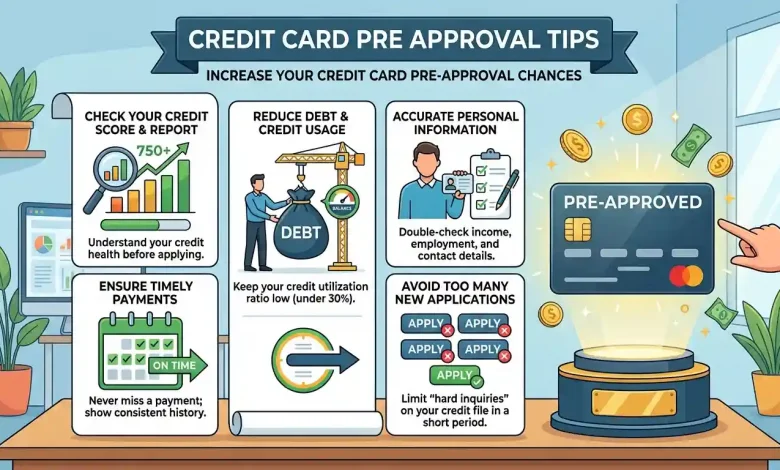

7 Powerful Credit Card Pre-Approval Tips – Boost Approval Odds Fast

Table of Contents

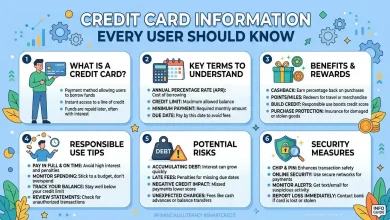

Credit Card Pre Approval Tips are essential for anyone looking to secure new credit with greater confidence and better terms. In the competitive landscape of personal finance, receiving a pre-approval for a credit card can feel like a golden ticket, signaling that a lender has already taken an initial look at your financial profile and deemed you a strong candidate. This initial nod can significantly boost your confidence before a formal application, potentially saving you from a credit-damaging hard inquiry and the disappointment of denial. Understanding the nuances of pre-approval and actively working to improve your financial standing are crucial steps in navigating this process successfully.

Pre-approval is not a guarantee of final approval, but it’s a powerful indicator. It suggests that, based on certain criteria, you meet the basic requirements set by the credit card issuer. By proactively implementing strategies to enhance your creditworthiness, you can move from merely hoping for a pre-approval to strategically increasing your chances of receiving favorable offers and ultimately, securing the credit card that best suits your needs. This comprehensive guide will delve into the critical factors that influence pre-approval decisions and provide actionable tips to optimize your financial profile, making you a more attractive prospect for credit card issuers.

Understanding Credit Card Pre-Approval

Credit card pre-approval is an offer from a credit card issuer suggesting that you meet some of their basic eligibility criteria for a specific card. These offers often come in the mail or via email and are typically the result of a “soft inquiry” (also known as a “soft pull” or “soft credit check”) on your credit report. A soft inquiry allows lenders to review your creditworthiness without impacting your credit score.

It’s important to differentiate between pre-approval, pre-qualification, and actual approval. While many card issuers use the terms interchangeably, there can be subtle differences. Pre-qualification usually involves you initiating the process by providing some basic financial details to the card issuer, often through an online tool. The issuer then performs a soft inquiry to see if you might be eligible for certain cards. Pre-approval, on the other hand, often originates from the issuer who has already reviewed your credit information and identified you as a potential candidate, sending you an unsolicited offer. Both pre-qualification and pre-approval involve a soft credit check and do not harm your credit score. However, neither guarantees final approval. Once you formally apply for a pre-approved offer, the issuer will conduct a “hard inquiry” (or “hard pull”) on your credit report, which can temporarily lower your credit score by a few points and remains on your report for up to two years.

Understanding this distinction is vital. A pre-approved offer is a strong indication that you’re likely to be approved if you proceed with the full application, provided your financial situation hasn’t drastically changed since the soft inquiry. It’s an opportunity to gauge your chances without the risk of a credit score dip from a hard inquiry on a speculative application.

Key Factors Influencing Your Pre-Approval Chances

Credit card issuers consider several factors when evaluating you for a pre-approval or a formal application. By understanding and optimizing these areas, you can significantly increase your likelihood of receiving favorable offers.

The Pivotal Role of Your Credit Score

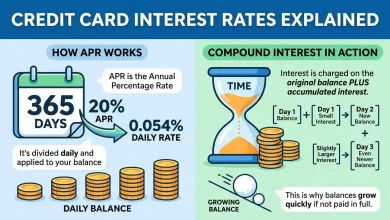

Your credit score is arguably the most significant factor in credit card approval. It’s a numerical representation of your creditworthiness, indicating to lenders how likely you are to repay borrowed money. FICO and VantageScore are the most common scoring models. While there’s no universal minimum score for pre-approval, generally, higher scores correlate with better approval odds and more attractive card offers, such as lower interest rates and higher credit limits. For instance, people with credit scores of 700 and above are often easily approved for low-interest, high-limit credit cards. A good FICO score typically ranges from 670-739, with 740-799 considered “very good” and 800-850 as “exceptional.”

Length of Credit History

Lenders prefer to see a longer credit history because it provides more data to assess your repayment habits and financial responsibility. The length of your credit history includes the age of your oldest account, your newest account, and the average age of all your accounts. Generally, a credit history of seven to ten years is considered good for most top-tier financial products. If you have a limited credit history, issuers might be hesitant, as you haven’t yet proven your long-term creditworthiness. However, some cards are designed for individuals with little to no credit history, such as secured credit cards, which can help you build credit responsibly.

Payment History and Consistency

Your payment history is a critical component, often carrying the most weight in credit score calculations. Consistently paying your bills on time demonstrates reliability and responsibility. Late payments, missed payments, or delinquencies can significantly harm your credit score and signal a red flag to potential lenders, making you appear less creditworthy. Even a single late payment can have a noticeable negative impact.

Credit Utilization Ratio (CUR)

Your Credit Utilization Ratio (CUR) is the percentage of your available credit that you are currently using. It’s calculated by dividing your total credit used by your total credit limit and is a key factor, accounting for a significant portion (around 30%) of your credit score. Lenders generally prefer to see a low CUR, ideally below 30%, and even better, under 10%. A high CUR suggests financial stress or over-reliance on borrowed money, which can negatively impact your score and approval chances. Reducing outstanding debt to keep this ratio low is a primary tip for increasing approval odds.

Debt-to-Income (DTI) Ratio

The Debt-to-Income (DTI) ratio compares your total monthly debt payments to your gross monthly income. Lenders use this ratio to assess your ability to take on and repay new debt. A high DTI can signal that you may have limited funds to manage additional debt, making lenders hesitant to approve new credit. While DTI requirements vary, many lenders prefer a DTI of 35% or less. A DTI of 50% or more is often seen as problematic and can severely limit your borrowing options.

Income and Employment Stability

Credit card applications will typically ask for your household income and employment status. Lenders assess your income to ensure you have the financial capacity to make monthly payments. Stable employment and a consistent income demonstrate reliability and a steady ability to repay debt, which are favorable in the eyes of card issuers. Some issuers even have minimum income requirements for certain cards.

Relationship with the Issuer

Your existing relationship with a bank or credit union can sometimes play a role. If you already have a checking account, savings account, or another product with an issuer, they may have more insight into your financial habits and be more likely to send you pre-approved offers.

Strategies to Improve Your Credit Score for Pre-Approval

Improving your credit score is a continuous process that involves disciplined financial habits. Here are actionable steps to take:

- Pay Bills On Time, Every Time: This is fundamental. Payment history is the most important factor in your credit score. Set up automatic payments or reminders to ensure you never miss a due date on credit cards, loans, and even utility bills.

- Reduce Credit Card Balances: Aim to keep your credit utilization ratio (CUR) low. Pay down existing credit card debt, especially on cards with high balances, before the statement closing date. Ideally, keep your CUR below 30%, with under 10% being excellent.

- Review Your Credit Reports Regularly: Obtain your free credit reports from Equifax, Experian, and TransUnion annually via AnnualCreditReport.com. Scrutinize them for any errors, unauthorized accounts, or fraudulent activity. Dispute any inaccuracies immediately, as these can negatively impact your score.

- Avoid New Debt: In the months leading up to a credit card application, try to avoid opening new credit accounts or adding substantial balances to existing ones. This can signal stability to lenders.

- Maintain a Good Credit Mix: While not as influential as payment history or CUR, having a mix of credit types (e.g., credit cards, installment loans like a car loan or mortgage) can positively impact your score over time.

- Keep Old Accounts Open: The length of your credit history benefits from older accounts. Even if you no longer use an old credit card, keeping it open (especially if it has no annual fee) can help maintain a longer average credit age. Closing older accounts can potentially shorten your credit history and negatively affect your score.

Optimizing Your Credit Utilization Ratio

The Credit Utilization Ratio (CUR) is a powerful lever for your credit score. Lenders consider a high CUR a sign of financial instability, indicating you might be a high-risk borrower. To lower your CUR effectively:

- Pay Down Balances: The most direct way is to reduce the outstanding debt on your credit cards. Even small payments can make a difference.

- Make Multiple Payments Per Month: Instead of waiting for the statement due date, make several payments throughout the billing cycle. This can ensure a lower balance is reported to the credit bureaus.

- Request a Credit Limit Increase: If your credit score has improved and your payment history is solid, you might request an increase in your credit limit on an existing card. If approved, and you maintain your spending, your CUR will decrease. However, only do this if you trust yourself not to increase your spending along with the new limit.

- Avoid Maxing Out Cards: Even temporarily maxing out a card can hurt your score if it gets reported to the credit bureaus. Try to keep your balances well below your limits.

Managing Your Debt-to-Income Ratio (DTI)

Your DTI ratio is another critical metric that credit card issuers scrutinize. A low DTI indicates that you have more disposable income available to handle new debt obligations, making you a less risky borrower. Here’s how to manage it:

- Understand Your DTI: Calculate your DTI by summing all your monthly debt payments (e.g., rent/mortgage, car loans, student loans, minimum credit card payments) and dividing that by your gross monthly income.

- Reduce Existing Debt: Focus on paying down installment loans and credit card balances. This directly lowers your monthly debt payments.

- Increase Your Income: While not always quick or easy, increasing your gross monthly income can naturally lower your DTI.

- Avoid New Loans or Credit: Resist taking on new loans or lines of credit until after you’ve secured the credit card you desire, as this will increase your monthly debt obligations.

A DTI of 35% or less is generally considered good by lenders, with 36%-41% being acceptable but potentially requiring additional scrutiny. A DTI above 50% often indicates significant financial strain and can make it challenging to obtain new credit.

| Credit Factor | Description | Ideal State for Pre-Approval | Impact on Pre-Approval |

|---|---|---|---|

| Credit Score | A numerical representation of creditworthiness. | ≥ 700 (Very Good to Exceptional) | Higher scores lead to better offers and approval odds. |

| Credit Utilization Ratio (CUR) | Percentage of available credit being used. | < 30%, ideally < 10% | Low CUR shows responsible credit use, boosts score. |

| Payment History | Record of on-time or late payments. | 100% on-time payments | Most significant factor; consistent on-time payments are crucial. |

| Debt-to-Income Ratio (DTI) | Monthly debt payments vs. gross monthly income. | < 35% | Lower DTI indicates ability to manage new debt. |

| Length of Credit History | Age of oldest account and average age of accounts. | 7-10+ years | Longer history demonstrates experience and reliability. |

| Income Stability | Consistent and sufficient earnings. | Steady employment and adequate income | Ensures ability to make minimum payments. |

Strategic Application Practices

Beyond improving your underlying credit health, how you approach the application process itself can influence your success rate.

- Research Cards Within Your Credit Range: Don’t just apply for aspirational cards. Use online tools to check for pre-qualified offers or cards that cater to your current credit score range. Applying for cards that align with your credit profile significantly increases your approval odds. Many issuers offer resources to help you understand which cards you might qualify for based on your credit health.

- Avoid Submitting Too Many Applications: Each formal application results in a hard inquiry on your credit report, which can slightly lower your score. Multiple hard inquiries in a short period can appear alarming to lenders, suggesting you might be desperate for credit or a higher risk. Space out your applications if you need to apply for several cards.

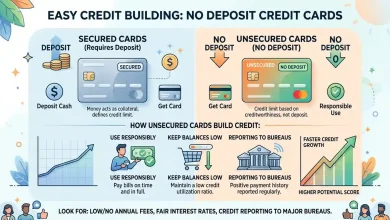

- Consider Secured Credit Cards for Rebuilding Credit: If your credit score is low or you have a limited credit history, a secured credit card can be an excellent starting point. These cards require a refundable security deposit, which typically acts as your credit limit. They are easier to get approved for and, when used responsibly (making on-time payments and keeping utilization low), can help build or rebuild your credit score, making you eligible for unsecured cards later. Many secured cards report to all three major credit bureaus, aiding in credit building.

- Be Truthful on Applications: Always provide accurate income and personal information on your application. Lenders verify this data, and inconsistencies can lead to denial or even accusations of fraud.

Conclusion

Navigating the world of credit card pre-approvals and applications requires a strategic approach grounded in understanding and improving your financial health. By focusing on key areas such as your credit score, payment history, credit utilization, and debt-to-income ratio, you can transform your credit profile and significantly increase your chances of not only receiving pre-approval offers but also securing the credit cards you desire with favorable terms. Remember that pre-approval is a strong hint, not a guarantee, but it empowers you to apply with greater confidence. Regularly monitoring your credit report, diligently managing your debts, and making informed application decisions are paramount to building and maintaining a strong credit foundation for your financial future.