6 Powerful Credit Card Balance Tips to Avoid Debt & Stay Debt-Free

Table of Contents

Credit card balance management is a critical aspect of personal finance, serving as a cornerstone for avoiding debt and building a stable financial future. In today’s economy, credit cards offer unparalleled convenience and flexibility, enabling everything from emergency purchases to rewards accumulation. However, without proper management, these powerful tools can quickly transform into a significant source of financial strain, leading to accumulating interest, daunting minimum payments, and a cycle of debt that is challenging to escape. This comprehensive guide will delve into effective strategies and practical tips to help individuals maintain control over their credit card balances, prevent the pitfalls of debt, and foster healthier financial habits.

Understanding Credit Card Debt: The Basics

To effectively manage credit card balances, it’s essential to first grasp the fundamental mechanics of how credit card debt accumulates. When you use a credit card, you are essentially borrowing money from the card issuer, which you are then expected to repay. If the full balance is not paid by the due date, interest charges begin to accrue on the outstanding amount. These interest rates, often referred to as Annual Percentage Rates (APRs), can be remarkably high, sometimes exceeding 20% or even 30% for certain cards or individuals with lower credit scores. This means that even small outstanding balances can grow significantly over time if only minimum payments are made.

Minimum payments, while appearing manageable, are often structured to keep you paying interest for an extended period. They typically cover a small percentage of your outstanding balance plus the interest accrued. Relying solely on minimum payments prolongs the repayment period considerably and vastly increases the total cost of your purchases due to compounding interest. For instance, a $2,000 balance with a 20% APR could take over a decade to repay and cost hundreds, if not thousands, in interest if only minimum payments are consistently made. Understanding this mechanism is the first step toward appreciating the urgency of proactive balance management.

Beyond high interest rates, credit card debt can also negatively impact your credit score. A high credit utilization ratio – the amount of credit you’re using compared to your total available credit – is a significant factor in credit scoring models. Experts generally recommend keeping your credit utilization below 30% to maintain a healthy credit score. Exceeding this threshold can signal to lenders that you are a higher credit risk, potentially leading to difficulties in securing loans for homes or cars, or even affecting rental applications and insurance premiums.

The Importance of Proactive Balance Management

Proactive credit card balance management is not just about avoiding debt; it’s about building financial resilience and achieving long-term financial goals. By consistently managing your balances, you gain several key advantages:

- Reduced Interest Payments: The most direct benefit is saving a substantial amount of money that would otherwise go towards interest charges. Paying off balances in full or making more than the minimum payment drastically cuts down the interest accrued, freeing up funds for savings or other investments.

- Improved Credit Score: Lower credit utilization ratios, consistent on-time payments, and a history of responsible credit use are all positive indicators for your credit score. A strong credit score opens doors to better loan rates, higher credit limits, and greater financial flexibility.

- Financial Peace of Mind: The burden of credit card debt can be a significant source of stress and anxiety. Effective management alleviates this pressure, allowing for greater peace of mind and the ability to focus on other aspects of your life.

- Increased Financial Flexibility: When you’re not bogged down by credit card payments, you have more disposable income. This allows you to save for emergencies, invest in your future, or make significant purchases without incurring additional debt.

Developing a systematic approach to credit card management from the outset is far more effective than trying to dig yourself out of debt once it has accumulated. This involves establishing good habits, understanding your spending patterns, and utilizing the right tools and strategies.

Practical Strategies for Lowering Your Credit Card Balance

Once you understand the ‘why’ behind balance management, the next step is implementing practical strategies to bring down existing balances and prevent new debt from forming. These strategies range from disciplined payment approaches to smarter spending habits.

The Avalanche and Snowball Methods

Two popular and effective methods for tackling multiple credit card balances are the debt avalanche and debt snowball methods:

- Debt Avalanche: This method prioritizes paying off the card with the highest interest rate first, while making minimum payments on all other cards. Once the highest-interest card is paid off, you take the amount you were paying on it and apply it to the card with the next highest interest rate. This strategy saves you the most money on interest over time.

- Debt Snowball: With this method, you focus on paying off the card with the smallest balance first, regardless of its interest rate, while making minimum payments on all other cards. Once the smallest balance is cleared, you roll that payment amount into the next smallest balance. This method provides psychological wins, as you see individual cards paid off quickly, which can motivate you to keep going.

The choice between these methods often depends on individual psychology. The avalanche is mathematically superior, while the snowball offers quicker motivational boosts. Both are effective if consistently applied.

Paying More Than the Minimum

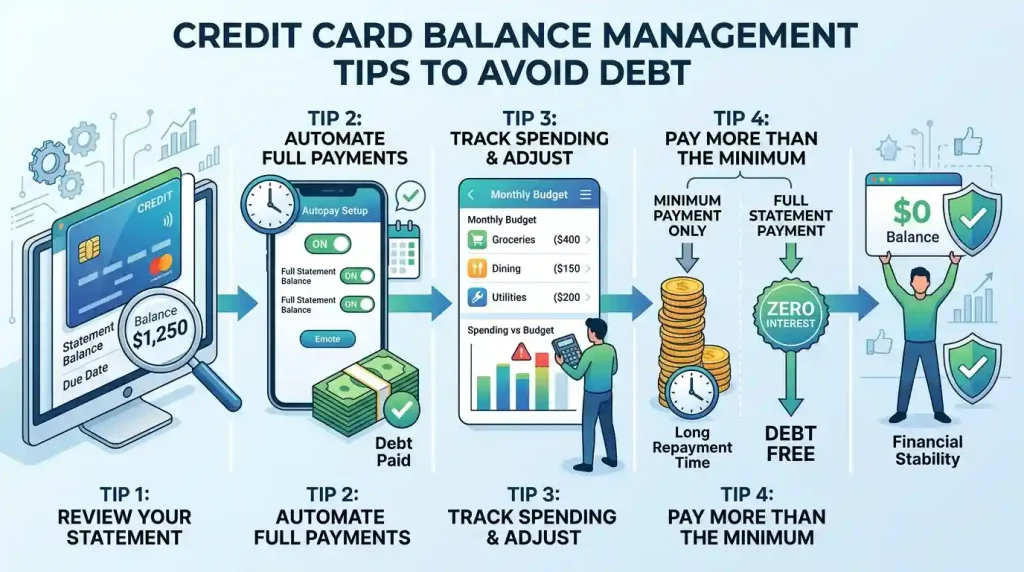

As highlighted earlier, minimum payments are a trap. Whenever possible, pay more than the minimum amount due. Even an extra $20 or $50 each month can significantly reduce the principal balance, thereby cutting down the interest accrued and shortening your repayment timeline. If you can pay off your entire balance each month, you’ll avoid interest charges altogether, effectively making your credit card a free short-term loan.

Budgeting and Tracking Expenses

A robust budget is the bedrock of effective credit card management. By meticulously tracking your income and expenses, you can identify where your money is going and pinpoint areas where you can cut back. This allows you to allocate more funds towards credit card payments. There are numerous budgeting apps and tools available that can automate this process, making it easier to stick to your financial plan. Understanding your spending habits is crucial for preventing overspending and accumulating new debt. For more insights on managing your personal finances, consider resources that delve into effective budgeting strategies.

Consolidating Debt

For those with significant credit card debt spread across multiple cards, debt consolidation can be a viable strategy. This involves combining several debts into a single, new loan, often with a lower interest rate. Common consolidation options include:

- Balance Transfer Credit Cards: These cards offer a promotional 0% APR period (typically 6-18 months) on transferred balances. This can be a powerful tool to pay down debt without accruing interest, provided you can pay off the balance within the promotional period. Be aware of balance transfer fees, which usually range from 3-5% of the transferred amount.

- Personal Loans: A personal loan can be obtained from a bank or credit union at a fixed interest rate, often lower than credit card APRs. This allows you to make one predictable monthly payment until the debt is paid off.

- Home Equity Loans or Lines of Credit (HELOCs): If you own a home, you might be able to borrow against your home equity. These typically have lower interest rates due to being secured by your home, but they also carry the risk of foreclosure if you fail to make payments.

Debt consolidation should be approached cautiously. It simplifies payments and can reduce interest, but it doesn’t eliminate the underlying spending habits that led to debt. If new debt is accumulated after consolidation, you could end up in a worse financial position.

Advanced Techniques for Debt Avoidance and Financial Health

Beyond the fundamental strategies, several advanced techniques can significantly bolster your credit card balance management efforts and contribute to overall financial health.

Negotiating Interest Rates

Many consumers are unaware that they can often negotiate a lower interest rate with their credit card issuer. If you have a good payment history and a decent credit score, a quick phone call to your credit card company might result in a reduced APR. This can save you a substantial amount of money, especially on larger balances. It’s always worth asking, as the worst they can say is no.

Automating Payments

Setting up automatic payments for at least the minimum amount due can prevent late fees and negative marks on your credit report. Ideally, automate a payment for more than the minimum, or even the full balance, if your cash flow allows. This ensures you never miss a payment and keeps your accounts in good standing.

Setting Up Payment Alerts

Utilize the notification features offered by most credit card companies and banking apps. Set up alerts for payment due dates, large transactions, and when your balance approaches your credit limit. These reminders can help you stay on top of your spending and avoid surprises.

Strategic Use of Credit Card Rewards

If you use credit cards responsibly, rewards programs can be a great benefit. However, never spend more than you can afford to pay off each month simply to earn rewards. The interest charged on an unpaid balance will almost always outweigh the value of any rewards earned. Use rewards as a bonus for spending you would have done anyway, not as an incentive to overspend.

Here’s a table summarizing common debt reduction strategies:

| Strategy Name | Primary Benefit | Best Suited For | Potential Drawbacks |

|---|---|---|---|

| Debt Avalanche | Maximizes interest savings | Disciplined individuals seeking maximum financial efficiency | Slower psychological wins |

| Debt Snowball | Provides motivational boosts | Individuals needing quick wins to stay motivated | May pay more interest overall |

| Balance Transfer Card | 0% APR period on transferred debt | Those who can pay off transferred debt within promotional period | Balance transfer fees, risk of new debt after promo ends |

| Personal Loan | Fixed, often lower interest rate; single monthly payment | Consolidating multiple high-interest debts | Requires good credit for best rates, fixed payment commitment |

| Budgeting & Tracking | Identifies spending leaks, controls future spending | Everyone, foundational for financial health | Requires consistent effort and discipline |

The Role of Credit Scores and Responsible Usage

Your credit score is a numerical representation of your creditworthiness, and it’s heavily influenced by how you manage your credit cards. A healthy credit score is vital for numerous financial endeavors, from securing a mortgage to obtaining favorable interest rates on car loans. Understanding the factors that influence your score can help you make better credit card management decisions. The primary components of a credit score include payment history, amounts owed (credit utilization), length of credit history, new credit, and credit mix.

Responsible credit card usage boils down to a few key principles:

- Pay on Time, Every Time: Your payment history is the most significant factor in your credit score. Even one late payment can have a substantial negative impact. Automating payments is an excellent way to ensure punctuality.

- Keep Utilization Low: Aim to use no more than 30% of your available credit on any given card, and ideally, across all your cards combined. Lower utilization ratios indicate less reliance on borrowed money and are viewed favorably by lenders.

- Avoid Unnecessary New Credit: While it might be tempting to open new credit card accounts for promotional offers, each new application results in a hard inquiry on your credit report, which can temporarily ding your score. Only open new accounts when genuinely necessary.

- Monitor Your Credit Report: Regularly review your credit reports from all three major bureaus (Equifax, Experian, TransUnion) to check for errors or fraudulent activity. You are entitled to a free report from each bureau annually.

By adhering to these principles, you not only avoid debt but also actively build and maintain a strong credit profile, which is an invaluable asset in the financial world. Consistent monitoring and understanding of your financial situation can also be enhanced by exploring broader concepts of long-term financial planning.

When to Seek Professional Help

Despite best efforts, some individuals may find themselves overwhelmed by credit card debt. If you’re struggling to make even minimum payments, constantly relying on credit to cover basic expenses, or facing calls from debt collectors, it might be time to seek professional assistance. There are reputable organizations designed to help people navigate difficult financial situations:

- Non-Profit Credit Counseling Agencies: These organizations offer guidance on budgeting, debt management plans (DMPs), and financial education. A DMP can help consolidate payments into one monthly amount with potentially reduced interest rates. Look for agencies accredited by the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA).

- Debt Management Plans (DMPs): Through a credit counseling agency, a DMP consolidates your unsecured debts into one monthly payment, often with lower interest rates negotiated by the agency. This helps you pay off debt faster and more systematically.

- Debt Settlement Companies: These for-profit companies negotiate with creditors to settle debts for a lower amount than what you owe. While it can reduce your debt, it often comes with significant fees, can harm your credit score, and might lead to tax implications on the forgiven debt. This option should be considered a last resort.

- Bankruptcy: For severe cases of overwhelming debt, bankruptcy might be an option. This is a legal process that can eliminate or restructure your debts, but it has severe and long-lasting negative impacts on your credit score and financial future. Consult with a qualified bankruptcy attorney to understand the implications.

It’s crucial to choose professional help wisely, avoiding scams and predatory practices. Always research an agency or company thoroughly before committing. For further information on financial regulations and consumer protection, especially regarding credit and debt, you can refer to official government resources such as the Consumer Financial Protection Bureau (CFPB).

Conclusion

Credit card balance management is an ongoing process that demands discipline, awareness, and strategic planning. By understanding how debt accumulates, adopting proactive management techniques like budgeting and strategic payment methods, and leveraging tools for automation and monitoring, individuals can effectively avoid the pitfalls of credit card debt. Maintaining a healthy credit score through responsible usage is equally important, paving the way for greater financial freedom and opportunity. When debt becomes unmanageable, knowing when and where to seek professional help ensures that you have the support needed to regain control. Ultimately, the goal is not just to use credit cards, but to master their use, turning them into powerful financial assets rather than liabilities, and securing a stable, debt-free future.

By consistently applying these credit card balance management tips, you empower yourself to navigate the complexities of personal finance with confidence, ensuring that credit cards serve as tools for convenience and growth, not sources of stress and endless debt.

This comprehensive approach to managing credit card balances will help individuals not only avoid debt but also build a solid foundation for long-term financial stability and peace of mind.