7 Shocking Truths About $5,000 Guaranteed Credit Cards – Reality Check

Table of Contents

Credit Cards with a $5000 limit can be a significant financial tool, offering substantial purchasing power and flexibility for consumers. Many individuals are naturally drawn to the concept of “guaranteed approval,” especially when aspiring to obtain a higher credit line. However, it’s crucial to approach the idea of “guaranteed approval” for any credit card, particularly one with a generous $5000 limit, with a clear understanding of what that truly entails in the world of personal finance. Generally, a credit score of 700 or better is typically needed for an unsecured card offering a $5,000 credit limit, alongside a high income and minimal debt.

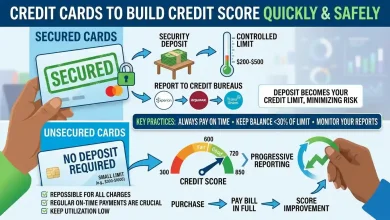

The term “guaranteed approval” is often a marketing phrase that can be misleading when it comes to unsecured credit cards with substantial limits. Most reputable lenders do not offer genuinely guaranteed approval for unsecured cards, as they must assess an applicant’s creditworthiness to mitigate risk. This assessment typically involves a review of various factors, including credit score, income, and existing debt. For those seeking “guaranteed approval” with a $5,000 limit, the closest option usually involves a secured credit card, where the credit limit is backed by a cash deposit.

The Realism of “Guaranteed Approval” for a $5000 Limit

The notion of “guaranteed approval” for an unsecured credit card with a $5,000 limit is largely a myth in the traditional sense. Credit card issuers, by nature of their business, need to evaluate an applicant’s financial stability and repayment history before extending a line of credit. This process is designed to protect both the lender and the consumer from potential financial distress. While some offers may seem to suggest guaranteed approval, these often come with caveats, such as very low initial limits, high fees, or are conditional on specific circumstances like a security deposit.

For individuals with excellent credit scores and high incomes, approval for cards with a $5,000 limit or higher is highly probable, but it is still not “guaranteed” in the strictest sense. These premium cards, such as the Chase Sapphire Preferred® Card or Chase Sapphire Reserve®, often have minimum credit limits of $5,000 or $10,000, respectively, but approval is contingent on meeting stringent credit criteria.

The most realistic path to a “guaranteed” $5,000 credit limit, particularly for those with fair or bad credit, is through a secured credit card. With a secured card, the credit limit is typically equal to the cash deposit you provide to the issuer. Therefore, by depositing $5,000, you can secure a credit card with a $5,000 limit. This method removes much of the risk for the lender, making approval far more likely, though not always absolutely guaranteed for every applicant. Banks like Bank of America and U.S. Bank offer secured cards that allow deposits up to $5,000.

Key Factors Influencing Your Credit Card Limit and Approval

Credit card issuers consider a multitude of factors when deciding whether to approve an application and what credit limit to assign. Understanding these elements is essential for anyone aiming for a $5,000 limit. The process involves a complex evaluation of your financial history and creditworthiness.

- Credit Score and History: Your credit score is a numerical representation of your creditworthiness, derived from your credit history. Lenders use it to predict the likelihood of you repaying your debts. A score of 700 or better is generally required for a $5,000 unsecured limit. A positive credit history, characterized by on-time payments and responsible credit management, significantly improves your chances.

- Income and Employment: Your income demonstrates your capacity to repay outstanding balances. Lenders want to ensure you have a stable income source to cover payments. A higher income generally correlates with a higher approved credit limit.

- Debt-to-Income (DTI) Ratio: This ratio compares your monthly debt obligations to your gross monthly income. A lower DTI ratio indicates that you are not overextended and can responsibly manage additional debt, making you a less risky borrower.

- Credit Utilization Ratio (CUR): This is the amount of credit you’re currently using compared to your total available credit. Keeping your CUR low (ideally below 30%) signals responsible credit management and can positively impact your credit score and limit.

- Length of Credit History: A longer credit history with consistent responsible behavior shows lenders a proven track record.

- Credit Mix: Having a diverse mix of credit accounts (e.g., installment loans, revolving credit) and managing them well can also be a favorable factor.

- Recent Credit Inquiries: Numerous recent credit applications can be a red flag for lenders, suggesting financial distress or a high-risk borrower.

Issuers also verify identity and may ask for additional information like your monthly housing payment.

Types of Credit Cards That Offer Higher Limits

While a $5,000 credit limit is considered substantial for many, certain types of credit cards are more prone to offering such limits either from the outset or after a period of responsible use.

1. Secured Credit Cards: As discussed, secured cards are the most straightforward way to potentially obtain a $5,000 limit, especially for those with less-than-perfect credit. Cards like the Bank of America® Unlimited Cash Rewards Secured Credit Card, U.S. Bank Cash+® Visa® Secured Card, and others allow security deposits up to $5,000, directly setting your credit limit. These cards are designed to help individuals build or rebuild their credit.

2. Premium Travel and Rewards Cards: For individuals with good to excellent credit (typically 670 FICO score or higher), premium travel and rewards cards frequently offer initial credit limits starting at $5,000 or even $10,000. Examples include the Chase Sapphire Preferred® Card (minimum $5,000 limit) and the Chase Sapphire Reserve® (minimum $10,000 limit). These cards come with various benefits, such as high rewards rates, sign-up bonuses, and travel perks, but they also require a strong credit profile for approval.

3. Business Credit Cards: Small business owners or self-employed individuals may find that business credit cards offer higher credit lines compared to personal cards, reflecting the higher spending needs associated with business operations. While not “guaranteed” approval, they can be a viable path for those with a solid business and personal credit history.

4. Unsecured Cards for Fair/Good Credit (with a path to increases): Some unsecured cards designed for fair to good credit, while starting with lower limits (e.g., $300-$1,000), offer a clear path to credit limit increases with responsible use. The Capital One Platinum Credit Card, for instance, allows cardholders to request a limit increase after a few months of on-time payments, with some reporting reaching $2,000-$3,000 limits within a year. This approach requires patience and consistent responsible financial behavior.

| Credit Card Type | Typical Initial Limit Range | Approval Likelihood for $5000 Limit (Initial) | Credit Score Requirement (General) | Key Characteristic |

|---|---|---|---|---|

| Secured Credit Cards | $200 – $5,000 (equal to deposit) | High, if deposit matches | Bad to Fair (no minimum sometimes) | Requires a cash security deposit. |

| Premium Travel/Rewards Cards | $5,000 – $10,000+ | Medium to High (with excellent credit) | Good to Excellent (700+) | Offers substantial rewards and benefits. |

| Business Credit Cards | Varies widely, often higher than personal cards | Medium to High (with strong business/personal credit) | Good to Excellent (for high limits) | Tailored for business expenses. |

| Unsecured Cards (Fair/Good Credit) | $300 – $1,500 (initially) | Low (initial), higher over time | Fair to Good (580-739) | Credit limit increases with responsible use. |

Strategies for Obtaining a $5000 Credit Card Limit

Achieving a $5,000 credit card limit, whether immediately or over time, involves strategic financial planning and responsible credit behavior. Here are key strategies:

- Utilize Secured Cards Effectively: If your credit is fair or bad, a secured credit card is your best bet for a high initial limit. Deposit the full $5,000 if you have the funds available. Maintain perfect payment history and keep your credit utilization low. After 6-18 months of responsible use, many secured cards offer a path to upgrade to an unsecured card and get your deposit back.

- Improve Your Credit Score: For unsecured cards with high limits, a good to excellent credit score (700+) is typically a prerequisite. Focus on:

- Paying all bills on time, every time. Payment history is the most significant factor in your credit score.

- Keeping credit utilization below 30%. This shows lenders you manage credit responsibly.

- Reducing existing debt to lower your debt-to-income ratio.

- Avoiding opening too many new credit accounts in a short period.

- Increase Your Income and Lower Debt: Lenders assess your capacity to repay. A higher income and lower existing debt make you a more attractive candidate for a higher credit limit.

- Request Credit Limit Increases: Once you have a credit card, consistently making on-time payments and keeping your utilization low can make you eligible for a credit limit increase. Many issuers automatically review accounts, but you can also proactively request an increase, usually after 6-12 months of opening the account. Be aware that a request might result in a “hard inquiry” on your credit report.

- Consider “Pre-qualification” Offers: While not guaranteed approval, pre-qualification allows you to see if you’re likely to be approved for certain cards without a hard inquiry on your credit report. This can help you identify cards for which you have a good chance of approval and potentially a higher limit.

- Target Premium Cards (with caution): If your credit is already strong, target premium cards known for high starting limits. Research cards like the Chase Sapphire Preferred® or Capital One Venture X Rewards Credit Card, which have minimum limits of $5,000 or $10,000. However, remember that these are not “guaranteed approval.”

Building and Maintaining Excellent Credit for Increased Limits

Achieving and maintaining a high credit limit, such as $5,000, is a continuous process rooted in strong financial habits. A healthy credit profile makes you a desirable customer for lenders, opening doors to better credit products and higher limits. The foundation of excellent credit lies in consistent, responsible financial behavior.

- Consistent On-Time Payments: This is arguably the most critical factor. Payment history accounts for 35% of your FICO score. Late or missed payments can severely damage your credit. Setting up automatic payments can help ensure you never miss a due date.

- Low Credit Utilization: Strive to keep your credit utilization ratio (CUR) below 30% across all your credit accounts. A lower CUR demonstrates that you’re not over-reliant on credit and can manage your debt effectively. If you have a $5,000 limit, try to keep your balance below $1,500.

- Manage Existing Debt: Actively work to pay down outstanding balances on loans and credit cards. A lower debt burden improves your debt-to-income ratio, signaling to lenders that you have more disposable income to handle new credit.

- Length of Credit History: The longer your credit accounts have been open and in good standing, the better. Avoid closing old credit cards, even if you don’t use them frequently, as this can negatively impact the average age of your credit accounts.

- Diversify Your Credit Mix: Having a mix of different types of credit (e.g., credit cards, auto loans, mortgages) can demonstrate your ability to manage various forms of debt. However, only take on new credit if you genuinely need it and can afford to repay it.

- Monitor Your Credit Report: Regularly review your credit reports from all three major bureaus (Experian, Equifax, and TransUnion) for errors or fraudulent activity. You can obtain a free copy of your credit report annually from AnnualCreditReport.com. Promptly dispute any inaccuracies.

- Be Patient: Building excellent credit and securing high limits takes time and consistent effort. There are no shortcuts to a strong credit profile.

Conclusion

Obtaining a credit card with a $5,000 limit, while often desired, rarely comes with “guaranteed approval” for unsecured products. The closest approximation to guaranteed approval for such a high limit lies in secured credit cards, where your deposit directly determines your credit line. For unsecured cards, a strong credit profile, characterized by a good to excellent credit score (typically 700+), a high income, low debt-to-income ratio, and a history of responsible payments, is essential.

Strategies for achieving a $5,000 limit include responsibly using secured cards to build credit, diligently improving your credit score through consistent on-time payments and low utilization, and strategically requesting credit limit increases over time. Understanding the factors that influence credit approval and credit limits—such as your credit score, income, debt, and credit history—empowers you to make informed financial decisions and work towards your goal. By committing to sound financial practices and patience, a $5,000 credit card limit becomes an achievable reality, providing the financial flexibility and purchasing power you seek.