6 Smart Balance Transfer Cards to Reduce Interest & Debt Fast

Table of Contents

Balance Transfer credit card options offer a strategic pathway for individuals grappling with high-interest credit card debt. In an economic climate where managing personal finances can be challenging, understanding tools like balance transfers becomes crucial for reducing interest payments and accelerating debt repayment. This comprehensive guide will delve into the intricacies of balance transfer credit cards, exploring how they function, their benefits, potential drawbacks, and how to effectively utilize them to achieve financial relief.

What is a Balance Transfer?

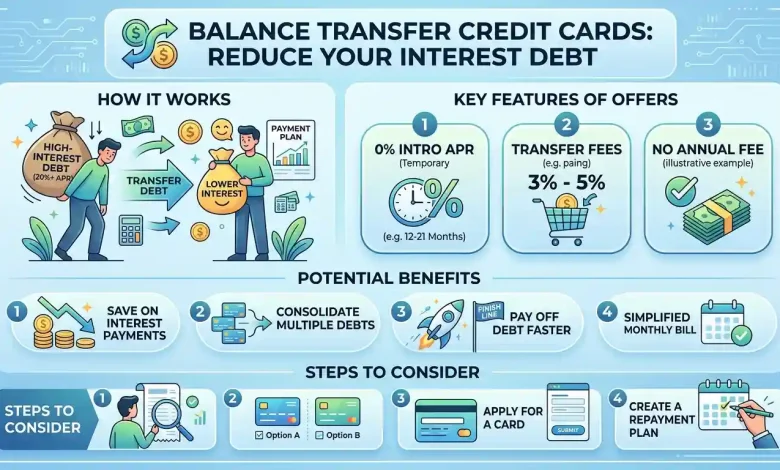

A balance transfer involves moving existing debt from one or more credit card accounts to a new credit card, typically one offering a lower, often 0%, introductory interest rate for a specific period. This mechanism is designed to provide borrowers with a temporary reprieve from high interest charges, allowing more of their monthly payments to go directly towards reducing the principal debt. Essentially, it’s a way to “refinance” high-rate credit card debt, consolidating multiple payments into a single, more manageable one.

The primary goal of a balance transfer is to save money on interest, enabling you to pay off your debt more efficiently. During the promotional period, every dollar you pay contributes to your debt, rather than being eroded by accruing interest. This can significantly accelerate the debt repayment process, helping consumers become debt-free sooner than if they continued paying high interest rates on their original cards.

How Balance Transfers Work

The process of executing a balance transfer generally involves several steps. First, you identify a credit card offering a balance transfer promotion, ideally with a low or 0% introductory Annual Percentage Rate (APR) and a long promotional period. Once you’ve chosen a suitable card, you apply for it. Approval typically depends on your creditworthiness, with a “good” or “excellent” credit score (generally 670 or higher) boosting your chances of qualifying for the best offers.

Upon approval, you initiate the transfer by providing your new issuer with details of the account(s) and amount(s) you wish to move. The new credit card company then pays off your old card(s) and transfers the balance to your new account. The time it takes for a balance transfer to complete can vary, ranging from a few days to several weeks.

It’s crucial to understand that while the introductory APR is in effect, you’ll be paying little to no interest on the transferred balance. However, most balance transfer cards charge a one-time balance transfer fee, usually between 3% and 5% of the amount transferred. This fee is typically added to your new card’s total balance and can eat into your available credit limit.

- Identify high-interest debt you wish to consolidate.

- Research balance transfer credit cards with favorable introductory APRs and terms.

- Apply for the chosen balance transfer card, ensuring you meet the credit score requirements.

- Upon approval, request the transfer, providing necessary account details.

- Monitor the transfer process and confirm the balance has moved successfully.

- Begin making consistent payments on the new card, focusing on paying down the principal before the promotional period ends.

Benefits of Balance Transfers

The primary allure of balance transfer credit cards lies in their ability to significantly reduce the cost of debt. By moving debt to a card with a 0% or low introductory APR, you can avoid accruing high interest charges for a substantial period, often 12 to 21 months. This means that a larger portion of your payments goes directly towards the principal, accelerating your debt repayment.

Another significant benefit is debt consolidation. If you’re managing multiple credit card balances with different due dates and interest rates, a balance transfer can streamline your finances into a single monthly payment. This simplification can make it easier to stay organized, avoid missed payments, and maintain better control over your debt.

Furthermore, successfully paying down a transferred balance during the introductory period can positively impact your credit score. By reducing your overall credit utilization ratio (the amount of credit you’re using compared to your total available credit), you can demonstrate responsible credit management, which is a key factor in credit scoring models.

Potential Downsides and Risks

While balance transfers offer considerable advantages, they are not without their risks and potential downsides. The most prominent is the balance transfer fee, typically 3% to 5% of the amount transferred, which can add to your initial debt. It’s crucial to calculate whether the interest savings during the promotional period outweigh this upfront cost.

Another critical factor is the temporary nature of the introductory APR. Once the promotional period expires, any remaining balance will typically accrue interest at a much higher standard APR, which can be significant. If you don’t pay off the entire transferred balance within the introductory period, you could end up paying more interest in the long run than you saved initially. Some cards might even charge retroactive interest on the unpaid balance if the terms are not carefully reviewed.

There’s also the risk of falling back into debt. Some balance transfer cards offer 0% APR on new purchases as well as transfers, which can be tempting. However, making new purchases on the balance transfer card, or continuing to use your old cards, can quickly negate any benefits and lead to accumulating more debt. Additionally, late payments can often result in the forfeiture of your introductory APR and the imposition of penalty rates.

Applying for a new credit card for a balance transfer also involves a hard inquiry on your credit report, which can cause a temporary dip in your credit score. While this is usually minor and temporary, multiple applications in a short period could have a more significant negative impact.

Choosing the Right Balance Transfer Card

Selecting the optimal balance transfer credit card requires careful consideration of several factors to ensure it aligns with your financial goals and repayment capacity.

| Feature | Description & Considerations |

|---|---|

| Introductory APR Period | Look for the longest 0% or low APR period possible (e.g., 18-21 months). This gives you more time to pay off the debt interest-free. |

| Balance Transfer Fee | Most cards charge a fee (3-5%). Calculate if the interest savings outweigh this fee. Some rare offers may have no fee, but often come with shorter intro periods or higher regular APRs. |

| Regular APR After Intro Period | Understand what the interest rate will be once the promotional period expires. Ideally, you’ll pay off the balance before this kicks in, but it’s important for any remaining debt. |

| Credit Score Requirements | Most attractive offers require good to excellent credit (FICO score of 670+). Cards for fair or bad credit are less likely to offer 0% APR balance transfers. |

| Credit Limit & Transfer Cap | Ensure the card’s credit limit is sufficient to cover the entire balance you wish to transfer, including fees. Some cards have a lower limit for balance transfers than for purchases. |

| Introductory Purchase APR | Some cards offer 0% APR on both balance transfers and new purchases. If you plan to use the card for new spending, ensure the purchase APR period is also favorable, but ideally, avoid new purchases on the card. |

| Annual Fee | Many top balance transfer cards have no annual fee, which helps maximize your savings. |

It’s recommended to use a balance transfer calculator to estimate potential savings and determine if a particular offer is financially beneficial for your specific situation. Remember, the “best” card is one that aligns with your realistic repayment plan.

Strategies for Success with a Balance Transfer

To maximize the benefits of a balance transfer and effectively reduce your interest debt, a well-thought-out strategy is essential.

- Develop a Repayment Plan: Before initiating the transfer, calculate exactly how much you need to pay each month to eliminate the entire transferred balance before the introductory APR period expires. Divide your total transferred debt by the number of months in the promotional period to get your target monthly payment.

- Prioritize Payments: Make consistent, on-time payments, ideally exceeding the minimum required. Every extra dollar paid during the 0% APR period directly reduces your principal.

- Avoid New Debt: Critically, refrain from making new purchases on the balance transfer card. Many cards apply interest immediately to new purchases, even while the transferred balance remains at 0% APR. Furthermore, avoid racking up new debt on your old credit cards. The goal is to get out of debt, not move it around or create more.

- Mark the Expiration Date: Set reminders for when the introductory APR period is scheduled to end. This ensures you’re aware of when higher interest rates will apply to any remaining balance.

- Automate Payments: Set up automatic monthly payments for at least the minimum, or ideally your planned payoff amount, to avoid late fees and the potential loss of your promotional APR.

- Don’t Close Old Accounts Immediately: While tempting, closing old credit card accounts can negatively impact your credit score by reducing your total available credit and increasing your credit utilization ratio. Keep old, unused accounts open to maintain a healthy average age of accounts and utilization.

By adhering to these strategies, you can leverage a balance transfer as a powerful tool for debt management and achieve significant savings on interest, ultimately leading to financial freedom. This proactive approach turns a temporary interest break into a permanent reduction in your debt burden.

Common Mistakes to Avoid

Despite its potential benefits, a balance transfer can exacerbate debt problems if not handled carefully. Being aware of common pitfalls can help you navigate this financial tool successfully.

- Missing Payments: A single late payment can often trigger the loss of your introductory APR, immediately subjecting your balance to a much higher, standard interest rate, or even a penalty APR. This negates the primary benefit of the transfer.

- Making New Purchases: Using the balance transfer card for new spending, especially if the 0% APR only applies to transferred balances, can lead to new, high-interest debt that quickly spirals out of control.

- Not Paying Off the Balance in Time: Failing to eliminate the transferred debt within the promotional period is a common mistake. Once the introductory rate expires, the remaining balance will accrue interest at the card’s standard, often high, variable APR.

- Transferring Too Little Debt: If your new card’s credit limit isn’t high enough to cover all your high-interest debt, you might only transfer a portion, leaving you to manage multiple balances anyway, which reduces the consolidation benefit.

- Ignoring Transfer Fees: While the 0% APR is attractive, the balance transfer fee can be substantial (3-5%). Neglecting this cost in your calculations can make the transfer less beneficial than anticipated.

- Constantly Transferring Balances: Repeatedly opening new credit cards and transferring balances without addressing the root causes of debt can negatively impact your credit score in the long run and make you appear as a higher risk to lenders.

A balance transfer should be a temporary solution with a clear exit strategy, not a perpetual cycle. For a deeper understanding of responsible credit card usage and debt management, you might find valuable resources on platforms like the Consumer Financial Protection Bureau website.

Alternatives to Consider

While balance transfers are effective for many, they aren’t the only solution for managing or paying off high-interest debt. Depending on your financial situation and credit profile, other options might be more suitable.

- Personal Loans: An unsecured personal loan allows you to consolidate multiple debts into a single loan with a fixed interest rate and a predictable monthly payment over a set period (typically 2 to 7 years). This provides a clear payoff date and can be a good option if you need a longer repayment timeline than a balance transfer offers, or if you struggle with resisting new credit card spending. While personal loan rates vary based on creditworthiness, they can often be lower than high credit card APRs.

- Debt Management Plans (DMPs): Offered by non-profit credit counseling agencies, DMPs involve working with counselors to create a payment plan with your creditors. The agency negotiates with creditors for lower interest rates and waives fees, allowing you to make one consolidated monthly payment to the agency, which then distributes funds to your creditors.

- Debt Payoff Strategies (Snowball or Avalanche Method): These self-managed strategies involve focusing intensely on paying off one debt at a time while making minimum payments on others.

- The debt snowball method prioritizes paying off the smallest debt first to build momentum, then rolling that payment into the next smallest debt.

- The debt avalanche method prioritizes paying off the debt with the highest interest rate first, which can save you more money in interest over time.

- Secured Credit Cards: For individuals with bad credit who may not qualify for conventional balance transfer cards, a secured credit card can be a starting point for rebuilding credit. While typically not offering 0% APR balance transfers, some may provide a reduced rate for a limited time, and their responsible use can pave the way for better offers in the future.

- Home Equity Line of Credit (HELOC): If you own a home and have substantial equity, a HELOC can offer lower interest rates because your home secures the debt. However, this option carries higher risk as your home is collateral.

The best alternative depends on your specific financial situation, comfort with risk, credit score, and ability to stick to a repayment plan. It’s advisable to compare the potential savings and risks of each option before committing.

Conclusion

Balance Transfer credit card options can be a powerful financial tool for individuals seeking to reduce high-interest debt and accelerate their path to financial freedom. By offering a period of low or 0% interest, they provide a crucial window to pay down principal without the burden of accumulating interest charges. However, their effectiveness hinges on careful planning, disciplined execution, and a thorough understanding of their terms, including transfer fees and the post-promotional APR.

To truly benefit, consumers must commit to a strict repayment plan, avoid new debt on both the new and old cards, and be vigilant about the introductory period’s expiration. For those who can strategically manage these aspects, a balance transfer offers a valuable opportunity to consolidate debt, simplify payments, and significantly save on interest. For others, exploring alternatives like personal loans or debt management plans might be a more suitable route. Ultimately, the goal is to choose the option that best supports your journey toward a healthier, debt-free financial future.