7 Smart Ways to Navigate $2000 Credit Card Approval Options

Table of Contents

Credit cards with a $2000 limit are often sought by individuals looking for greater purchasing power, whether to manage larger expenses, improve their credit utilization ratio, or simply have more financial flexibility. While the term “guaranteed approval” is frequently used in online searches, it’s crucial to understand what this truly means in the context of credit card applications. Generally, no legitimate credit card offers “guaranteed approval” without some form of assessment, as lenders always need to evaluate risk. However, certain types of cards, particularly secured credit cards, come very close to this promise by minimizing the risk for the issuer through a security deposit.

Understanding “Guaranteed Approval” in Credit Cards

The concept of “guaranteed approval” in the credit card industry can be misleading. While some cards are advertised this way, it’s important to recognize that a genuine guarantee of approval without any conditions is rare, if not nonexistent, for traditional unsecured credit cards. Lenders are legally and financially obligated to assess an applicant’s ability to repay debt. This assessment typically involves reviewing credit scores, credit history, income, and debt-to-income ratios.

However, the term “guaranteed approval” is most commonly associated with secured credit cards. For these cards, approval is highly likely because you provide a refundable security deposit that acts as collateral. This deposit typically matches your credit limit, significantly reducing the risk for the lender. As long as you meet basic eligibility requirements like age and residency, and can provide the security deposit, your chances of approval are very high. Even in these cases, there isn’t a 100% guarantee, as an issuer might still decline an application if there are issues like fraud concerns or a failure to meet basic identity verification requirements.

For unsecured credit cards, what some might perceive as “guaranteed approval” usually refers to “pre-approval” or cards with very lenient qualification criteria, often aimed at those with limited or poor credit. Pre-approval means you are likely to be accepted, but it is not a definite guarantee, as a full credit check is still performed during the application process.

Factors Influencing a $2000 Credit Limit

Achieving a $2000 credit limit, whether initially or through increases, depends on several key factors that credit card issuers evaluate. These factors help lenders gauge your creditworthiness and your ability to manage higher lines of credit.

- Credit Score and History: A higher credit score and a positive credit history are paramount. Lenders examine your payment history, the length of your credit history, your credit mix, and recent credit inquiries. A strong track record of on-time payments and responsible credit use signals to lenders that you are a reliable borrower.

- Income and Debt-to-Income Ratio: Your income level plays a significant role, as it indicates your ability to repay borrowed funds. Lenders also consider your debt-to-income (DTI) ratio, which compares your monthly debt payments to your gross monthly income. A lower DTI ratio generally improves your chances of securing a higher credit limit.

- Credit Utilization: This refers to the amount of credit you’re using compared to your total available credit. Keeping your credit utilization low (ideally below 30%) demonstrates responsible credit management and can positively influence your credit limit.

- Relationship with the Lender: An existing banking relationship with a financial institution can sometimes lead to better credit card offers and higher limits, as the lender has more insight into your financial habits.

- Type of Credit Card: Different types of credit cards naturally come with varying credit limit ranges. Premium travel cards or business cards often start with higher limits, typically $5,000 or more, while secured cards or cards for those with bad credit may start with lower limits.

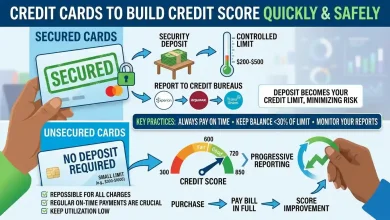

Secured Credit Cards for a $2000 Limit

For individuals with poor credit, no credit history, or those looking for a near-“guaranteed approval” option for a $2000 limit, secured credit cards are often the most viable path. These cards require a security deposit, which typically becomes your credit limit. Therefore, to get a $2000 limit on a secured card, you generally need to provide a $2000 deposit.

Several secured credit cards are known to offer limits up to or exceeding $2000, provided you make the corresponding deposit. Some examples include:

- Discover it® Secured Credit Card: This card offers a credit limit equal to your security deposit, up to a maximum of $2,500, and is reviewed for graduation to an unsecured card after seven months. It also offers cash back rewards, which is a rare feature for secured cards.

- OpenSky® Secured Visa® Credit Card: Notably, the OpenSky Secured Visa Credit Card does not require a credit check for approval, making it accessible to a broader range of applicants. Its credit limit can go up to $3,000, depending on your deposit.

- First Progress Platinum Select Mastercard® Secured Credit Card: This card allows a credit line between $200 and $2,000, equal to the security deposit. It’s an easy card to get approved for as it requires no credit history or minimum credit score.

- U.S. Bank Secured Visa® Card: This card allows you to choose a credit limit between $300 and $5,000, matching your security deposit, and has no annual fee.

Secured cards are excellent tools for building or rebuilding credit because most issuers report your payment activity to the major credit bureaus. Responsible use, such as making on-time payments and keeping your utilization low, can lead to a higher credit score and potentially allow you to graduate to an unsecured card in the future, getting your deposit back.

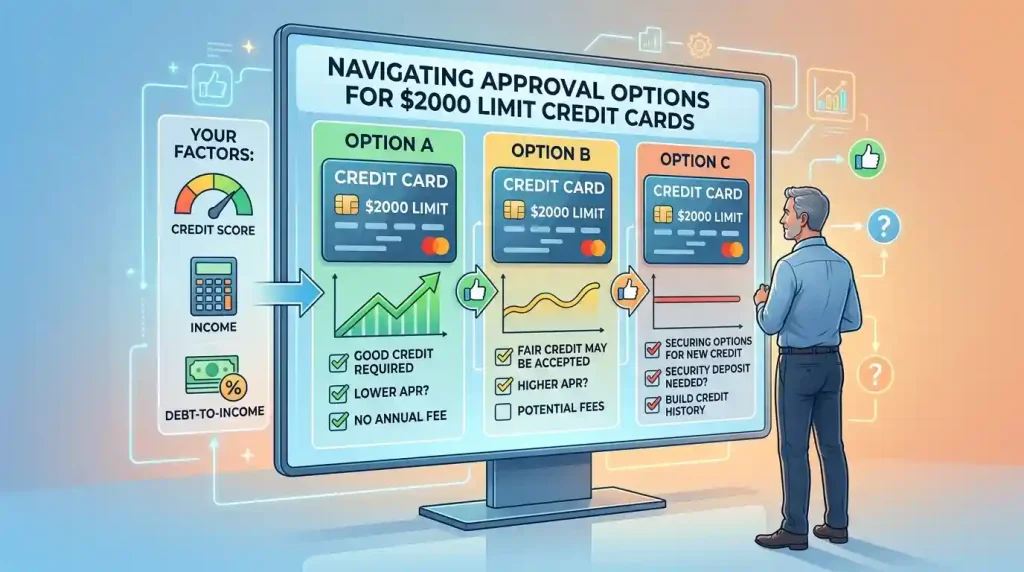

Unsecured Credit Cards and the $2000 Limit

For unsecured credit cards (which do not require a security deposit), obtaining a $2000 limit with bad or limited credit is significantly more challenging. Most unsecured cards for those with less-than-perfect credit typically start with lower limits, often in the range of $200-$500.

However, some unsecured cards designed for fair credit or those building credit may offer the potential for a $2000 limit, though it’s usually not guaranteed as an initial limit. For instance, cards like the Petal® 2 “Cash Back, No Fees” Visa® Credit Card offer limits ranging from $300 to $10,000, with the actual limit determined after approval based on various factors, including your “Cash Score” (which analyzes your banking history). The Capital One QuicksilverOne Cash Rewards Credit Card is another option for fair credit that may offer consideration for a higher credit line after as little as six months of responsible use.

If you have fair to good credit, your options for starting with or quickly reaching a $2000 limit expand. Many cards geared towards individuals with good credit often have minimum credit limits of $500 or more, and your individual creditworthiness could lead to an initial limit of $2000 or higher. Some premium cards even have minimum limits starting at $5,000 or $10,000.

Here’s a comparison of card types and their typical paths to a $2000 limit:

| Card Type | Credit Score Range | Path to $2000 Limit | Key Characteristic |

|---|---|---|---|

| Secured Credit Cards | Poor to Fair/No Credit | Deposit $2000 as collateral. | Requires security deposit; high approval odds. |

| Unsecured (Credit Builder/Fair Credit) | Poor to Fair Credit (580-669 FICO) | Start with lower limit ($300-$1000), build credit, then request increase or be offered one. | No deposit required; initial limits often lower but can grow. |

| Unsecured (Good/Excellent Credit) | Good to Excellent Credit (670+ FICO) | May qualify for $2000+ limit initially. | No deposit; higher starting limits and better terms. |

Strategies to Increase Your Credit Limit to $2000+

If your initial credit limit is lower than $2000, there are several effective strategies you can employ to increase it over time. Credit card issuers often review accounts for potential limit increases, and you can also request one yourself.

- Consistent On-Time Payments: This is arguably the most critical factor. Paying your bills on time every month demonstrates reliability and responsible financial behavior.

- Keep Credit Utilization Low: Aim to keep your credit card balances well below 30% of your available credit. Low utilization indicates that you are not overly reliant on credit and can manage your finances effectively.

- Increase Your Income and Update Information: If your income increases, update this information with your credit card issuer. A higher income can make lenders more comfortable extending a larger credit line.

- Reduce Other Debt: A lower debt-to-income ratio improves your overall financial profile, making you a more attractive candidate for a higher credit limit.

- Use Your Card Regularly (but Responsibly): While keeping utilization low, actively using your card for purchases and paying it off shows the issuer that you need and can handle a higher limit.

- Build a Longer Credit History: The length of your credit history positively impacts your credit score and demonstrates a sustained period of responsible borrowing.

- Request a Credit Limit Increase: After several months (typically 6-12) of responsible use, you can formally request a credit limit increase from your issuer, often through their online portal or by phone. Be aware that this might sometimes result in a hard inquiry on your credit report, which could temporarily ding your score. However, some issuers offer increases without a hard pull.

- Demonstrate Financial Stability: Beyond credit reports, having stable employment, a consistent savings pattern, and a good overall financial picture can encourage lenders to trust you with more credit. For more insights into building financial stability and smart money management, you might find valuable resources on a reputable financial literacy platform like the Consumer Financial Protection Bureau’s credit card section.

Applying for a Credit Card with a $2000 Limit

When you’re ready to apply for a credit card with the aim of securing a $2000 limit, precision and strategy can improve your chances.

First, assess your current credit standing. If you have poor or limited credit, a secured credit card is likely your best bet for a $2000 limit, requiring a matching deposit. If your credit is fair or better, you might qualify for an unsecured card with a starting limit of $2000 or the potential to reach it quickly.

Research cards that are known for offering higher initial limits or that have a clear path to increases. While specific starting limits are not always advertised, some premium cards or cards for excellent credit often begin at $5,000 or more. For fair credit, some cards may offer initial limits around $500-$1000 with the potential for an increase to $2000 or more after six months of responsible use.

During the application process, provide accurate and complete information, especially regarding your income. Lenders use this information to determine your borrowing capacity. Avoid applying for multiple credit cards within a short period, as numerous hard inquiries can negatively impact your credit score.

If you’re initially approved for a lower limit, focus on managing the card responsibly. Make all payments on time and keep your balances low. After six to twelve months, you can then consider requesting a credit limit increase. Many cardholders find that consistent, responsible use of their card is the most reliable way to grow their credit limit over time.

Conclusion

While the phrase “guaranteed approval” is often associated with credit cards, it’s crucial to understand that true guarantees are rare, especially for unsecured cards aiming for a $2000 limit. Secured credit cards offer the closest approximation to guaranteed approval, allowing you to secure a $2000 limit by providing a matching security deposit. These cards are invaluable tools for building or rebuilding credit. For unsecured options, achieving a $2000 limit typically requires fair to excellent credit, or a demonstrated history of responsible financial behavior that leads to credit limit increases over time. By understanding the factors that influence credit limits—such as your credit score, income, debt-to-income ratio, and payment history—and by employing strategic credit management practices, you can significantly improve your chances of obtaining and maintaining a credit card with a $2000 limit or higher.