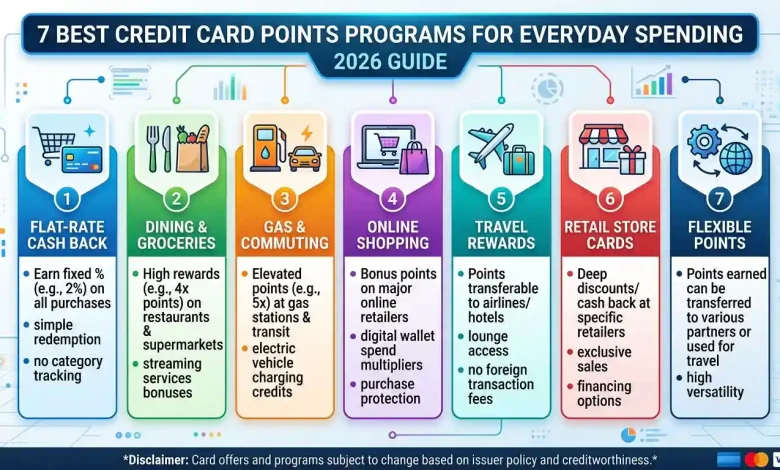

7 Best Credit Card Points Programs for Everyday Spending in 2026

Table of Contents

Credit card points programs have transformed how consumers view their daily expenditures, turning routine transactions into opportunities for significant savings and valuable perks. In an increasingly competitive financial landscape, credit card issuers are continually enhancing their rewards programs to attract and retain cardholders, with a strong emphasis on incentivizing everyday spending. These programs allow individuals to earn points, miles, or cash back on purchases they would make anyway, such as groceries, gas, dining, and online shopping, effectively putting money back in their pockets or funding future experiences.

The allure of credit card rewards isn’t limited to extravagant travel or luxury goods; instead, it’s the consistent accumulation of value from ordinary purchases that makes these programs particularly appealing. By strategically selecting and utilizing credit cards, consumers can turn their regular spending habits into a powerful tool for financial optimization. This comprehensive guide will delve into the mechanics of credit card points programs, explore various types of rewards, outline strategies for maximizing earnings on everyday spending, and provide insights into choosing the best cards for individual financial goals and lifestyles.

Understanding Credit Card Points Programs

Credit card points programs are loyalty perks designed by card issuers to incentivize card usage. At their core, these programs allow cardholders to earn a form of reward—typically points, miles, or cash back—for every dollar spent on eligible purchases. The value and type of reward earned can vary significantly depending on the specific card and its reward structure. Understanding these fundamentals is the first step toward effectively leveraging these programs.

How Points, Miles, and Cash Back Work

- Points: Often considered the most flexible, points can typically be redeemed for a variety of rewards, including cash back, gift cards, merchandise, or travel. The value of a point can fluctuate based on the redemption method; for instance, points might be worth 1 cent each for cash back but 1.5 to 2 cents or more when redeemed for travel through the issuer’s portal or transferred to airline/hotel partners. Programs like Chase Ultimate Rewards, American Express Membership Rewards, and Citi ThankYou Points are popular examples of flexible points systems.

- Miles: Primarily associated with travel rewards, miles are often earned through travel-related purchases or airline-branded credit cards. While typically redeemable for flights, hotel stays, or other travel expenses, their value can also vary. Some general travel cards offer flexible miles that can be used across various airlines and hotels, while co-branded cards tie rewards to a specific airline or hotel loyalty program.

- Cash Back: This is arguably the most straightforward reward, offering a percentage of your spending back as actual cash or statement credit. Cash back cards can offer a flat rate on all purchases (e.g., 1.5% or 2% on everything) or provide higher percentages in specific spending categories. The simplicity and universal appeal of cash back make it a popular choice, especially for those who prefer immediate and flexible value.

Regardless of the type, the core principle remains: responsible credit card use allows consumers to earn rewards on transactions they already plan to make, without incurring interest charges.

How Everyday Spending Translates into Rewards

The magic of credit card rewards lies in their ability to monetize your regular, everyday spending. From your morning coffee to your monthly utility bills, almost every transaction can contribute to your rewards balance. The key is to understand how different spending categories are rewarded and to align your card choices with your personal spending habits.

Categorized vs. Flat-Rate Rewards

Most rewards cards fall into two main structures: categorized rewards or flat-rate rewards.

- Categorized Rewards: Many cards offer accelerated rewards in specific spending categories where consumers typically spend the most. Common bonus categories include groceries, gas stations, dining, travel, and drugstores. For example, a card might offer 5% cash back on groceries, 3% on gas, and 1% on all other purchases. These categories can be fixed year-round or rotate quarterly, requiring cardholders to activate new categories to earn bonus rewards.

- Flat-Rate Rewards: These cards offer a consistent earning rate on all purchases, regardless of the category. A common example is a card that provides unlimited 1.5% or 2% cash back on every transaction. While the earning rate per dollar might be lower than in bonus categories of other cards, the simplicity and broad applicability of flat-rate cards make them excellent for general spending or for consumers who don’t want to track rotating categories.

By reviewing your spending habits, you can identify where you spend the most and choose a card that maximizes rewards in those areas.

Types of Points Programs and Their Benefits

The landscape of credit card points programs is diverse, offering various structures tailored to different consumer preferences and financial goals. Understanding these types is crucial for selecting a program that aligns with your lifestyle and maximizes your earning potential.

General Rewards Programs

These programs, offered by major banks, are known for their flexibility. Points earned can typically be redeemed for a wide array of options, including travel, cash back, gift cards, or merchandise. Examples include Chase Ultimate Rewards, American Express Membership Rewards, and Citi ThankYou Points. A significant benefit of these programs is the ability to transfer points to various airline and hotel loyalty partners, often at a favorable redemption rate, which can unlock substantial value, particularly for travel.

Co-branded Credit Cards

Co-branded cards are partnerships between a credit card issuer and a specific brand, such as an airline, hotel chain, or retailer. These cards typically offer enhanced rewards and exclusive perks when spending with that particular brand. For example, an airline co-branded card might provide free checked bags, priority boarding, or bonus miles on airline purchases. Similarly, a hotel co-branded card could offer elite status, free night certificates, or bonus points on hotel stays. While these cards can be highly rewarding for loyal customers of a specific brand, their redemption options are usually limited to that brand’s loyalty program.

Cash Back Credit Cards

As discussed, cash back cards offer a percentage of your spending back as cash or statement credit. These cards are often recommended for everyday spending due to their simplicity and versatility. Many cash back cards also feature bonus categories that change quarterly or offer higher rates on specific types of purchases, allowing for strategic maximization of rewards.

Maximizing Rewards: Strategies for Everyday Spending

Earning rewards on everyday spending requires more than just owning a credit card; it demands a strategic approach to how and where you use your cards. By implementing smart spending habits, you can significantly boost your rewards accumulation.

Matching the Card to the Purchase

One of the most effective strategies is to use the credit card that offers the highest reward rate for a particular spending category. If you have multiple rewards cards, each excelling in different categories (e.g., one for groceries, another for dining, and a third for gas), make a conscious effort to use the right card for each transaction. For instance, use a card that offers 4x points at US supermarkets for your grocery runs and a different card offering 3x points on dining when eating out. This approach, often referred to as “category maximizing” or “wallet optimization,” ensures you’re always getting the best return.

Automating Recurring Expenses

Monthly bills and subscriptions are predictable expenses that can consistently build rewards. Consider putting recurring charges like streaming services, cell phone bills, internet, and gym memberships on a rewards card, especially one that offers bonus points in those categories. This “set it and forget it” method allows you to earn rewards effortlessly, provided you always pay your balance in full to avoid interest charges.

Utilizing Shopping Portals and Loyalty Programs

Many credit card issuers operate online shopping portals that offer additional bonus points or cash back when you make purchases through their portal with participating retailers. Combining these portals with store loyalty programs allows for “double-dipping” on rewards, earning both credit card points and store loyalty benefits. For example, you might earn extra points by clicking through your card issuer’s portal to an online retailer and then earning that retailer’s loyalty points on your purchase.

Taking Advantage of Welcome Bonuses and Promotions

Credit card issuers frequently offer lucrative welcome bonuses for new cardholders who meet a specified spending requirement within a certain timeframe. These bonuses can be a quick way to accumulate a large sum of points, miles, or cash back. Additionally, many cards offer limited-time bonus promotions for specific merchants or categories. Staying informed about these offers through email alerts or checking your online account can provide opportunities for accelerated earnings.

Top Credit Card Categories for Everyday Rewards

Credit card issuers identify common spending areas to offer bonus rewards, aligning with consumer habits. Knowing these top categories can help you choose cards that best suit your lifestyle.

| Spending Category | Typical Reward Rates / Examples | Popular Card Features |

|---|---|---|

| Groceries | 3% to 6% cash back or 3x-4x points on U.S. supermarket purchases (often capped annually). | Cards like Blue Cash Preferred® Card from American Express (6% on U.S. supermarkets up to $6,000/year, then 1%) or Amex Gold Card (4x points on U.S. supermarkets up to $25,000/year). |

| Dining & Restaurants | 3% to 4% cash back or 3x-4x points on dining, including takeout and eligible delivery services. | Cards such as American Express Gold Card (4x points at restaurants worldwide) or Chase Sapphire Reserve (3x points on dining). |

| Gas Stations & EV Charging | 3% to 5% cash back or 3x points on gas and often EV charging. | Cards like Citi Strata Premier Card (3x ThankYou Points at gas stations and EV charging stations) or Blue Cash Preferred® Card from American Express (3% cash back at U.S. gas stations). |

| Travel | 2x-5x points/miles on general travel, airlines, hotels, or bookings through issuer portals. | Chase Sapphire Preferred, Chase Sapphire Reserve, Capital One Venture Rewards Credit Card, and American Express Platinum Card are popular for travel rewards. |

| Online Shopping | Variable, often through rotating categories (e.g., Amazon.com, Walmart) or specific retailer partnerships. | Cards like Chase Freedom Flex (5% cash back on rotating categories, which can include Amazon.com). |

| Drugstores | Often 3% cash back or 3x points. | Chase Freedom Unlimited and Chase Freedom Flex offer 3% cash back at drugstores. |

| Streaming Services | Often 3% to 6% cash back. | Blue Cash Preferred® Card from American Express (6% on select U.S. streaming services). |

| General/Everything Else | Flat 1.5% to 2% cash back or 1x-2x points on all other purchases. | Cards such as Citi Double Cash® Card (2% cash back) or Chase Freedom Unlimited (1.5% cash back). |

Choosing the Right Card for Your Spending Habits

Selecting the ideal credit card for everyday spending involves a careful assessment of your personal financial situation, spending patterns, and long-term goals. It’s not about finding the “best” card universally, but rather the best card for you.

Analyze Your Spending

The fundamental step is to understand where your money goes. Review your bank statements and expense trackers for the past few months to identify your primary spending categories. Do you spend heavily on groceries, dining out, gas, or online shopping? Are you a frequent traveler? This analysis will reveal which bonus categories would be most beneficial for you. Without this insight, you might choose a card that rewards categories where you spend very little, thus missing out on potential earnings.

Consider Your Financial Goals

What do you hope to achieve with your rewards?

- Cash Back for Savings: If your goal is to reduce monthly expenses or build a savings fund, a strong cash back card is likely the most suitable option.

- Travel for Experiences: For those who prioritize free flights, hotel stays, or travel upgrades, a travel rewards card or a flexible points card with strong transfer partners would be ideal.

- Specific Brand Loyalty: If you frequently use a particular airline or hotel chain, a co-branded card can offer exclusive benefits and accelerated earnings within that brand’s ecosystem.

Evaluate Fees and Interest Rates

Always consider a card’s annual fee. While many premium rewards cards come with annual fees, the value of their rewards and perks can often offset or even exceed this cost, especially for high spenders. However, for lower spenders, a no-annual-fee card might be a smarter choice. More critically, always pay your credit card balance in full and on time. Interest charges can quickly negate any rewards earned, making the card a net loss. Rewards credit cards typically have higher Annual Percentage Rates (APRs), so carrying a balance is particularly costly.

Pitfalls to Avoid and Smart Usage Tips

While credit card points programs offer immense value, they also come with potential pitfalls that can erode your earnings if not managed carefully. Adopting smart usage habits is paramount to maximizing rewards without falling into debt.

Avoid Carrying a Balance

The most critical rule for any rewards card user is to pay your balance in full every month. Credit card interest rates, especially on rewards cards, can be high, quickly wiping out any rewards earned. For example, accruing $600 in interest on a $5,000 balance can swiftly cancel out the value of a substantial rewards bonus. Rewards are only truly beneficial when you avoid interest charges.

Don’t Overspend for Rewards

Never spend more than you can comfortably afford to pay off, even if it’s to reach a welcome bonus spending threshold or to chase bonus categories. The primary purpose of a credit card should be as a convenient payment tool, not an incentive to make unnecessary purchases. Overspending can lead to debt, negating any benefits from the rewards.

Understand Point Valuations and Expiration Dates

The value of points can vary significantly between programs and redemption methods. Research the value of your points for different redemptions (e.g., cash back vs. travel) to ensure you’re getting the most out of them. Additionally, be aware of any expiration dates for your points or miles, or rules regarding account inactivity, and redeem them strategically to avoid losing hard-earned rewards.

Monitor Your Accounts Regularly

Regularly review your credit card statements and online accounts. This helps you track your spending, ensure you’re meeting any bonus category requirements, and promptly identify any fraudulent charges or errors. Setting up transaction alerts can also provide immediate notifications of card activity.

Stay Informed About Program Changes

Credit card reward programs can evolve, with issuers modifying reward structures, bonus categories, and redemption options. Staying informed about these changes, often communicated via email or online account messages, ensures you can adapt your strategy to continue maximizing your earnings. For example, some programs have shifted redemption options from statement credits to direct points redemption for certain categories. The Consumer Financial Protection Bureau (CFPB) has highlighted issues consumers face with unexpected promotional conditions, devaluation, redemption problems, and revocation in credit card rewards programs, underscoring the importance of staying vigilant. A CFPB report on credit card rewards provides further insights into these consumer frustrations.

Conclusion

Credit card points programs offer a powerful avenue to enhance your financial well-being by transforming everyday spending into valuable rewards. By understanding the different types of programs, meticulously analyzing your spending habits, and adopting strategic card usage, you can unlock significant savings and access aspirational perks. Whether you prioritize cash back, travel, or specific brand benefits, there’s a credit card designed to align with your lifestyle. However, the true value of these programs is realized only through responsible financial management: consistently paying balances in full, avoiding overspending, and staying informed about program terms. With a disciplined and informed approach, your credit cards can become more than just payment tools—they can be integral components of a smart financial strategy, continually rewarding your routine expenditures.