6 Powerful Ways Credit Card Interest Works – Simple Examples

Table of Contents

Credit Card Interest is a fundamental concept that every cardholder must understand to manage their finances effectively. It is essentially the cost you pay for borrowing money through your credit card. While credit cards offer unparalleled convenience and can be powerful tools for building credit and earning rewards, the interest charged on outstanding balances can quickly negate these benefits if not managed wisely. This comprehensive guide will demystify credit card interest, breaking down how it’s calculated, the different types you might encounter, and practical strategies to minimize or avoid these charges altogether.

What is Credit Card Interest?

At its core, credit card interest is the fee charged by a lender for the privilege of using their money. When you make a purchase with a credit card, you’re effectively taking out a short-term loan. If you pay off your entire balance by the due date each month, you typically won’t pay any interest on new purchases. However, if you carry a balance—meaning you don’t pay off the full amount you owe—interest begins to accrue on that unpaid portion. This interest is almost always expressed as an Annual Percentage Rate (APR), which signifies the yearly cost of borrowing.

Understanding this “cost of borrowing” is crucial because it directly impacts how much you ultimately pay for items purchased on credit. A higher APR means you’ll pay more when you carry a balance, and over time, these charges can significantly increase the total amount you owe.

How Credit Card Interest Works: Understanding APR and Grace Periods

The mechanics of credit card interest revolve primarily around two key components: the Annual Percentage Rate (APR) and the grace period.

Annual Percentage Rate (APR)

The APR is the annual rate of interest charged on your credit card balance. While it’s an annual rate, interest is typically calculated and compounded daily. Credit card APRs can vary significantly based on your creditworthiness, the type of card, and market conditions. For instance, as of May/June 2026, average credit card interest rates ranged from approximately 19.19% to 23.79% for new offers and existing balances, with variations based on credit scores. Consumers with excellent credit might qualify for rates in the mid-teens, while those with fair or poor credit could see rates in the 20% to 30%+ range.

Most credit cards feature variable APRs, meaning the rate can fluctuate based on an index like the prime rate, which is influenced by the federal funds rate set by the Federal Reserve. If the prime rate increases, your credit card’s APR is likely to increase as well. While less common for credit cards, some might offer a fixed APR, which generally remains constant, though issuers can still change it under certain circumstances with prior notification.

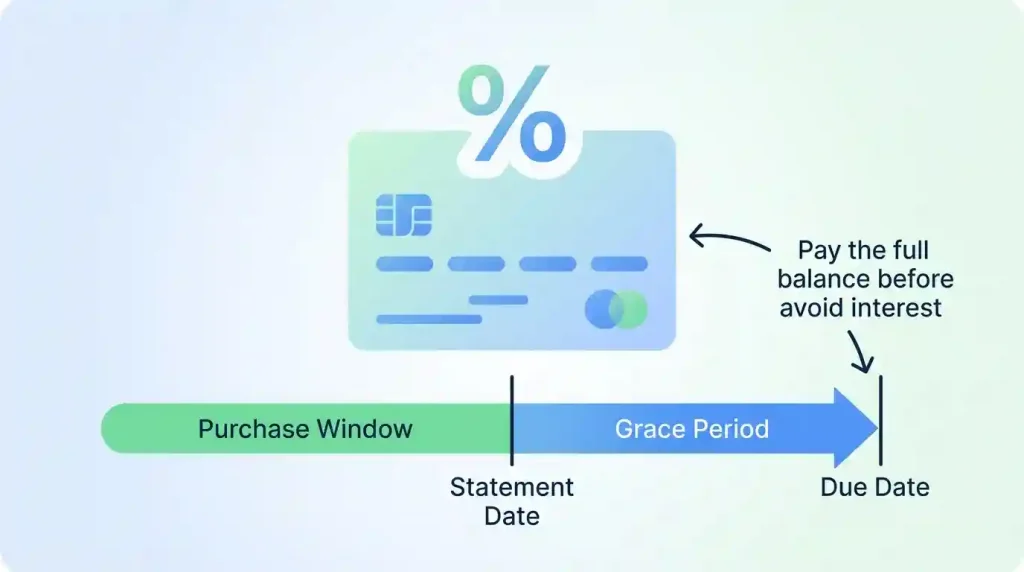

The Grace Period

A grace period is an interest-free window, typically ranging from 21 to 25 days (or even up to 30 days), between the end of your billing cycle and your payment due date. During this period, most credit card issuers do not charge interest on new purchases, provided you pay your previous statement balance in full by the due date.

This grace period is your golden ticket to avoiding interest charges. As long as you consistently pay your statement balance in full before the due date each month, you can effectively use your credit card interest-free for new purchases. However, if you fail to pay your balance in full, you usually lose this grace period, and interest may begin accruing immediately on both your outstanding balance and any new purchases. Some transactions, like cash advances, typically do not qualify for a grace period, and interest starts accumulating right away.

Calculating Credit Card Interest: The Average Daily Balance Method

The most common method credit card issuers use to calculate interest is the Average Daily Balance (ADB) method. This method involves computing interest based on the average amount you owe each day during your billing cycle. Here’s a breakdown of how it works:

- Convert APR to Daily Periodic Rate (DPR): Since interest is compounded daily, the annual APR is converted into a daily rate. This is done by dividing your APR by 365 (the number of days in a year).

Daily Periodic Rate = APR / 365 - Determine the Daily Balance: For each day in the billing cycle, your daily balance is calculated. This includes any balance carried over from the previous day, plus new purchases, fees, and minus any payments or credits.

- Calculate the Average Daily Balance: The daily balances for all days in the billing cycle are added up, and this total is then divided by the number of days in that billing cycle.

Average Daily Balance = (Sum of daily balances for billing cycle) / (Number of days in billing cycle) - Calculate Interest Charges: Finally, the interest for the billing cycle is calculated by multiplying the Average Daily Balance by the Daily Periodic Rate, and then multiplying that by the number of days in the billing cycle.

Monthly Interest Charge = Average Daily Balance × Daily Periodic Rate × Number of days in billing cycle

Simple Example 1: Paying in Full

Let’s consider a practical example. Imagine you have a credit card with an APR of 20% and a 30-day billing cycle. You start the cycle with a $0 balance. On Day 5, you make a purchase of $500. On Day 15, you make another purchase of $300. You pay your full statement balance of $800 by the due date. In this scenario, because you paid your balance in full during the grace period, you would owe $0 in interest on these purchases. This highlights the power of the grace period in helping you avoid interest charges.

Simple Example 2: Carrying a Balance

Now, let’s look at what happens if you carry a balance. Suppose you have a credit card with a 22% APR. Your billing cycle is 30 days. Let’s assume an average daily balance of $1,000 for the entire billing cycle.Daily Periodic Rate = 22% / 365 = 0.22 / 365 ≈ 0.0006027Monthly Interest Charge = $1,000 (ADB) × 0.0006027 (DPR) × 30 (days) ≈ $18.08

So, for that month, you would be charged approximately $18.08 in interest. This amount is then added to your principal balance, becoming part of the balance on which interest is charged the next day (compounding interest). This illustrates how quickly interest can add up when you don’t pay your balance in full.

The Deceptive Nature of Minimum Payments and Compound Interest

One of the most insidious aspects of credit card interest, particularly for consumers who struggle to pay their balances, is the impact of making only the minimum payment. While making the minimum payment keeps your account in good standing and avoids late fees, it does little to reduce your principal balance.

The Trap of Minimum Payments

Credit card minimum payments are typically calculated as a small percentage of your outstanding balance (often 1% to 3%) plus any accrued interest and fees, or a fixed dollar amount (e.g., $25-$35), whichever is greater. The majority of this minimum payment often goes towards covering the interest charges, leaving only a tiny fraction to pay down the actual amount you borrowed (the principal).

This creates a cycle of debt. Your balance barely decreases, or may even increase, as new interest compounds daily on the remaining high balance. Credit card statements are legally required to show how long it would take and how much it would cost to pay off your balance by only making minimum payments, and these figures can be staggering. For example, a $5,000 balance with a 20% APR making only minimum payments could take more than a decade to pay off and cost thousands in interest alone.

Compound Interest in Action

Compound interest is interest calculated on the initial principal, which also includes all of the accumulated interest from previous periods. On credit cards, this means that interest is charged on the interest you’ve already incurred. It’s a powerful force that can work for you (e.g., in savings accounts) or against you (e.g., in credit card debt).

To illustrate the long-term impact of minimum payments and compounding interest, consider the following hypothetical scenario:

| Initial Balance | APR | Minimum Payment (e.g., 2% or $25) | Estimated Time to Pay Off (Minimum Payments Only) | Estimated Total Interest Paid |

|---|---|---|---|---|

| $1,000 | 22% | $25 (or 2% of balance) | Approx. 5 years | ~$300 |

| $3,000 | 22% | $60 (2% of balance) | Approx. 19 years | ~$4,500 |

| $5,000 | 24% | $100 (2% of balance) | Approx. 20+ years | ~$7,000+ |

Note: These are approximations and actual figures depend on specific card terms, payment frequency, and balance fluctuations. The figures provided are based on general industry examples.

As you can see, the longer you only pay the minimum, the more interest you accumulate, and the longer you remain in debt. This cycle significantly increases the overall cost of your purchases. It’s a stark reminder that while minimum payments prevent delinquency, they are not a strategy for debt reduction or financial well-being. More insights into credit card debt and its broader impact can be found on resources like Wikipedia’s page on Credit Card Debt.

Different Types of Credit Card Annual Percentage Rates (APRs)

It’s important to recognize that a single credit card may have multiple APRs, each applying to different types of transactions. Understanding these variations can help you avoid unexpected charges.

- Purchase APR: This is the standard interest rate applied to new purchases if you don’t pay your statement balance in full by the due date. It’s the most common APR and typically what people refer to when discussing credit card interest.

- Cash Advance APR: When you use your credit card to withdraw cash, it’s considered a cash advance. These transactions typically come with a higher APR than purchases, and often, interest begins accruing immediately, with no grace period. Cash advance fees are also common.

- Balance Transfer APR: This rate applies when you transfer a balance from one credit card to another. Issuers often offer promotional low or 0% APRs on balance transfers to attract new customers, allowing you to pay down existing debt interest-free for a limited time. However, a balance transfer fee usually applies, and the standard balance transfer APR takes effect after the promotional period.

- Penalty APR: This is an elevated interest rate that can be triggered if you make a late payment or violate other terms of your cardholder agreement. A penalty APR is typically much higher than your standard purchase APR and may apply to your current balance and future purchases. Issuers are generally required to notify you before applying a penalty APR.

- Introductory or Promotional APR: Many credit cards offer a low or 0% introductory APR on purchases and/or balance transfers for a set period (e.g., 6, 12, or 18 months). These promotions can be very beneficial for large purchases or consolidating debt, but it’s crucial to pay off the balance before the introductory period ends, as the standard APR will then apply to any remaining balance.

Strategies to Minimize or Avoid Credit Card Interest

Effectively managing credit card interest is key to sound financial health. Here are several strategies to keep those charges at bay:

- Pay Your Statement Balance in Full Every Month: This is the single most effective way to avoid credit card interest. By paying your entire statement balance before the due date, you take full advantage of your grace period and won’t be charged interest on new purchases.

- Understand Your Billing Cycle and Due Date: Know precisely when your billing cycle ends and when your payment is due. This knowledge empowers you to make timely payments and utilize your grace period effectively. Most card issuers are required to send your bill at least 21 days before the due date.

- Set Up Automatic Payments: To avoid missing due dates, consider setting up automatic payments for your full statement balance from your checking account. This ensures you never accidentally incur interest charges or late fees.

- Pay More Than the Minimum: If paying your full balance isn’t feasible, always aim to pay more than the minimum amount due. Even a small extra payment can significantly reduce the principal balance, leading to less interest accruing over time and a faster debt payoff.

- Utilize 0% Intro APR Offers Wisely: If you have a large purchase or existing high-interest debt, a credit card with a 0% introductory APR on purchases or balance transfers can provide a valuable window to pay down debt interest-free. However, be disciplined and ensure you pay off the balance before the promotional period expires to avoid deferred interest or the regular APR kicking in.

- Consider a Balance Transfer: For existing high-interest debt, transferring your balance to a card with a lower (or 0%) introductory APR can save you a substantial amount in interest. Be mindful of balance transfer fees and the expiry of the promotional rate.

- Avoid Cash Advances: As discussed, cash advances typically come with higher APRs and no grace period, making them an expensive form of borrowing. Only use them in dire emergencies.

- Monitor Your Credit Utilization: Keeping your credit utilization ratio (the amount of credit you’re using compared to your total available credit limit) low is beneficial for your credit score and can potentially help you qualify for lower APRs in the future. Experts recommend keeping it below 30%, or ideally under 10%.

The Broader Implications of Credit Card Debt

Beyond the direct financial cost of interest, carrying credit card debt can have several far-reaching implications for your overall financial health and well-being.

Impact on Credit Score

While making minimum payments on time prevents negative marks for delinquency, consistently carrying high balances can negatively affect your credit score. A high credit utilization ratio signals to lenders that you are heavily reliant on credit, which can be seen as a risk. This can make it harder to get approved for new loans (like mortgages or auto loans) or qualify for favorable interest rates in the future.

Financial Stress

The burden of mounting credit card debt and the constant accrual of interest can lead to significant financial stress. This stress can impact various aspects of your life, from mental health to relationships, and can hinder your ability to save for future goals, such as retirement or a down payment on a home. The cycle of debt fostered by minimum payments can feel overwhelming, making financial freedom seem unattainable.

Taking proactive steps to understand and manage credit card interest is not just about saving money; it’s about gaining control over your financial future and reducing unnecessary stress.

Conclusion

Credit card interest is a fundamental component of using credit, representing the cost of borrowing money. While it can be a significant expense, a thorough understanding of how it’s calculated, the role of APR and grace periods, and the various types of interest charges empowers consumers to manage their credit effectively. By prioritizing full payments, utilizing grace periods, and being mindful of the deceptive allure of minimum payments, individuals can minimize or even completely avoid interest charges. Ultimately, responsible credit card use, informed by a clear grasp of interest mechanics, transforms these financial tools into assets that enhance, rather than hinder, personal financial health.