6 Simple Ways Credit Card Interest Rates Work – Beginner’s Guide

Table of Contents

Credit card interest rates are a fundamental aspect of owning and using a credit card, yet for many beginners, they remain a source of confusion. Understanding how these rates work is crucial for managing your finances effectively, avoiding unnecessary debt, and building a strong financial future. When you use a credit card, you are essentially borrowing money from the card issuer. The interest rate is the cost you pay for this privilege, applied to any outstanding balance you carry from one billing cycle to the next. Failing to grasp the intricacies of credit card interest can lead to a snowball effect of debt, making it harder to pay off what you owe. This comprehensive guide aims to demystify credit card interest rates, breaking down complex concepts into easily digestible information for beginners. We will explore what interest rates are, how they are calculated, the different types you might encounter, and most importantly, strategies to minimize the amount you pay in interest.

Introduction to Credit Card Interest Rates

Credit card interest is essentially the fee charged by credit card companies when you borrow money and do not pay off your full balance by the due date. It is the price you pay for the convenience and flexibility that a credit card offers, allowing you to make purchases now and pay for them later. If you consistently leave an unpaid balance at the end of each billing cycle, this interest can quickly accumulate, adding to your overall debt.

The concept of credit card interest is central to how credit cards operate. Unlike other loans where you might have a fixed repayment schedule, credit cards offer revolving credit. This means you can continuously borrow up to your credit limit, repaying a portion each month, and then borrow again. This flexibility comes with the caveat of interest charges if you don’t manage your payments diligently. For instance, if you carry a $5,000 credit card balance with a 20% interest rate, you could incur an additional $1,000 in interest over a year. The average credit card interest rate has been a significant factor in recent years, with the average hovering around 19.19% as of May 2026, though it can range from 12.20% to 34.52% depending on various factors.

What is APR? Understanding the Annual Percentage Rate

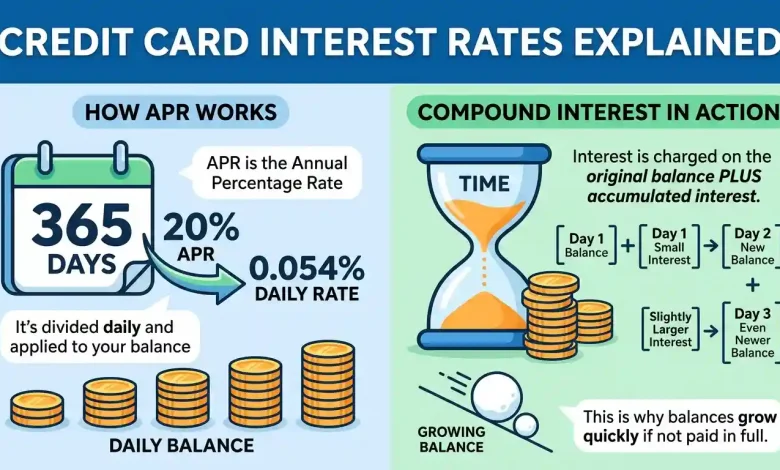

The most commonly used term for credit card interest is the Annual Percentage Rate, or APR. The APR represents the yearly cost of borrowing money on your credit card, expressed as a percentage. While the APR is an annual rate, credit card issuers typically charge interest on a daily basis, as your balance can fluctuate from day to day. A higher APR means it will be more expensive to maintain a balance on your card.

It’s important to note that a single credit card may have several different APRs depending on the type of transaction. These commonly include:

- Purchase APR: This is the standard interest rate applied to purchases you make with your card. You’ll generally only be charged this rate if you carry a balance beyond the grace period.

- Balance Transfer APR: This rate applies when you transfer debt from one credit card to another. Often, cards offer a promotional 0% or low balance transfer APR for an introductory period, but a regular rate will apply afterward. Interest on balance transfers typically accrues immediately, without a grace period.

- Cash Advance APR: This is the rate charged when you use your credit card to get cash, for example, at an ATM. Cash advance APRs are usually significantly higher than purchase APRs and interest often begins accruing immediately, without a grace period.

- Introductory APR: Many credit cards offer a temporary low or 0% APR on purchases or balance transfers for a set period (e.g., 6 to 24 months) to attract new cardholders. Once this promotional period ends, the standard APR applies to any remaining balance.

- Penalty APR: Some cards may impose a penalty APR if you miss a minimum payment by 60 days or more. This rate is typically much higher than your standard purchase APR. Under the Credit CARD Act of 2009, if a card issuer raises your rate due to a 60-day late payment, they must restore the original rate after six months of on-time payments.

Understanding these different APRs is vital for managing your credit card usage and minimizing potential interest charges. The APR provides a more complete picture of your borrowing costs than just the interest rate alone, as it can sometimes include fees. However, for credit cards, the APR and interest rate are often the same because they typically don’t have the same fees as other loans like mortgages.

Types of Credit Card Interest Rates

Beyond the various APRs for different transaction types, credit card interest rates can also be categorized by their nature: fixed or variable.

- Variable Interest Rates: Most credit cards today come with variable APRs. A variable interest rate fluctuates over time, tied to an underlying index, such as the prime rate. The prime rate is a benchmark interest rate that banks use for their most creditworthy customers, and it’s heavily influenced by the federal funds rate set by the Federal Reserve. If the prime rate increases, your card’s variable APR will likely increase, and vice versa. This means your interest costs can change without direct action from you, making it harder to predict your monthly payments if you carry a balance.

- Fixed Interest Rates: Fixed interest rates, as the name suggests, are designed to remain consistent. While they may change, your card issuer is typically required to notify you beforehand. However, truly fixed-rate credit cards are relatively uncommon in the market today, especially compared to personal loans or mortgages. Even rates advertised as “fixed” can still change under certain circumstances, such as missed payments or the end of a promotional period.

Many credit cards also offer promotional or introductory APRs, often 0%, for a limited time on new purchases or balance transfers. These can be a valuable tool for managing debt or financing a large purchase without immediate interest. However, it’s crucial to understand when the introductory period ends and what the regular APR will be afterward, as any remaining balance will then accrue interest at the higher rate. Some deferred interest cards might even charge all accrued interest from the purchase date if the balance isn’t paid in full by the end of the promotional period.

How Interest is Calculated on Your Credit Card

Understanding how credit card interest is calculated is perhaps the most critical step for beginners. Most credit card issuers use the “average daily balance method” to determine your monthly interest charges. This method calculates interest based on your balance each day of the billing cycle, effectively compounding daily.

Here’s a step-by-step breakdown of how interest is typically calculated using the average daily balance method:

- Convert APR to Daily Periodic Rate (DPR): The first step is to convert your annual APR into a daily rate. You do this by dividing your APR by 365 (the number of days in a year).

Example: If your APR is 20%, your daily rate would be 0.20 / 365 = 0.0005479 or approximately 0.055% per day. - Determine Your Average Daily Balance: For each day of your billing cycle, your card issuer tracks your balance. This includes new purchases, payments, credits, and any accrued interest from the previous day if interest is compounded daily. To find your average daily balance, they sum up your unpaid balance for each day in the billing cycle and then divide that total by the number of days in the billing cycle.

Example: If you have a balance of $1,000 for 15 days and $500 for the remaining 15 days of a 30-day billing cycle, your average daily balance would be (($1,000 * 15) + ($500 * 15)) / 30 = $750. - Calculate Your Monthly Interest Charge: Finally, multiply your average daily balance by the daily periodic rate and then by the number of days in the billing cycle.

Example: Using the previous examples, if your average daily balance is $750, your daily rate is 0.0005479, and your billing cycle is 30 days, your monthly interest would be $750 * 0.0005479 * 30 = $12.33.

It’s important to understand the concept of a “grace period”. Most credit cards offer an interest-free grace period, which is the time between the end of your billing cycle and your payment due date. If you pay your full statement balance by the due date within this grace period, you will not be charged interest on new purchases. However, cash advances and balance transfers typically do not have a grace period, meaning interest starts accruing immediately. If you carry even a small balance from one month to the next, you may lose your grace period on new purchases until you pay the balance in full.

Factors Influencing Credit Card Interest Rates

Several key factors determine the interest rate you receive on a credit card. These can vary based on market conditions, your personal financial profile, and the policies of the card issuer.

Here are the primary influences:

- Credit Score: Your credit score is one of the most significant determinants of your credit card interest rate. Individuals with higher credit scores are generally seen as lower risk by lenders and tend to qualify for lower interest rates. Conversely, those with fair or poor credit scores often face higher rates, sometimes in the 20% to 30% range.

- Prime Rate and Market Conditions: As mentioned earlier, most credit card APRs are variable and tied to the prime rate, which in turn is influenced by the federal funds rate set by the Federal Reserve. When the Federal Reserve raises benchmark rates, credit card APRs typically move in the same direction. This means that broader economic conditions can directly impact how much interest you pay.

- Type of Card: The kind of credit card you have can also affect its APR. Rewards credit cards, which offer benefits like cash back or travel miles, often come with higher interest rates to offset the cost of their rewards programs. Student credit cards, designed for individuals with limited credit history, can also have high interest rates, sometimes reaching 29%. Cards with no rewards, on the other hand, may offer lower rates.

- Card Issuer Policies: Each credit card issuer sets its own rate structures and policies. This means that even with a similar credit profile, you might be offered different rates by different lenders.

- Debt-to-Income Ratio: Lenders also consider your debt-to-income ratio, which is how much of your income goes toward debt payments. Higher ratios can signal increased risk, potentially leading to higher interest rates.

It’s worth noting that high credit card interest rates can also be influenced by factors such as compensation for average default losses, the costs of credit card rewards, and significant marketing expenses incurred by card issuers.

| APR Type | Description | Interest Accrual | Typical Rate |

|---|---|---|---|

| Purchase APR | Rate on everyday purchases if you carry a balance. | After grace period if balance not paid in full. | Variable, often 18-29% |

| Balance Transfer APR | Rate for debt transferred from another card. | Immediately, unless 0% intro offer. | Varies, promotional 0% for 6-24 months possible |

| Cash Advance APR | Rate for withdrawing cash from your credit card. | Immediately, no grace period. | Usually higher than purchase APR |

| Introductory APR | Temporary low or 0% rate for new cardholders. | During promotional period, then regular APR. | Often 0% for a set period |

| Penalty APR | Elevated rate applied after late payments (e.g., 60 days). | Applies to new purchases after triggering event. | Significantly higher than standard rates |

Avoiding or Minimizing Credit Card Interest

The best way to avoid paying credit card interest altogether is to pay your full statement balance by the due date every month. This allows you to take full advantage of your card’s grace period, meaning you won’t be charged interest on new purchases. However, if paying in full isn’t always possible, there are several strategies to minimize the interest you accrue:

- Pay More Than the Minimum Payment: While making the minimum payment keeps your account in good standing and avoids late fees, it does little to reduce your principal balance, with a large portion going towards interest. Paying more than the minimum whenever possible significantly reduces the total interest you pay and helps you get out of debt faster. Even small additional payments can make a dramatic difference over time.

- Utilize 0% Introductory APR Offers Wisely: If you plan to make a large purchase or need time to pay off existing debt, a credit card with a 0% introductory APR on purchases or balance transfers can be beneficial. Be sure to pay off the balance before the promotional period ends to avoid interest charges.

- Consider Balance Transfers: If you have high-interest debt on one card, transferring it to another card with a lower or 0% balance transfer APR can provide an interest-free window to pay down the principal. Be aware of any balance transfer fees, which typically range from 3% to 5% of the transferred amount.

- Avoid Cash Advances: As discussed, cash advances come with higher APRs and no grace period, making them an expensive way to borrow money. It’s best to avoid them whenever possible.

- Make Multiple Payments During the Billing Cycle: Since interest accrues daily, making payments throughout the month can reduce your average daily balance, thereby lowering the total interest charged.

- Improve Your Credit Score: A better credit score can help you qualify for credit cards with lower standard APRs. Regularly checking your credit report and ensuring on-time payments contribute to a healthy credit score.

- Negotiate Your Interest Rate: If you have a good payment history, you might be able to call your credit card issuer and ask for a lower interest rate. This strategy can sometimes be effective, especially if you have an excellent credit score.

The Impact of Minimum Payments on Interest

While making the minimum payment on your credit card bill might seem like a responsible way to keep your account in good standing, it can be a financially detrimental habit in the long run. Credit card companies often calculate minimum payments as a small percentage of your outstanding balance, typically between 1% and 4%, plus any interest and fees owed.

The primary issue with minimum payments is that a significant portion of your payment often goes towards covering interest charges and fees, leaving very little to reduce your principal balance. This means that while you are making payments, your actual debt shrinks very slowly, or in some cases, barely at all. For example, if you have a $5,000 credit card balance with a 20% APR and only make a 2% minimum payment, your first payment might be $100. However, most of that $100 would be consumed by interest, with only a small fraction applied to the principal. At this rate, it could take more than a decade and thousands of dollars in interest to pay off the debt. Some calculations suggest it could take over 55 years and cost more than quadruple your original principal in interest alone.

This phenomenon can lead to a “cycle of debt,” where balances never seem to decrease, and you find yourself paying for purchases made months or even years ago. This extended repayment period due to minimum payments significantly increases the total cost of borrowing, making everything you buy with your credit card far more expensive. The compounding effect of high interest rates on minimum payments can create a “debt spiral” that is incredibly challenging to escape.

To truly understand the long-term cost, consider this: if you have a $5,000 debt at 20% interest and only pay the minimum, you could end up paying thousands in interest and take many years to clear the debt. This highlights why financial experts strongly recommend paying more than the minimum whenever possible. Even if you cannot pay off the full balance, increasing your payment beyond the minimum can significantly reduce the total interest paid and accelerate your debt repayment journey. For further insights into the long-term implications of minimum payments, you can refer to resources like the Consumer Financial Protection Bureau’s guidance on credit card interest and fees.

Conclusion: Mastering Credit Card Interest Rates

Navigating the world of credit cards can be daunting for beginners, but a solid understanding of credit card interest rates is your most powerful tool for responsible credit management. We’ve explored that credit card interest is essentially the cost of borrowing, primarily expressed as an Annual Percentage Rate (APR). This APR isn’t a single, fixed number but can vary significantly based on transaction type (purchases, balance transfers, cash advances), promotional offers, and whether the rate is fixed or variable, often tied to economic benchmarks like the prime rate.

Crucially, we’ve broken down how interest is calculated using the average daily balance method, emphasizing the importance of the daily periodic rate and the grace period. Remembering that paying your full statement balance by the due date can allow you to avoid interest on purchases altogether is a golden rule for all cardholders. We’ve also highlighted the various factors influencing your interest rate, from your personal credit score and the type of card you hold to broader market conditions.

Perhaps most importantly, we’ve underscored the profound impact of minimum payments. While they keep your account current, they significantly prolong your debt and dramatically increase the total interest you pay over time. By consciously choosing to pay more than the minimum, utilizing introductory APRs strategically, avoiding costly cash advances, and maintaining a healthy credit score, you empower yourself to minimize interest charges.

Mastering credit card interest rates is not just about understanding the numbers; it’s about making informed financial decisions that safeguard your financial well-being. By applying the knowledge shared in this article, beginners can confidently use credit cards as a valuable financial tool rather than a source of accumulating debt, paving the way for a more secure financial future.