7 Powerful Union Bank Credit Card Features – Rewards & Benefits Guide

Table of Contents

Union Bank credit cards offer a comprehensive suite of financial products designed to cater to a broad spectrum of customer needs, from everyday spending to premium travel experiences. These cards are engineered to provide convenience, security, and a host of benefits that enhance the cardholder’s financial lifestyle. With a focus on digital innovation and customer-centric services, Union Bank aims to make credit card ownership a rewarding and seamless experience. Whether one is seeking cashback on daily purchases, accumulating travel miles, or desiring exclusive lifestyle perks, Union Bank typically provides a card variant tailored to those specific aspirations. The robust infrastructure supporting these cards ensures global acceptance and peace of mind for users, making them a significant tool in modern personal finance management.

Introduction: Understanding Union Bank Credit Cards

Union Bank, a prominent name in the financial sector across various regions, including India, the Philippines, and the United States (MUFG Union Bank), offers a diverse portfolio of credit cards. These cards are much more than mere payment instruments; they are gateways to a world of features and benefits meticulously crafted to suit different spending habits and financial goals. From competitive interest rates to robust security protocols, and from attractive reward programs to exclusive privileges, Union Bank credit cards are designed to provide substantial value to their users. The objective of this comprehensive article is to delve into the intricate details of these offerings, providing potential and existing cardholders with a clear understanding of what makes Union Bank credit cards a compelling choice in today’s competitive market.

The landscape of credit cards is constantly evolving, with banks striving to introduce innovative features that stand out. Union Bank has been at the forefront of this evolution, integrating advanced technology and customer feedback to refine its credit card products. This proactive approach ensures that cardholders receive up-to-date benefits and a secure transactional environment. The bank’s commitment to digital transformation means that many services, from application to statement viewing and reward redemption, are accessible through intuitive online platforms and mobile applications, providing unparalleled convenience.

Diverse Range of Credit Cards and Their Core Features

Union Bank’s credit card portfolio is characterized by its diversity, with offerings designed to match various consumer segments. Each card typically comes with a set of core features that form the foundation of its utility and appeal. Understanding these variants is crucial for choosing the card that best aligns with individual financial behavior and preferences.

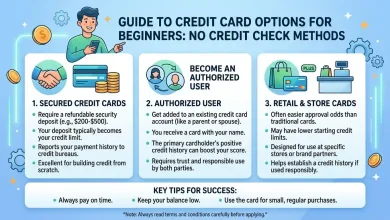

- Entry-Level and Secured Cards: For individuals new to credit or looking to rebuild their credit score, Union Bank often provides secured credit cards. These cards are typically issued against a fixed deposit, offering a secure way to establish a credit history while enjoying basic credit card functionalities. For instance, Union Bank of India offers the Usecure Credit Card, which is lifetime free and secured against a fixed deposit, providing a safe entry into the credit ecosystem. Union Bank & Trust also offers a Secured Visa card for building or repairing credit.

- Reward-Centric Cards: A significant portion of Union Bank’s offerings is dedicated to reward programs. These cards typically allow cardholders to earn points, cashback, or miles on every purchase, which can then be redeemed for various benefits. Examples include the Union Bank Travel Rewards Visa Credit Card, Union Bank Preferred Rewards Visa Credit Card (MUFG Union Bank), Union Bank Rewards Credit Card (Philippines), and Union Bank of India’s RuPay Select or VISA Signature cards. These cards often feature accelerated earning rates on specific categories like travel, dining, groceries, or digital wallet transactions.

- Lifestyle and Co-Branded Cards: Union Bank also features cards tailored to specific lifestyle needs or through partnerships with other brands. For example, Union Bank of India offers the Union UNI-CARBON Credit Card in partnership with HPCL for fuel savings and the Union JCB Wellness Credit Card for health and lifestyle benefits. UnionBank of the Philippines has cards like the UnionBank Go Rewards Gold for shopping at Robinsons Retail brands and the UnionBank Lazada Credit Card for online shopping benefits. These cards often provide enhanced benefits relevant to their co-branding or target lifestyle, such as rebates on supermarket purchases or utility bill payments.

- Premium and Travel Cards: For high-net-worth individuals and frequent travelers, Union Bank offers premium cards with enhanced benefits such as complimentary airport lounge access, comprehensive travel insurance, and dedicated concierge services. The Union Bank Travel Rewards Visa Credit Card (MUFG Union Bank), UnionBank Miles+ World Mastercard and Visa Signature (Philippines), and Union Bank of India’s Unicorn RuPay Credit Card fall into this category, providing perks like non-expiring miles, higher travel insurance, and VIP lounge access.

Across all variants, common core features typically include worldwide acceptance on major networks like Visa, Mastercard, and RuPay, EMV chip and PIN technology for enhanced security, and the provision for supplementary cards for family members. Many cards also offer an interest-free credit period on purchases, typically ranging from 21 to 50 days, provided the full balance is paid by the due date.

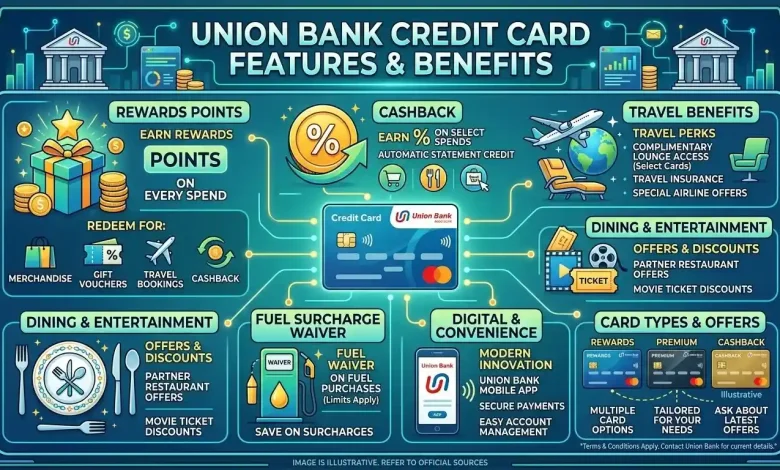

Lucrative Reward Programs: Points, Cashback, and Miles

One of the most attractive aspects of Union Bank credit cards is their diverse and often generous reward programs. These programs are designed to reward cardholders for their spending, offering tangible value back on purchases. The primary types of rewards include points, cashback, and travel miles, each with its own redemption mechanisms and benefits.

- Points-Based Rewards: Many Union Bank credit cards operate on a points system. Cardholders earn a certain number of points for every unit of currency spent (e.g., 1 point for every $1 spent, or 4 points for every ₹100 spent). These points often accumulate faster in specific spending categories, such as dining, travel, or digital wallet transactions. The redemption options for points are typically broad, including merchandise, gift cards, cash credits, or travel bookings. Some Union Banks offer unique redemption bonuses, like a 25% bonus when redeeming points into a Union Bank checking or savings account, or a 50% bonus as a principal reduction payment to a Union Bank mortgage, which can significantly enhance the value of earned points. Points validity can vary; some points may not expire, while others have a validity period, such as three years (MUFG Union Bank) or 24 months (Union Bank of Colombo).

- Cashback Programs: For cardholders who prefer straightforward savings, Union Bank offers cashback credit cards. These cards provide a percentage of spending back as cash. For example, the UnionBank Cash Back Visa Platinum (Philippines) offers up to 6% rebates on supermarket purchases and 2% on Meralco bill payments, with 0.20% on all other purchases. MUFG Union Bank also offers cash-back rewards that do not expire as long as the account remains open and in good standing. Cashback programs are particularly appealing to those who want direct savings on their everyday expenses without managing a points system.

- Travel Miles: Frequent travelers benefit immensely from Union Bank credit cards that offer travel miles. Cards like the UnionBank Miles+ World Mastercard and Visa Signature allow cardholders to earn miles for every peso spent, which can then be converted into airline miles or used as cash credits to offset travel-related purchases. A significant advantage of some of these travel cards is that the miles earned may not expire, providing cardholders with ample time to accumulate enough for significant travel redemptions. This makes them ideal for individuals who plan their trips well in advance or accumulate miles over longer periods.

It’s important to note that reward programs often come with specific terms and conditions, such as spending caps on bonus categories, exclusions for certain transaction types (e.g., cash advances, balance transfers, fees), and requirements for account standing for redemption. Cardholders are usually notified of their reward points activity through monthly statements or dedicated online portals.

| Credit Card Type/Feature | Description & Typical Benefits | Example (Union Bank of…) |

|---|---|---|

| Rewards/Points Cards | Earn points on purchases, often accelerated in specific categories (dining, travel, groceries). Points redeemable for merchandise, gift cards, cash credits, or travel. | MUFG Union Bank Travel Rewards Visa Credit Card (3x points on travel) Union Bank of India RuPay Select (up to 4 reward points per ₹100) |

| Cashback Cards | Receive a percentage of spending back as cash or rebates. Direct savings on everyday expenses. | UnionBank Cash Back Visa Platinum (up to 6% on supermarkets, 2% on Meralco bills) MUFG Union Bank Bank Freely Rewards Visa (unlimited 1.5% cashback) |

| Travel/Miles Cards | Accumulate travel miles on spending, often with non-expiring miles. Benefits include lounge access, travel insurance. | UnionBank Miles+ World Mastercard/Visa Signature (1 mile per ₱30 spend, lounge access, travel insurance) Union Bank of India Unicorn RuPay (International Lounge Access, travel discounts) |

| Secured Credit Cards | Issued against a fixed deposit, ideal for building or rebuilding credit. Offers basic credit card functions with high security. | Union Bank of India Usecure Credit Card (Lifetime Free, EMV chip) Union Bank & Trust Secured Visa |

| Co-Branded/Lifestyle Cards | Partnerships offering specialized benefits in specific sectors like fuel, retail, or health. | Union Bank of India UNI-CARBON Credit Card (fuel savings with HPCL) UnionBank Go Rewards Gold (Go Rewards points with Robinsons Retail) |

| Premium Cards | Exclusive benefits for affluent clients including enhanced lounge access, concierge services, and higher insurance coverage. | UnionBank Reserve Card (5x points on global shopping/dining, Priority Pass, VIP Global Concierge) Union Bank of India NEXTERIA (Metal card, exclusive lounge access) |

Exclusive Travel and Lifestyle Privileges

Beyond transactional benefits, Union Bank credit cards often come bundled with a range of exclusive travel and lifestyle privileges that significantly enhance the cardholder experience. These perks are particularly valuable for frequent travelers and those who appreciate premium services.

- Airport Lounge Access: A highly sought-after benefit, many premium Union Bank credit cards offer complimentary access to domestic and international airport lounges. For instance, Union Bank of India’s RuPay Select Credit Card can offer up to 4 complimentary airport lounge visits per year at over 300 partner lounges worldwide. The UnionBank Miles+ Visa Signature (Philippines) provides free DragonPass membership with two complimentary lounge passes per membership year. Such access allows travelers to relax in comfort, enjoy refreshments, and utilize business facilities before their flights. Cards like the Union Bank of India Unicorn RuPay and NEXTERIA also boast comprehensive lounge access benefits, including Priority Pass access for international lounges.

- Travel Insurance and Assistance: Travel-oriented Union Bank credit cards often include complimentary travel insurance coverage, which can range from accidental insurance to more comprehensive plans covering flight delays, lost luggage, and medical emergencies. The UnionBank Miles+ World Mastercard and Visa Signature, for instance, provide up to ₱1 million in travel insurance if tickets are charged to the card. Some Union Bank of India cards also offer personal accident insurance coverage. Additionally, cards may provide roadside dispatch services and access to Visa Global Customer Care Services for emergencies while traveling.

- Concierge Services: High-tier Union Bank credit cards may grant access to dedicated concierge services. These services can assist with a wide array of tasks, including booking flights and hotels, arranging car rentals, securing event tickets, and making dining reservations. This personalized support can be invaluable for busy individuals seeking convenience and efficiency.

- Dining and Shopping Discounts: Cardholders can frequently enjoy exclusive discounts and offers at partner restaurants, retail outlets, and e-commerce platforms. These can range from percentage-based discounts to special bundles or cashback offers on specific purchases. For example, some UnionBank of the Philippines cards offer rebates on supermarket purchases. Union Bank of India’s Unicorn RuPay card includes benefits like Swiggy One Membership, Myntra, Big Basket, and Nykaa vouchers, as well as Book My Show movie ticket discounts.

- Exclusive Experiences: Certain premium cards might offer unique experiences such as complimentary golf games, spa services, or health check-ups, as seen with Union Bank of India’s JCB Wellness and Health Credit Cards. These benefits cater to a luxury lifestyle, providing cardholders with access to exclusive leisure and wellness opportunities.

Robust Security and Financial Flexibility

Security and financial flexibility are paramount features of Union Bank credit cards, designed to provide cardholders with peace of mind and greater control over their finances.

Advanced Security Features

Union Bank places a strong emphasis on protecting its cardholders from fraud and unauthorized transactions. Key security features commonly include:

- EMV Chip and PIN Technology: All Union Bank cards are equipped with embedded EMV chip technology, providing an extra layer of security for transactions at chip-enabled POS terminals and ATMs. This technology securely stores account information, making it difficult to counterfeit cards. Some banks, like UnionBank of the Philippines, have even disallowed “fallback” transactions to magnetic stripes for enhanced protection.

- One-Time Passwords (OTPs) and 3FA Authentication: For online transactions, a One-Time Password (OTP) is sent to the cardholder’s registered mobile number for validation. This multi-factor authentication (often 3FA for domestic online transactions in India) adds a crucial layer of security, ensuring that only the legitimate cardholder can complete online purchases.

- Zero Fraud Liability: In the unfortunate event of unauthorized transactions, many Union Bank credit cards offer zero fraud liability. This means cardholders are protected from financial loss due to fraudulent activity, provided they report the loss or theft of their card promptly.

- Transaction Alerts and Card Controls: Union Bank often provides SMS alerts for all transactions, billing amounts, and other account activities. Furthermore, digital banking platforms and dedicated apps allow cardholders to actively manage their card security. Features like temporarily locking/unlocking cards, setting real-time transaction alerts, viewing transaction history, and placing location controls on purchases are increasingly common, giving users direct control over their card’s usage.

- Secure Online Shopping: Union Bank offers features like ShopSafe, which adds an extra level of protection for internet shopping by requiring an OTP for transactions at participating online stores.

Financial Flexibility Options

Union Bank credit cards also offer various features that enhance financial flexibility, allowing cardholders to manage their spending and repayments effectively:

- Interest-Free Credit Period: Most cards provide an interest-free credit period on fresh purchases, typically ranging from 20 to 50 days, giving cardholders time to pay their outstanding balance without incurring interest charges, provided the full amount is paid by the due date.

- Flexible Monthly Payments and Installment Plans: Cardholders have the option to pay a minimum amount due (e.g., 5% of the bill amount or a fixed minimum), allowing them to manage their cash flow. Furthermore, Union Bank credit cards often offer in-house installment plans, enabling cardholders to convert large purchases or billed statement balances into fixed monthly installments. This also extends to balance transfers from non-Union Bank credit cards.

- Cash Advance Facility: In times of urgent need, cardholders can avail of a cash advance facility, withdrawing cash from their credit limit at ATMs, typically up to a certain percentage of their credit limit (e.g., 20% to 40%). However, cash advances usually incur fees and do not benefit from an interest-free period.

- Bill Payment Facilities: Many Union Bank cards offer convenience features like auto-charge for utility bills, allowing cardholders to manage all their recurring payments through a single due date, streamlining financial management.

The Application Process and Eligibility

Applying for a Union Bank credit card is typically a straightforward process, often facilitated by online applications. However, eligibility criteria and required documentation can vary depending on the specific Union Bank entity and the type of credit card being applied for.

General Eligibility Criteria

While specific requirements differ, common eligibility criteria often include:

- Age: Applicants must typically be at least 18 or 21 years old. Supplementary cardholders can be as young as 14 years old with the principal cardholder’s consent.

- Income: A stable source of income is usually a prerequisite. Union Bank of India, for example, often requires a minimum annual proven income for unsecured cards, which can be around ₹4.80 lakhs. For secured cards, income proof might not be strictly required as the card is issued against a fixed deposit.

- Credit History: For unsecured credit cards, a good credit history and score are generally essential for approval. For those with no credit or damaged credit, secured credit cards are available as an alternative to help build or repair credit.

- Residency: Applicants must be residents of the country where the Union Bank operates.

Required Documents

The documentation needed for a credit card application typically includes:

- Proof of Identity: Government-issued IDs such as a national ID card, passport, or driver’s license.

- Proof of Address: Utility bills, bank statements, or rental agreements.

- Proof of Income: Salary slips, income tax returns, bank statements showing salary credits, or employment certificates. For self-employed individuals, business financial statements may be required.

The application process itself is often facilitated through online portals, allowing applicants to submit their details and documents digitally. Banks usually aim for a quick turnaround time for application processing, especially for digital-first institutions like UnionBank of the Philippines. Upon approval, a virtual card might be immediately available for online shopping even before the physical card arrives.

Maximizing Your Union Bank Credit Card Benefits

To truly unlock the full potential of a Union Bank credit card, cardholders should adopt strategic usage habits and actively engage with the features offered. Here are some tips to maximize the benefits:

- Understand Your Card’s Reward Structure: Each card has a unique reward system. Familiarize yourself with which categories offer accelerated points, cashback, or miles. Use the card primarily for these categories to maximize earnings.

- Pay Bills on Time and In Full: To avoid interest charges and late fees, always pay your outstanding balance by the due date. This ensures you benefit from the interest-free credit period and maintains a good credit score.

- Leverage Redemption Bonuses: If your Union Bank offers bonuses for redeeming points into checking/savings accounts or towards mortgage principal, take advantage of these for higher value. Compare redemption values across different options (e.g., travel vs. merchandise vs. cash back) to get the most out of your points.

- Utilize Travel Perks: If your card offers complimentary lounge access, travel insurance, or concierge services, make sure to use them when traveling. These can save significant costs and enhance your travel experience.

- Monitor Offers and Promotions: Keep an eye on exclusive discounts, cashback offers, and promotions that Union Bank regularly rolls out for its cardholders. These can be seasonal or tied to specific merchants.

- Use Security Features: Activate SMS alerts for all transactions and utilize online card controls to monitor and protect your account from fraud. Report any suspicious activity immediately.

- Consider Supplementary Cards: For family members, supplementary cards can help accumulate rewards faster while allowing controlled spending under the principal account.

- Maintain a Good Credit Utilization Ratio: Keep your credit utilization low (ideally below 30%) to positively impact your credit score, which can lead to higher credit limits and better offers in the future. A good credit score is also beneficial for various financial endeavors, as explained by Wikipedia’s article on credit scores.

Conclusion

Union Bank credit cards stand out in the financial market for their comprehensive range of features and benefits, catering to a diverse clientele. From robust security measures like EMV chip technology and OTP authentication to a variety of reward programs encompassing points, cashback, and travel miles, these cards are designed to add tangible value to a cardholder’s financial life. The inclusion of lifestyle privileges such as airport lounge access, extensive travel insurance, and dedicated concierge services further enhances their appeal, particularly for those seeking premium experiences. With user-friendly application processes and a strong emphasis on digital convenience, Union Bank ensures that managing credit card accounts is as seamless as possible. By understanding the specific features of each card variant and strategically utilizing the myriad of benefits offered, cardholders can significantly maximize their financial advantage and elevate their overall banking experience with Union Bank.