6 Powerful Credit Card Surcharge Rules for Businesses & Customers

Table of Contents

Credit Card Surcharge Rules are a complex yet critical aspect of modern payment processing, impacting both businesses striving to offset costs and customers seeking transparency in their transactions. In an economy increasingly reliant on electronic payments, understanding when and how these additional fees can be applied is paramount for compliance and consumer trust. While the practice of surcharging is generally permissible in the United States, it is subject to a labyrinth of federal regulations, state-specific laws, and strict card network rules that dictate its implementation. This comprehensive guide aims to demystify credit card surcharges, providing an in-depth look at the regulations governing them and offering clarity for businesses and customers alike.

Understanding Credit Card Surcharges: What They Are and Why They Exist

A credit card surcharge is an additional fee that a business may add to a transaction when a customer chooses to pay with a credit card. Its primary purpose is to help merchants recover the costs associated with processing credit card payments, which can be substantial. These costs typically include interchange fees, assessment fees, and payment processor fees. Surcharges are usually calculated as a percentage of the purchase total, reflecting the merchant’s actual cost of accepting the card.

The ability for U.S. merchants to impose surcharges on credit card transactions largely stems from a 2013 legal settlement between a class of U.S. merchants and major card brands like Visa and Mastercard. Prior to this, surcharging was broadly prohibited by card network rules. However, the settlement allowed merchants in the U.S. and its territories to add surcharges, provided they adhere to specific disclosure requirements and other conditions. This practice has become more common as businesses seek to maintain profit margins in the face of rising processing fees, which can amount to significant expenses, particularly for those handling a high volume of credit card transactions.

Surcharge vs. Convenience Fee: A Crucial Distinction

While often confused, credit card surcharges and convenience fees are distinct charges with different rules and applications. Understanding this difference is vital for businesses to ensure compliance and for customers to identify what they are being charged for.

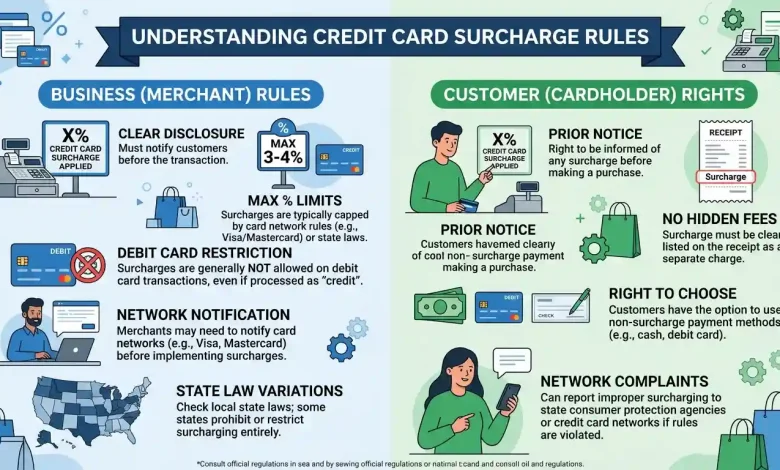

- Surcharge: A surcharge is an additional percentage-based fee applied exclusively to credit card transactions to offset the merchant’s processing costs for those cards. It is directly tied to the cost of accepting the credit card itself. By federal law and card network rules, surcharges cannot be applied to debit or prepaid card transactions, even if a debit card is processed as credit.

- Convenience Fee: A convenience fee, on the other hand, is a charge for the privilege of using a non-standard or alternative payment method or channel, such as paying a bill online or over the phone when the standard method might be in-person or by mail. Unlike surcharges, convenience fees are often a flat dollar amount (though sometimes a small percentage) and are not limited to credit cards; they can apply to debit cards or other electronic payment methods, provided they are tied to the “convenient” channel rather than the card itself. Convenience fees are generally permitted in all U.S. states and territories.

The key differentiator lies in what triggers the fee: the type of card (credit card for surcharges) versus the method or channel of payment (for convenience fees). Businesses must be careful not to conflate the two, as they are governed by different sets of rules and disclosure requirements.

The Legal Landscape: Federal, State, and Card Network Regulations

The legality and implementation of credit card surcharges are shaped by a three-tiered regulatory framework: federal law, state statutes, and the operating rules set by credit card networks. Businesses operating in the United States must navigate all three to ensure compliance.

Federal Framework

At the federal level, the Durbin Amendment, while primarily focused on debit card interchange fees, indirectly influences the overall discussion around payment processing costs. More directly, federal law prohibits card issuers from restricting merchants from offering discounts for cash or other payment methods that do not involve credit cards. The ability for merchants to surcharge credit cards in the U.S. largely stems from a 2013 legal settlement rather than a specific federal law explicitly permitting it. This settlement established the general permissibility of surcharging with certain limitations, such as not exceeding the merchant’s cost of acceptance and requiring clear disclosure.

State-Specific Credit Card Surcharge Laws in the United States

The most complex layer of surcharge rules comes from individual state laws, which vary significantly across the U.S. While surcharging is legal in most states, a handful still prohibit it entirely, and many others impose specific conditions or caps.

- States with Outright Bans: As of 2026, Connecticut, Massachusetts, and Maine, along with Puerto Rico, continue to enforce outright bans on credit card surcharges. Businesses operating in these jurisdictions cannot pass on processing fees through a surcharge under any circumstances and face potential fines or regulatory action if they violate these laws.

- States with Restrictions and Conditions: Many states permit surcharging but impose strict conditions. These often include caps on the surcharge amount, requirements for specific disclosure language, or mandates that the surcharge not exceed the merchant’s actual cost to process the card.

- Colorado: Surcharges are limited to a maximum of 2% or the actual processing fee, whichever is lower.

- New York: A new law effective February 11, 2024, requires businesses to clearly and conspicuously post the total price for using a credit card, inclusive of the surcharge, and the surcharge may not exceed the actual amount charged to the business by the credit card company. The law prohibits simply posting a percentage surcharge without showing the inclusive price. A two-tier pricing system, where cash and credit prices are both displayed, is permitted.

- Illinois: Surcharges are capped at 1% of the transaction amount or the actual processing fee, whichever is lower.

- Nevada, New Jersey, South Dakota, Nebraska, and Georgia: Generally limit surcharges to the merchant’s actual processing cost.

- California and Texas: Historically had statutory bans, but federal courts have found these bans unconstitutional, creating a complex and varying enforcement landscape. Merchants in these states must still ensure transparent pricing, especially in California, where a 2024 amendment (SB 478) requires all mandatory charges, including card-related fees, to be included in the upfront advertised price.

- Florida: Similarly, Florida’s law prohibiting surcharges was held unconstitutional by federal courts, allowing merchants to add surcharges but with limitations on the amount and strict disclosure requirements.

- States with Broad Allowance: In other states, surcharging is more broadly allowed, typically subject to federal disclosure rules and card network requirements, often capped at 3% or 4%.

Businesses operating in multiple states or online must be particularly vigilant, as state laws apply to the merchant’s location of operation and/or the location of the consumer, making compliance a potentially intricate affair. It’s always advisable for businesses to consult legal counsel to ensure full compliance with the specific laws in every jurisdiction where they operate or sell.

Card Network Rules: Beyond Government Regulations

Beyond state laws, major credit card networks such as Visa, Mastercard, Discover, and American Express also impose their own set of rules governing surcharges. These rules are critical for merchants to understand, as violations can lead to significant fines or even the revocation of credit card processing privileges.

- Surcharge Caps:

- Visa: Limits surcharges to the lower of the merchant’s discount rate or 3% of the transaction amount. Visa previously had a 4% cap but reduced it to 3% effective April 15, 2023.

- Mastercard: Allows surcharges up to 4%, but practically, if a merchant accepts both Visa and Mastercard, the effective maximum surcharge is often limited to Visa’s 3% cap. Mastercard also limits surcharges to the merchant’s effective discount rate.

- American Express: Requires that its cards be surcharged at the same rate as other cards.

- Discover: Does not allow surcharges that exceed the cost of processing.

- Notification Requirements: All major card networks, including Visa and Mastercard, require merchants to notify them and their payment processor at least 30 days in advance of implementing surcharges. This notification helps ensure that the networks are aware of the merchant’s intent and can provide guidance on compliance.

- Exclusion of Debit and Prepaid Cards: A universal rule across all major networks and federal law is the prohibition of surcharging debit and prepaid card transactions. Even if a customer opts to run a debit card as a “credit” transaction, a surcharge cannot be applied.

- Disclosure Requirements: Card networks mandate clear and conspicuous disclosure of surcharges to customers. This typically includes:

- Signage at the point of entry (e.g., store entrance).

- Notification at the point of sale or transaction (e.g., at the register, on a payment page for online transactions).

- Itemization of the surcharge on the customer’s receipt.

Here is a table summarizing key credit card surcharge rules across various jurisdictions and card networks:

| Category | Rule/Requirement | Details/Exceptions |

|---|---|---|

| General Legality (U.S.) | Generally permissible in most states. | Subject to state laws and card network rules. |

| States Prohibiting Surcharges | Connecticut, Massachusetts, Maine, and Puerto Rico. | Outright bans. Violations can lead to fines. |

| Maximum Surcharge Cap (Federal/Network) | Typically 3-4% or merchant’s actual cost. | Visa cap: 3%. Mastercard cap: 4% (but often limited to 3% if accepting Visa). Cannot exceed merchant’s actual processing cost. |

| Surcharge Cap (Colorado) | 2% or actual processing cost. | Specific state cap overrides network rules if lower. |

| Surcharge Cap (Illinois) | 1% or actual processing cost. | Specific state cap overrides network rules if lower. |

| Applicability of Surcharge | Only to credit card transactions. | Prohibited on debit and prepaid card transactions. |

| Notification to Card Networks | Required at least 30 days in advance. | Notify Visa, Mastercard, and your payment processor. |

| Customer Disclosure | Clear and conspicuous disclosure required. | At point of entry, point of sale, and on receipts. Must use “surcharge fee.” |

| New York Disclosure | Total price inclusive of surcharge, or two-tier pricing. | Cannot simply post a percentage surcharge. |

| California Disclosure | All mandatory charges in upfront advertised price. | Cannot itemize surcharges as separate fees after the fact. |

Best Practices for Businesses Implementing Surcharges

For businesses considering or currently implementing credit card surcharges, adhering to best practices is crucial for legal compliance, maintaining customer trust, and avoiding potential penalties. Navigating the legalities can be complex, and errors can be costly. For further general information on the history and legal battles surrounding credit card surcharges, a Wikipedia article on credit card surcharges provides a useful overview.

Here are key best practices:

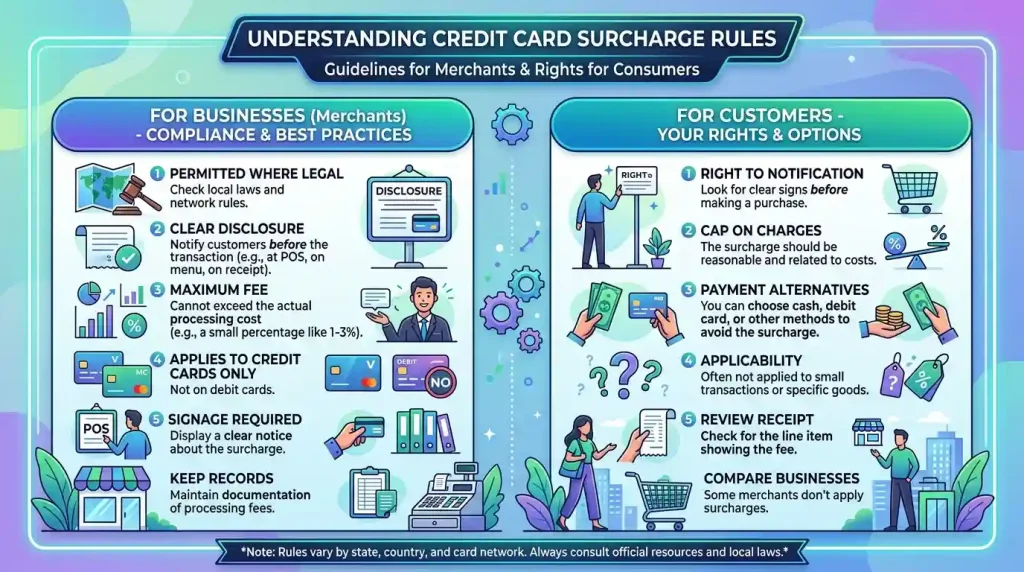

- Verify Legality by Location: Before implementing any surcharge, confirm that it is legal in every state and jurisdiction where your business operates, including for online sales. State laws frequently change and carry significant nuances.

- Notify Card Networks and Processor: Provide at least 30 days’ advance notice to all relevant credit card networks (Visa, Mastercard, Discover, Amex) and your payment processor of your intent to surcharge. Your payment processor can often assist with this process.

- Accurately Calculate Surcharge Amount: The surcharge cannot exceed your actual cost of accepting the credit card, even if card network caps are higher. It must also adhere to any lower state-specific caps. Regularly review your processing statements to determine your effective cost of acceptance.

- Clear and Conspicuous Disclosure: This is perhaps the most critical aspect of compliance.

- Point of Entry: Post clear signage at your physical store’s entrance, informing customers about the surcharge policy. Visa recommends a minimum 32-point Arial font.

- Point of Sale: Display the surcharge clearly at the checkout, whether it’s a physical terminal or an online payment page, before the transaction is completed. For states like New York, this means displaying the total price inclusive of the surcharge or using a two-tier pricing system.

- On Receipts: The surcharge amount must be itemized as a separate line item on every receipt, both in-store and online.

- Use Correct Terminology: Clearly label the fee as a “surcharge fee.” Avoid vague or misleading terms like “non-cash adjustment” or “non-cash fee.”

- Exclude Debit and Prepaid Cards: Never apply surcharges to debit or prepaid card transactions, regardless of how they are processed. Many payment processing systems can automatically differentiate between credit and debit cards to help ensure compliance.

- Train Staff: Ensure all employees who handle transactions are fully aware of your surcharge policy, its legal basis, and how to communicate it clearly and accurately to customers. They should be able to answer questions effectively.

- Offer Alternatives: Provide customers with alternative payment options that do not incur a surcharge, such as cash, checks, or debit cards. This empowers customers to choose how they pay and can mitigate negative perceptions of the surcharge. Offering a cash discount is a common and federally protected alternative to surcharging. Businesses may also consider integrating these rules into their payment processing solutions to streamline compliance.

- Regular Review: Payment processing costs and surcharge regulations can change. Regularly review your surcharge rates and policies to ensure they remain compliant with current state laws and card network rules. For businesses exploring ways to optimize their merchant services, understanding these rules is a foundational step.

The Customer’s Perspective: Navigating Surcharges

For customers, understanding credit card surcharges means being an informed consumer and knowing your rights. While surcharges are generally legal, transparency is key, and you should never be surprised by an unexpected fee at the point of payment.

- Look for Disclosure: Businesses are legally required to disclose surcharges clearly at the entrance, at the point of sale, and on your receipt. If you don’t see such disclosures, you may be able to dispute the charge.

- Know Your State’s Laws: Be aware of whether your state prohibits surcharges entirely or imposes specific limits. For example, if you are in Connecticut, Massachusetts, or Maine, a credit card surcharge should not be applied at all.

- Check the Surcharge Amount: The surcharge should not exceed the merchant’s actual cost of processing or the network/state cap (typically 3-4% federally, but often lower by state). If a surcharge seems excessively high, it might be in violation of rules.

- Distinguish from Convenience Fees: Remember that surcharges only apply to credit cards. If you’re paying with a debit or prepaid card, a “surcharge” is prohibited. A convenience fee might be charged for using an alternative payment channel, but it should be clearly disclosed as such.

- Consider Alternatives: Many businesses that surcharge also offer alternative payment methods (cash, debit) that do not incur the additional fee. If you wish to avoid a surcharge, ask about these options. Some businesses may even offer a cash discount.

- Report Violations: If you believe a merchant is improperly charging a surcharge, especially if it’s undisclosed, too high, or applied to a debit card, you can report it to your state’s Attorney General’s office, a local consumer protection agency, or directly to your credit card company.

Conclusion

Credit card surcharge rules represent a delicate balance between a business’s need to cover operational costs and a consumer’s expectation of transparent pricing. While surcharging has become a widely accepted practice in most parts of the United States, its implementation is far from straightforward. The intricate web of federal guidelines, varying state laws, and strict card network regulations demands meticulous attention to detail from businesses. For merchants, ensuring compliance through proper notification, accurate fee calculation, and robust disclosure practices is not just a legal requirement but a cornerstone of maintaining customer trust and avoiding costly repercussions. For customers, understanding these rules empowers them to make informed payment decisions and to recognize when a fee might be improperly applied. As payment technologies and regulations continue to evolve, staying informed about credit card surcharge rules will remain essential for both businesses and consumers navigating the modern financial landscape.