7 Shocking Indigo Card Fees – Better Credit Building Alternatives

Table of Contents

Indigo Credit Card offers a pathway for individuals seeking to build or rebuild their credit history. In the current financial landscape, having a good credit score is paramount, influencing everything from loan approvals to housing applications and even insurance rates. For those with less-than-perfect credit, securing an unsecured credit card can be a significant challenge, often requiring a security deposit for alternatives like secured credit cards. The Indigo Mastercard stands out by providing an unsecured option for individuals who may have been turned down by traditional lenders, making it a viable stepping stone towards financial recovery and improved creditworthiness. This comprehensive guide delves into the benefits and the approval process for the Indigo Credit Card, offering insights to help you make informed decisions on your credit-building journey.

Understanding the Indigo Credit Card: A Solution for Building Credit

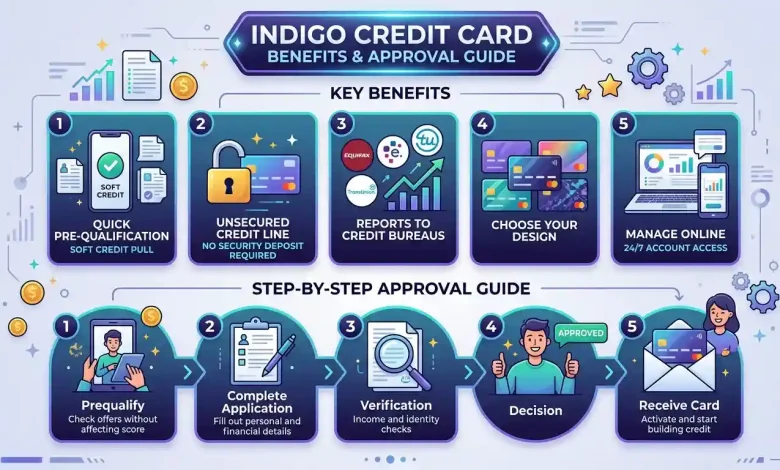

The Indigo Credit Card is specifically designed for consumers with poor or limited credit, including those who have experienced financial difficulties like bankruptcy. Unlike many credit cards aimed at this demographic, the Indigo Mastercard is an unsecured card, meaning it does not require an upfront security deposit. This feature makes it particularly accessible for individuals who may not have the cash readily available for a deposit, providing them with essential purchasing power without tying up their funds.

The primary goal of the Indigo Card is to help cardholders establish and improve their credit scores. It achieves this by reporting account activity to all three major credit bureaus in the U.S.: Experian, Equifax, and TransUnion. Consistent, on-time payments and responsible credit management can gradually build a positive payment history, which is a crucial factor in credit scoring models. This reporting mechanism is fundamental to the card’s utility as a credit-building tool, allowing users to demonstrate financial responsibility over time.

Key Benefits of the Indigo Mastercard

For individuals navigating the complexities of rebuilding or establishing credit, the Indigo Mastercard offers several compelling benefits that can make it a suitable choice.

Accessibility for Varied Credit Histories

One of the most significant advantages of the Indigo Credit Card is its accessibility. It caters to a broad spectrum of credit profiles, including those with bad credit or a limited credit history. While most unsecured cards are difficult to obtain with a low credit score, the Indigo Mastercard provides an opportunity for approval without requiring a security deposit. This makes it an attractive option for many who have struggled to get approved elsewhere.

Credit Building Opportunities

The core benefit of the Indigo Card lies in its ability to help cardholders build a positive credit history. By reporting regularly to all three major credit bureaus (Experian, Equifax, and TransUnion), the card allows consistent, on-time payments to reflect positively on a user’s credit report. Over time, this can lead to an improved credit score, opening doors to better financial products and more favorable terms in the future. This proactive approach to credit reporting is essential for anyone serious about enhancing their financial standing.

Mastercard Acceptance and Features

As a Mastercard, the Indigo Credit Card boasts wide acceptance globally, allowing cardholders to use it at millions of locations where Mastercard is accepted. This offers convenience for everyday purchases and transactions. Beyond basic acceptance, the card typically includes standard Mastercard benefits such as ID Theft Protection, which monitors for potential fraud and identity theft, and Mastercard Global Service, providing 24/7 assistance for lost or stolen cards. These features provide a layer of security and peace of mind for cardholders.

Online Account Management

Managing the Indigo Credit Card is made convenient through its online account access and mobile capabilities. Cardholders can monitor their balances, view transaction history, make payments, and access statements digitally. This accessibility empowers users to stay on top of their finances, which is crucial for responsible credit management and for making on-time payments, thereby fostering positive credit growth.

Navigating the Indigo Credit Card Approval Process

Understanding the steps involved in applying for and being approved for the Indigo Credit Card can significantly streamline the process and increase your chances of success.

Pre-Qualification: A Smart First Step

One of the most valuable features of the Indigo Credit Card application process is the option for pre-qualification. This allows potential applicants to check their eligibility without impacting their credit score, as it involves only a “soft” credit inquiry. By providing some basic personal and financial information, you can receive an initial offer within minutes. This sneak peek into your approval odds is a prudent first step, helping you assess your suitability before committing to a full application, which would involve a “hard” credit pull and could temporarily lower your score.

Eligibility Requirements

While the Indigo Credit Card is known for being accessible to those with less-than-perfect credit, there are still specific eligibility criteria that applicants must meet. Generally, applicants must be at least 18 years old, possess a valid Social Security Number, and have a physical U.S. address. Income and existing debt are also reviewed to determine the applicant’s ability to make monthly payments. Crucially, applicants typically should not have had an Indigo Mastercard account previously charged off due to delinquency. While a specific minimum credit score isn’t always explicitly published, the card is generally designed for individuals with credit scores in the poor to fair range, often cited as below 669.

For more insights on managing finances to meet credit card eligibility, you might find useful information on setting up a budget and tracking expenses by visiting this relevant article.

What to Expect During Application

After completing the pre-qualification, if you decide to proceed, you will typically submit a full application. This stage involves a hard credit inquiry, which may have a minor, temporary impact on your credit score. The application will require details such as your full name, address, email, phone number, date of birth, Social Security number, monthly income, and monthly expenses. Accuracy in providing this information is critical, as knowingly submitting false or misleading data is a federal crime. While the card is designed to help many credit-challenged individuals, approval is not guaranteed, and each application is reviewed closely against the card’s qualification criteria. If approved, you can typically expect to receive your physical card within 14 business days.

Important Fees and Interest Rates to Consider

While the Indigo Credit Card offers valuable credit-building opportunities, it’s essential to be aware of the associated fees and interest rates, which can be higher than those on cards for individuals with excellent credit. These costs can significantly impact the overall expense of maintaining the card if not managed carefully.

| Fee/Rate Type | Typical Range/Amount | Notes |

|---|---|---|

| Annual Fee | $0 – $199 (varies by creditworthiness) | Can be $175-$199 for the first year, then $49-$99 annually thereafter. Some offers might have a $0 annual fee for stronger profiles. |

| Monthly Fee | Up to $12.50/month (after first year) | Some cardholders may incur a monthly fee after the first 12 months, in addition to the annual fee. |

| Purchase APR | Typically 35.9% (variable) | This high Annual Percentage Rate means carrying a balance can be very expensive. Paying in full each month is highly recommended. |

| Cash Advance APR | Often 29.9% – 35.9% (variable) | Cash advances usually come with a higher APR and often a separate fee. |

| Cash Advance Fee | $5 or 5% of transaction (whichever is greater, max $100) | An additional fee charged for each cash advance. |

| Late Payment Fee | Up to $41 | Charged if a payment is not made by the due date. Can further damage credit. |

| Foreign Transaction Fee | 1% of each transaction in U.S. dollars | A small fee applied to purchases made outside the U.S. |

The varying annual fee is determined by your creditworthiness at the time of application. While some individuals might qualify for a $0 annual fee, others may face a higher fee, particularly in the first year. It is crucial to read the terms and conditions carefully before submitting your application to understand the specific fee structure that applies to you. The high APR for purchases emphasizes the importance of paying off your balance in full each month to avoid accumulating significant interest charges.

Maximizing Your Indigo Card for Credit Improvement

The Indigo Credit Card can be an effective tool for credit building, but its success largely depends on how responsibly it is managed. Adopting smart financial habits is key to leveraging the card’s potential for improving your credit score.

Responsible Usage Practices

To maximize the benefits of your Indigo card, treating it much like a debit card is a recommended strategy. This means making small, manageable purchases that you can afford to pay off completely and on time each month.

- Make On-Time Payments: This is arguably the most critical factor in building a positive credit history. Payment history accounts for a significant portion of your credit score. Setting up automatic payments or reminders can help ensure you never miss a due date.

- Keep Credit Utilization Low: Credit utilization refers to the amount of credit you’re using compared to your total available credit. Lenders typically recommend keeping this ratio below 30%. With an initial credit limit that may be modest (often around $300-$700), it’s easy to reach a high utilization quickly. Aim to pay off your balance in full or keep it significantly lower than your limit.

- Avoid Cash Advances: As noted, cash advances come with high fees and interest rates. They should generally be avoided unless absolutely necessary, as they can quickly become a costly way to access funds and negatively impact your credit.

- Understand Your Cardholder Agreement: Familiarize yourself with all the terms, conditions, fees, and interest rates outlined in your cardholder agreement. This knowledge empowers you to avoid unexpected charges and manage your account effectively.

For detailed information on the factors that influence your credit score and how to improve it, resources like those from the Federal Trade Commission’s Consumer.gov can provide valuable insights into responsible credit management.

Monitoring Your Credit

Regularly monitoring your credit report and score is an essential part of the credit-building process. Since the Indigo card reports to all three major credit bureaus, you’ll want to track how your responsible usage is impacting your credit profile. You can obtain free copies of your credit report from each of the three major bureaus annually through AnnualCreditReport.com. Reviewing these reports helps you:

- Track Progress: See how your payment history and credit utilization are affecting your score over time.

- Identify Errors: Dispute any inaccuracies or fraudulent activity that might appear on your report.

- Understand Your Score: Recognize what factors are helping or hindering your credit growth. A fair credit score, for example, is typically between 580 and 669 on the FICO scale. Improving your score into the “good” range (670-739) can unlock better financial opportunities.

Through consistent monitoring and diligent payment habits, the Indigo Credit Card can serve as an effective instrument for improving your credit health. Keeping your credit usage in check and making prompt payments are key elements to success. You can explore more about credit monitoring and its importance in maintaining a healthy financial profile at this internal resource.

Comparing Indigo with Other Credit-Building Options

While the Indigo Credit Card is a viable option for those with less-than-perfect credit, it’s beneficial to understand how it compares to other credit-building products available in the market. This comparison can help you determine if Indigo is the best fit for your specific financial situation and goals.

- Secured Credit Cards: These cards require a security deposit, which typically acts as your credit limit. They are often easier to obtain for individuals with poor or no credit, as the deposit minimizes the risk for the issuer. Examples include the Capital One Platinum Secured Credit Card or the Discover it Secured Credit Card. Many secured cards offer a path to graduate to an unsecured card and some even offer rewards or no annual fees. The main drawback is the need for an upfront deposit, which the Indigo card avoids.

- Credit-Builder Loans: Offered primarily by credit unions and community banks, these loans are designed to help you save money and build credit simultaneously. You make regular payments into a locked savings account, and once the loan is paid off, you receive the funds. This demonstrates responsible payment behavior. This is a good option if you don’t immediately need access to credit.

- Authorized User Status: Becoming an authorized user on a trusted family member’s credit card can allow you to benefit from their good credit history, provided the issuer reports authorized user activity to credit bureaus. It’s crucial that the primary account holder maintains responsible habits, as their actions will also reflect on your credit report.

- Store Credit Cards: These cards, offered by retailers, can sometimes be easier to qualify for than general-purpose credit cards, especially for those with limited credit. However, they often come with high interest rates and are restricted to purchases within that specific store.

The Indigo Mastercard’s key differentiator is its unsecured nature for credit-challenged individuals, eliminating the need for a security deposit. However, this often comes at the cost of higher fees and a high APR compared to some secured alternatives. For instance, some secured cards have no annual fee and may even offer cash back. Ultimately, the best choice depends on your ability to make a security deposit, your tolerance for fees, and your discipline in managing credit responsibly. If you can manage a security deposit, a secured card might offer a more cost-effective path to credit improvement. If an upfront deposit is a barrier, the Indigo card remains a viable unsecured option, provided you are diligent about avoiding interest and late fees.

Conclusion

The Indigo Credit Card serves a vital role in the credit landscape, offering an unsecured option for individuals who are striving to build or rebuild their credit history. Its accessibility, reporting to all three major credit bureaus, and the convenience of a Mastercard make it a practical tool for many. However, potential cardholders must be acutely aware of its higher fees and interest rates. By leveraging the pre-qualification process, understanding eligibility requirements, and committing to disciplined financial practices—such as making on-time payments and maintaining low credit utilization—the Indigo Mastercard can be an effective stepping stone. While other credit-building alternatives exist, the Indigo card provides a no-security-deposit route to establishing a positive credit footprint. For those seeking to demonstrate financial responsibility and progressively improve their credit score, the Indigo Credit Card, when managed judiciously, offers a clear path forward towards greater financial stability and opportunity.