6 Best No-Deposit Credit Cards for Easy Credit Building in 2026

Table of Contents

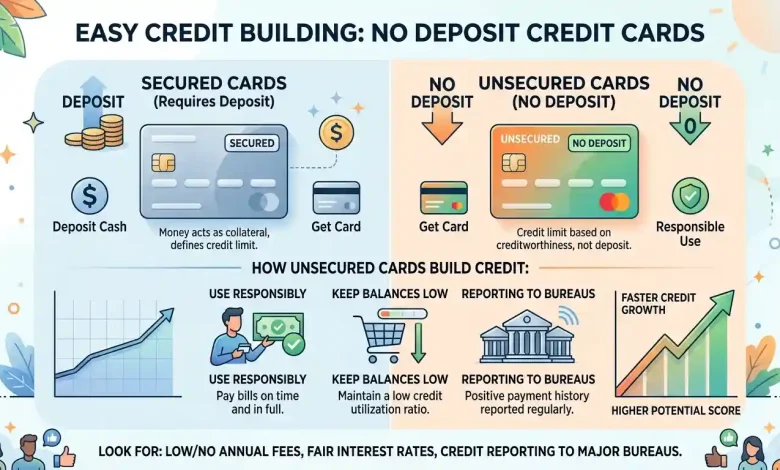

Credit cards with no deposit offer a powerful pathway for individuals looking to establish or rebuild their credit history without the upfront financial commitment typically required by secured credit cards. These unsecured cards are an attractive option, particularly for those with limited credit history or lower credit scores, as they remove the barrier of needing a cash deposit as collateral. Unlike secured cards, which demand a deposit that often mirrors your credit limit, no-deposit credit cards extend a line of credit based on an assessment of your creditworthiness, income, and other financial data.

Understanding No-Deposit Credit Cards

No-deposit credit cards, also known as unsecured credit cards, are the most common type of credit card available. What sets them apart from their secured counterparts is the absence of a security deposit. When you apply for an unsecured card, the issuer evaluates your financial profile, including your credit history, income, and reliability in repaying debts.

For individuals with a limited or poor credit history, securing an unsecured credit card can be challenging. Lenders traditionally view such applicants as higher risk because there is no collateral to recover losses if payments are missed. However, an increasing number of financial institutions and fintech companies are offering no-deposit options specifically designed for credit building, often utilizing alternative underwriting methods that look beyond traditional credit scores, such as bank account activity, income, or employment status.

The core mechanism of an unsecured credit card involves a revolving line of credit. You can borrow up to a pre-set credit limit, and as you repay the borrowed amount, your available credit is restored. Interest accrues on unpaid balances carried over to the next billing cycle, making it crucial to understand the APR (Annual Percentage Rate) associated with the card.

Why Choose a No-Deposit Card for Credit Building?

Opting for a no-deposit credit card offers several distinct advantages for individuals focused on credit building:

- No Upfront Cash Required: This is the most significant benefit. Unlike secured cards that necessitate a cash deposit (often between $200 and $2,500) which is tied up and unavailable for use, no-deposit cards free up your liquid assets. This can be critical if you need your savings for emergencies or other financial needs.

- Opportunity to Build Credit Independently: By managing a no-deposit card responsibly, you demonstrate to lenders that you can handle credit without collateral. This can be a stronger indicator of creditworthiness over time, potentially leading to better credit products in the future.

- Potential for Higher Credit Limits Over Time: While initial credit limits on no-deposit cards for credit building might be lower (e.g., $300-$1,000), consistent on-time payments and responsible usage can lead to credit limit increases. A higher credit limit, in turn, can improve your credit utilization ratio, positively impacting your credit score.

- Access to Rewards and Perks: Some no-deposit credit cards designed for credit building offer cash back or other rewards on purchases, which is a rare feature among secured cards. For example, some cards offer 1% to 3% cash back on specific categories like gas, groceries, and utilities.

- Stepping Stone to Better Financial Products: Successfully managing a no-deposit credit card can significantly improve your credit score, opening doors to a wider range of financial products with more favorable terms, such as lower interest rates on loans and mortgages.

Who Can Benefit from No-Deposit Credit Cards?

No-deposit credit cards are particularly beneficial for several groups:

- Individuals with Limited or No Credit History: Young adults, recent immigrants, or anyone new to the credit system often struggle to get approved for traditional credit cards. No-deposit options that rely on alternative data or have more lenient approval criteria can be a great starting point. Student credit cards also fall into this category, designed for college students to build credit without a deposit.

- Those with Bad Credit: If you have a low FICO score (e.g., below 580), conventional unsecured cards might be out of reach. However, specific no-deposit cards are tailored for those with bad credit, offering a chance to repair their financial standing. These cards provide an opportunity to demonstrate responsible financial behavior, which is crucial for credit repair.

- People Who Cannot Afford a Security Deposit: For many, tying up several hundred dollars in a security deposit for a secured card isn’t feasible. No-deposit cards eliminate this financial hurdle, making credit building accessible to a broader audience.

- Anyone Seeking Financial Flexibility: Keeping cash liquid for emergencies is a smart financial practice. No-deposit cards allow you to build credit without sacrificing your emergency fund or other important savings.

Types of No-Deposit Credit Cards

While the term “no-deposit credit card” broadly refers to unsecured cards, there are variations specifically geared towards different credit profiles:

Unsecured Cards for Fair/Average Credit: If your FICO score is in the “fair” or “average” range (typically 580-669), you have more options for unsecured cards. These cards may offer better terms, including lower APRs and potentially some rewards. Capital One Platinum and Capital One QuicksilverOne are often cited for those with fair credit.

Unsecured Cards for Bad Credit: These cards are designed for individuals with FICO scores below 580. They often come with higher annual fees and interest rates but provide a crucial opportunity to start building positive credit history. Examples include the Aspire® Cash Back Rewards Mastercard, Credit One Bank® Platinum Visa® for Rebuilding Credit, and Perpay Credit Card.

Student Credit Cards: Tailored for college students, these unsecured cards usually have more lenient approval requirements, lower credit limits, and sometimes offer rewards. They are an excellent way for young adults to begin their credit journey.

“Alternative Data” Credit Cards: Some newer fintech companies are disrupting the traditional credit scoring model by considering alternative data like bank transaction history, income, and employment status instead of solely relying on credit scores. Perpay and Arro Card are examples of cards that use such methods for approval, often without a hard credit check at signup.

Here’s a comparison of some popular no-deposit credit cards that cater to credit building:

| Card Name | Best For | Annual Fee | Key Features for Credit Building |

|---|---|---|---|

| Perpay Credit Card | Employed applicants with bad credit and steady paycheck | $5.50 to $9.00 monthly service fee, one-time $9 account opening fee | Up to $1,500 starting credit limit (higher than most), paycheck automated payments, no hard credit check, reports to all 3 bureaus. |

| Aspire® Cash Back Rewards Mastercard | Bad credit seeking rewards | Varies (e.g., $85–$175 yr 1; up to $229 yr 2+) | 3% cash back on gas, groceries, utilities; 1% on others; reports to all 3 bureaus, FICO scores as low as 300 accepted. |

| Petal® 2 Visa® Credit Card | Limited or no credit history, no annual fee | $0 | 1% to 1.5% cash back, reviews bank statements/income instead of credit score, reports to all 3 bureaus. |

| Capital One Platinum Credit Card | Building credit with fair credit | $0 | No annual fee, regular automatic reviews for credit line increases, reports to all 3 bureaus. |

| Tilt® Motion Visa® Credit Card | No credit score required, potential credit limit increases | $0 | No credit score required for approval, reports to all 3 bureaus, reviewed for credit limit increase as early as 4 months. |

| Credit One Bank® Platinum Visa® for Rebuilding Credit | Bad credit, cash back rewards | $75 for the first year, then $99 annually ($8.25/month) | 1% cash back on gas, groceries, and telecom services; prequalification available, automatic credit line reviews. |

| Arro Credit Card | Fair-credit and rebuilding borrowers, no hard credit check | $60/year | Up to $2,500 credit line, no security deposit, no hard credit check at signup, reports to all 3 bureaus. |

Key Features to Look for in No-Deposit Cards

When selecting a no-deposit credit card for credit building, consider these crucial features:

- Credit Bureau Reporting: Ensure the card reports your payment activity to all three major credit bureaus (Experian, Equifax, and TransUnion). This is fundamental for building a comprehensive credit history.

- Annual Fees and Other Charges: While some no-deposit cards offer no annual fee, many cards for individuals with lower credit scores do charge them. Compare these fees carefully, along with potential monthly servicing fees, late fees, and APRs. Look for transparency in fee structures.

- Credit Limit and Potential for Increase: A reasonable starting credit limit (e.g., $300-$1,000) is helpful. More importantly, inquire about the card’s policy for credit limit increases. Many issuers review accounts after 6-12 months of responsible use for potential increases, which can significantly boost your credit score by improving your credit utilization ratio.

- Rewards Programs: While not the primary focus for credit building, some no-deposit cards offer cash back or other rewards. If available, this can be a nice bonus, but prioritize credit-building features over rewards.

- Prequalification Options: Many lenders offer prequalification tools that allow you to check your approval odds without a hard inquiry on your credit report, which can temporarily lower your score. This can help you find suitable options without risk.

- Customer Service and Digital Tools: Good customer service and user-friendly mobile apps or online platforms can make managing your card easier, helping you stay on track with payments and monitor your credit.

How to Responsibly Use No-Deposit Cards to Build Credit

Simply getting a no-deposit credit card isn’t enough; responsible usage is key to effectively building credit. Here are essential tips:

- Make On-Time Payments: Your payment history is the most critical factor in your credit score. Always pay at least the minimum amount due by the due date. Setting up automatic payments can help prevent missed payments.

- Keep Credit Utilization Low: Aim to keep your credit utilization ratio (the amount of credit you’re using compared to your total available credit) below 30%, ideally even lower. For example, if you have a $500 credit limit, try to keep your balance below $150. This demonstrates that you don’t rely heavily on borrowed money.

- Pay Your Balance in Full (If Possible): Paying your statement balance in full each month avoids interest charges and further demonstrates responsible credit management. This also helps you avoid accumulating debt.

- Monitor Your Credit Report: Regularly check your credit reports from all three major bureaus for errors or fraudulent activity. You are entitled to a free copy of your credit report from each bureau annually.

- Avoid Opening Too Many New Accounts: Each credit application can result in a hard inquiry on your credit report, which can slightly lower your score temporarily. Apply for new credit only when necessary.

- Understand the Terms and Conditions: Familiarize yourself with your card’s APR, fees, and grace period to avoid unexpected costs.

For more detailed guidance on improving your credit, reputable sources like the Consumer Financial Protection Bureau (CFPB) offer valuable resources on understanding and managing your credit. The Consumer Financial Protection Bureau’s website provides information on credit reports and scores, which is crucial for anyone looking to build or rebuild their credit effectively.

Common Misconceptions About No-Deposit Credit Cards

Several myths surround no-deposit credit cards, particularly for those with less-than-perfect credit:

- Myth: They are “guaranteed approval.” While some cards are easier to get, no credit card offers truly guaranteed approval. All applications involve an assessment of risk, even if it’s based on alternative data.

- Myth: All no-deposit cards for bad credit are predatory. While some cards may have high fees and interest rates, many legitimate options exist that provide a clear path to credit building without being overly burdensome, especially if used responsibly.

- Myth: Secured cards are always better for building credit. Secured cards are a good option for many, but they are not inherently “better” than unsecured cards for credit building. Both types can be effective when used responsibly. The best choice depends on your financial situation and whether you have cash available for a deposit. In some cases, a secured card with a clear upgrade path to unsecured can be a good strategy.

- Myth: You can’t get rewards with a credit-building card. As seen with cards like Aspire and Petal 2, some no-deposit cards offer cash back rewards, though these are typically less generous than those offered by premium cards for excellent credit.

- Myth: You need a high credit score for any unsecured card. While many unsecured cards require good to excellent credit, there are specific products designed for those with fair, limited, or even bad credit, focusing on helping them build their scores.

Conclusion

Credit cards with no deposit offer an invaluable opportunity for many to embark on their credit-building journey. By understanding the different types available, focusing on key features like credit bureau reporting and fee structures, and committing to responsible usage, individuals can leverage these cards to establish a positive credit history. Whether you’re a student starting out, someone with a limited credit file, or rebuilding after past financial challenges, careful selection and diligent management of a no-deposit credit card can pave the way for a stronger financial future and greater access to favorable credit opportunities. The key is to choose wisely and use your card as a tool for financial growth, always prioritizing on-time payments and low credit utilization.