7 Powerful Home Depot Credit Card Perks – Financing & Rewards Guide

Table of Contents

The Home Depot Credit Card ecosystem offers a diverse range of financing and rewards options designed to cater to both individual homeowners and professional contractors. Navigating these various offerings can unlock significant benefits, from special financing on large purchases to enhanced rewards for loyal business customers. This comprehensive guide delves into the specifics of each card, helping you understand their features, benefits, and crucial considerations for maximizing their value in your home improvement and business endeavors.

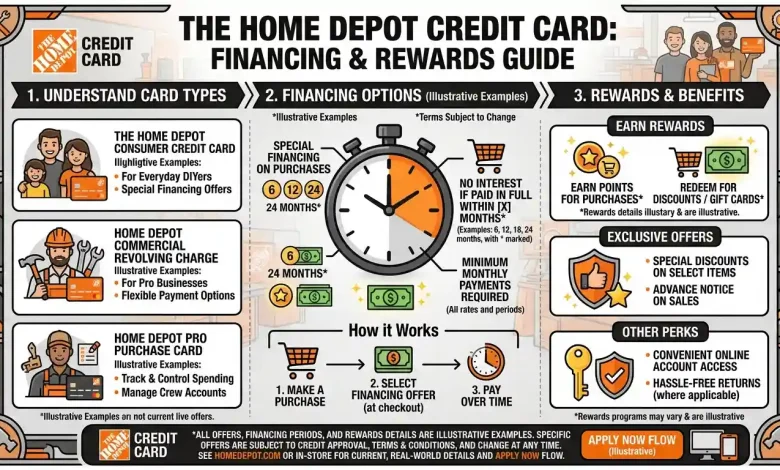

Understanding The Home Depot Consumer Credit Card

The Home Depot Consumer Credit Card is a popular choice for individuals looking to manage their home improvement expenses. Issued by Citibank, this store card can exclusively be used for purchases at Home Depot stores and on Homedepot.com. It stands out primarily for its special financing offers and extended return policy, making it an attractive option for frequent shoppers and those undertaking medium-sized projects. Unlike general-purpose credit cards, it doesn’t offer a traditional rewards program for everyday spending, focusing instead on purchase-specific benefits.

Key Benefits for Homeowners

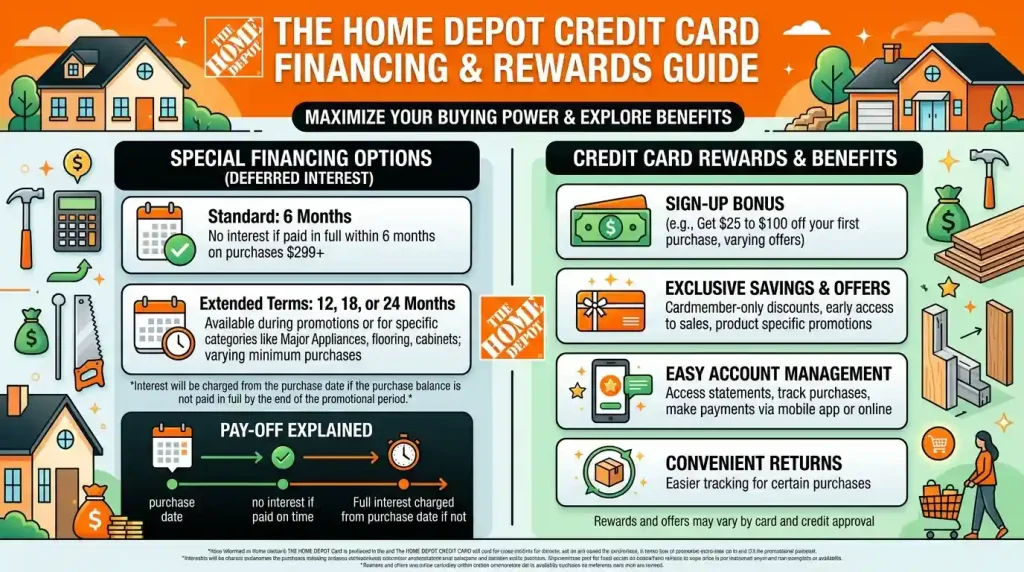

For homeowners, the Home Depot Consumer Credit Card presents several compelling advantages. One of its most significant features is the availability of special financing. Cardholders can typically receive six months of financing with no interest if the purchase of $299 or more is paid in full within that period. This allows for greater financial flexibility when undertaking projects that require a substantial outlay. Additionally, during various special promotions throughout the year, customers might be eligible for even longer financing periods, sometimes extending up to 24 months on specific purchases like appliances, installed windows, or custom closets. New cardholders may also benefit from a first-purchase discount, which can range from $25 off purchases of $25-$299, $50 off for $300-$999, and $100 off purchases of $1,000 or more. Beyond financing, the card offers an extended return policy, granting cardmembers a full year to return most purchases, which is four times longer than the standard 90-day return window. This extended period can be particularly useful for larger projects where items might be bought in advance or excess materials need to be returned. Furthermore, the card boasts a $0 annual fee, making it a low-cost option to maintain. Cardholders also benefit from zero liability protection against unauthorized charges and the flexibility to choose their payment due date.

The Nuance of Deferred Interest

While the special financing offers appear appealing, it is crucial for cardholders to fully understand the concept of “deferred interest.” This is a significant distinction from a true 0% APR offer. With deferred interest, no interest is charged to your account during the promotional period, provided the *entire* purchase balance is paid in full by the promotion’s expiration date. However, if even a single dollar of the promotional balance remains unpaid after the period ends, interest will be retroactively charged to your account from the original purchase date on the full amount. The standard Annual Percentage Rate (APR) for the Home Depot Consumer Credit Card can be quite high, often around 29.99%. This means that failing to clear the balance can result in substantial and unexpected interest charges, turning an attractive financing offer into a costly endeavor. For those interested in understanding the broader implications of such credit terms, a deeper dive into the mechanics of deferred interest versus true 0% APR offers can be found on resources like Wikipedia’s explanation of deferred interest.

The Home Depot Project Loan Card: For Major Renovations

Beyond the standard consumer credit card, Home Depot offers the Project Loan Card, specifically tailored for more extensive home improvement projects. This option is designed for both homeowners and professionals tackling significant renovations, providing a structured financing solution for larger expenditures. It operates more like a personal loan than a traditional revolving credit card, offering fixed monthly payments and higher borrowing limits.

How the Project Loan Works

The Project Loan card can facilitate purchases of Home Depot materials with loan values reaching up to $55,000. Unlike the consumer credit card’s revolving nature, this product typically offers three months of 0% APR on purchases, followed by fixed low monthly payments, and it generally carries no annual fees. The Annual Percentage Rate (APR) for the Project Loan is determined based on the applicant’s creditworthiness, similar to other loan products. This means that individuals with stronger credit profiles are likely to secure more favorable rates. The Project Loan provides flexibility in paying off purchases over an extended period, which can be crucial for managing the budget of a large-scale renovation, such as a kitchen remodel or a roof replacement. Potential applicants for the Project Loan should be prepared for a more rigorous application process, as it is treated more like a traditional loan, often requiring strong income documentation and a focus on maintaining low existing debt balances. This card is a valuable tool for those who have a clear budget for a project and prefer predictable, consistent payments over a set term.

| Credit Product | Primary Use Case | Key Features | Annual Fee | Typical APR |

|---|---|---|---|---|

| The Home Depot Consumer Credit Card | Everyday home improvement purchases ($299+) | 6 months deferred interest (on $299+), extended returns (1 year), new account discount | $0 | 29.99% (variable) |

| The Home Depot Project Loan Card | Large-scale renovations (up to $55,000) | Fixed low monthly payments, 3 months 0% APR (on some purchases), longer repayment terms | $0 | Based on creditworthiness |

| Pro Xtra Credit Card (Commercial Revolving Charge) | Business purchases for professionals | Earns Pro Xtra Perks 4X faster, flexible monthly payments, authorized user cards | $0 | Variable (often high if balance carried) |

| The Home Depot Commercial Account | Business line of credit for professionals | 2% early pay discount (20 days), 60-day payment window, itemized billing, employee cards | $0 | No APR (pay-in-full account) |

Tailored Solutions for Professionals: Commercial Cards and Pro Xtra

The Home Depot recognizes the unique needs of its professional customers, offering specialized credit solutions that go beyond consumer-focused cards. These commercial offerings, primarily the Pro Xtra Credit Card and The Home Depot Commercial Account, are designed to streamline purchasing, manage expenses, and provide additional value for businesses. These cards integrate with the Pro Xtra loyalty program, which is a free program for contractors and other professionals, offering members-only benefits, volume pricing, and exclusive offers.

The Pro Xtra Credit Card

The Pro Xtra Credit Card, also known as the Commercial Revolving Charge Card, is specifically designed for professional customers who frequently make purchases at Home Depot. This card grants automatic entry into the Pro Xtra loyalty program, where cardholders can earn rewards significantly faster. Every dollar spent with the Pro Xtra Credit Card counts as $4 for the purpose of earning Pro Xtra Perks, up to a qualifying purchase cap. These perks can be redeemed for various benefits, including tool rental perks, Pro Xtra Dollars (digital reward cards), and discounts on paint and other products. The Pro Xtra Credit Card offers payment flexibility, allowing businesses to make low monthly payments or pay their balance in full each month. It also provides the ability to issue authorized user cards to trusted employees, enabling them to make company purchases while allowing employers to track spending and set limits. This card, like its consumer counterpart, carries no annual fee. New Pro Xtra Credit Card accounts may also receive an initial discount of up to $100 on qualifying first purchases. The integration with the Pro Xtra program extends beyond just earning; it offers personalized offers, exclusive promotions, and savings tailored to the professional’s purchasing habits. For business owners seeking to efficiently manage their procurement and maximize value from their Home Depot spending, this card is a powerful tool. Learn more about optimizing your business operations with tools like effective business management strategies.

The Home Depot Commercial Account

Distinct from the Pro Xtra Credit Card, The Home Depot Commercial Account is a line of credit tailored for businesses, offering different benefits and payment structures. It is not a credit card account in the traditional sense, as it typically requires the balance to be paid in full each month. This account provides businesses with a 2% early pay discount if the invoice is paid online within 20 days of purchase, or it offers an extended 60-day payment window for greater flexibility. This feature is particularly valuable for businesses managing cash flow or those with longer invoicing cycles. The Commercial Account also allows employers to issue buyer ID cards to authorized users, set spending limits for each, and receive detailed spending information, which helps in tracking purchases and managing budgets effectively. This level of control and detailed reporting is crucial for larger organizations or businesses with multiple employees making purchases. Similar to the other Home Depot credit offerings, the Commercial Account does not charge an annual fee. The ability to itemize all invoices and receive detailed billing statements further enhances financial control and efficiency for professional customers. For businesses that prioritize clear accounting and flexible payment terms over revolving credit, the Commercial Account can be an invaluable asset. Consider how this could fit into your broader financial planning, perhaps alongside information on corporate finance basics.

Navigating Special Financing Offers and Promotions

A primary draw of The Home Depot credit cards, particularly the Consumer Credit Card, lies in its special financing offers. These promotions are designed to help customers manage the cost of significant purchases by deferring interest for a specified period. The standard offer for the Consumer Credit Card is often six months of no interest on purchases of $299 or more, provided the full balance is paid off within that timeframe. Beyond this everyday offer, Home Depot frequently rolls out limited-time promotions, extending financing periods up to 12, 18, or even 24 months for qualifying purchases in specific categories such as appliances, installed services like heating and air conditioning, or custom closets. These longer promotional windows can be particularly advantageous for extensive home renovation projects, allowing more time to complete payments without accruing interest.

Maximizing Promotional Periods

To truly benefit from these special financing offers and avoid the pitfalls of deferred interest, meticulous financial planning is essential. The most critical step is to ensure that the *entire* promotional balance is paid in full before the financing period expires. It is advisable to divide the total purchase amount by the number of months in the promotional period and make consistent, on-time payments that meet or exceed this calculated monthly amount. This strategy helps to systematically reduce the balance and prevent any retroactive interest charges. Home Depot and its issuer, Citibank, often apply payments in excess of the minimum due to higher APR balances first, but during the last 2-3 billing cycles of a deferred interest promotion, excess payments may be directed towards the expiring promotional balance, which can be a helpful feature if managed correctly. Cardholders should actively monitor their account statements and set reminders for the promotional end dates. Taking advantage of promotional offers requires discipline, but when managed effectively, they can significantly reduce the immediate financial burden of large home improvement expenses and provide a valuable budgeting tool.

Application Process and Eligibility

Applying for a Home Depot credit card is a relatively straightforward process, with options available both online and in-store. Whether you’re interested in the Consumer Credit Card, Project Loan, or a Commercial offering, understanding the eligibility criteria is key to a successful application. Citibank issues most of The Home Depot’s credit products, and approval is based on a review of your creditworthiness.

Credit Score and Requirements

For the Home Depot Consumer Credit Card, applicants generally need a fair credit score or better, typically in the range of 640 or higher, though approvals can sometimes occur with scores as low as 620 if other factors are strong. The Project Loan, given its larger borrowing amounts, usually looks for a slightly stronger credit profile, around 640 and above. Beyond a credit score, applicants must be at least 18 years old, possess a valid Social Security Number or International Tax Identification Number, provide proof of identity, have verifiable income, and a manageable debt-to-income ratio. You’ll typically be required to provide personal information such as your name, address, phone number, and financial details including your annual income, sources of income, and employment status.

One beneficial feature is the ability to pre-qualify for The Home Depot Consumer Credit Card online without impacting your credit score. This pre-qualification process allows you to gauge your likelihood of approval and see potential terms before committing to a full application, which triggers a hard inquiry on your credit report and may temporarily lower your score by a few points. While pre-qualification doesn’t guarantee final approval, it provides a good indication of your eligibility. Once approved, customers can often use their new credit account immediately for purchases.

Managing Your Home Depot Credit Card Account

Efficiently managing your Home Depot credit card account is vital to maximize its benefits and avoid potential fees or interest charges. All Home Depot credit products issued by Citibank offer robust online account management tools, allowing cardholders to view statements, track purchases, make payments, and manage various account settings from anywhere.

Customers can typically log into their Citi account online to access detailed information about their balance, transaction history, and promotional offer statuses. For the Commercial Account, businesses can also manage authorized buyers, set spending limits, and receive itemized billing statements through the online portal. The ability to choose your payment due date with the Consumer Credit Card provides additional flexibility in aligning payments with your personal financial calendar.

Should you encounter any issues or have questions, Home Depot and Citibank provide comprehensive customer service. Dedicated phone lines are available for Consumer Credit Card accounts (1-800-677-0232), Project Loan (Member Portal), and Pro Xtra Credit Card accounts (1-800-685-6691). In case of a lost or stolen card, it’s crucial to report it immediately, either by logging into your Citi account online or calling the relevant customer service number, to ensure zero liability protection against unauthorized charges. Regular review of account statements and prompt attention to due dates are critical practices for responsible credit card management, particularly with deferred interest promotions.

Potential Drawbacks and Alternatives

While The Home Depot credit cards offer compelling benefits, it’s important to consider potential drawbacks. The primary concern for the Consumer Credit Card is its high standard APR, which can be as high as 29.99%. If a balance is carried beyond the promotional period or a payment is missed, the retroactive deferred interest can quickly accumulate, negating any savings from the special financing. Additionally, being a store-specific card, its utility is limited to Home Depot, unlike general-purpose credit cards that can be used anywhere. The Consumer Credit Card also typically lacks an ongoing rewards program for all purchases, focusing instead on financing benefits.

For individuals not frequenting Home Depot, or those who struggle with paying off balances in full, a general-purpose credit card with a true 0% introductory APR (not deferred interest) might be a safer alternative for large purchases. Other options for financing large home improvement projects include home equity lines of credit (HELOCs) or personal loans, which can sometimes offer lower, fixed interest rates, though these often involve collateral or more extensive application processes. For businesses, while The Home Depot offers strong commercial options, exploring other business credit cards or lines of credit might provide broader purchasing power and diversified rewards programs.

Conclusion

The Home Depot credit card offerings provide a robust suite of financial tools for both consumers and professionals engaged in home improvement. From the Consumer Credit Card’s special financing and extended returns to the Project Loan’s high-value financing for major renovations, and the Pro Xtra Credit Card’s accelerated rewards for businesses, each option is tailored to specific needs. Understanding the nuances of deferred interest, leveraging promotional periods wisely, and actively managing your account are paramount to unlocking the full potential of these cards. By aligning the right Home Depot credit product with your purchasing habits and financial discipline, you can effectively extend your purchasing power, manage project costs, and even earn valuable perks, making your home improvement journey more efficient and rewarding.