7 Best Credit Cards to Maximize Your Everyday Savings

Table of Contents

Credit card cashback offers provide a compelling incentive for consumers to get more value from their everyday spending. In an increasingly competitive financial landscape, these programs allow cardholders to earn a percentage of their eligible purchases back as rewards, effectively reducing the cost of goods and services. Typically ranging from 1% to 5%, these cashback rewards can accumulate significantly over time, turning routine transactions into tangible savings. Understanding how to strategically utilize these offers is key to maximizing your financial benefits and ensuring that your credit card works for you, rather than against you.

Introduction to Cashback Credit Cards

Cashback credit cards are a popular type of rewards card that returns a portion of the money spent on purchases to the cardholder. This returned amount is known as “cashback” and can be redeemed in various forms, such as statement credits, direct deposits into a bank account, or gift cards. The fundamental appeal of cashback lies in its simplicity and flexibility: unlike airline miles or hotel points that might require specific redemption strategies, cashback offers straightforward value that can be used however the cardholder chooses.

The concept is simple: you spend, and the card issuer gives you a percentage back. This mechanism encourages responsible credit card use, where individuals can benefit from their spending habits without incurring debt, provided they pay their balance in full each month. The rise of digital transactions and remote banking has further fueled the growth and appeal of cashback programs, making them a central feature in many credit card marketing efforts.

Understanding Different Cashback Models

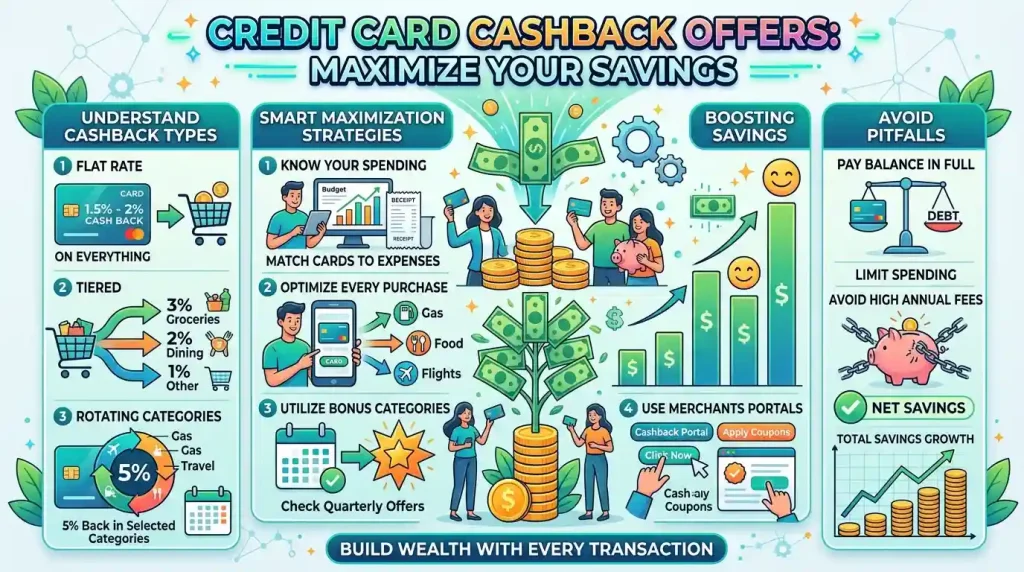

To truly maximize savings, it’s crucial to understand the various models cashback credit cards employ. These models dictate how and where you earn your rewards, and aligning them with your spending patterns is paramount. There are three primary structures for cashback programs: flat-rate, tiered, and rotating categories.

- Flat-Rate Cashback Cards: These cards offer a consistent percentage of cashback on all eligible purchases, regardless of the spending category. They are ideal for individuals who prefer simplicity and do not want to track changing categories or juggle multiple cards. A common flat rate is 1.5% to 2% on all purchases, making them a solid choice for everyday spending not covered by bonus categories on other cards. For instance, the Citi Double Cash Card offers 2% cash back (1% when you buy, 1% when you pay).

- Tiered Cashback Cards: With tiered cards, you earn different reward rates based on specific spending categories. For example, a card might offer 3% cashback on dining, 2% on groceries, and 1% on all other purchases. These cards reward spending in specific areas where consumers typically spend a lot, allowing for higher earning potential if your expenses align with the bonus categories.

- Rotating Category Cashback Cards: These cards offer the highest cashback rates, often 5%, in specific categories that change quarterly. Common rotating categories include gas stations, grocery stores, dining, and online shopping. A key aspect of these cards is that you usually need to activate the bonus categories each quarter to earn the elevated rewards. While they require more attention and management, they can yield significant rewards for disciplined users. Examples include Chase Freedom Flex and Discover it Cash Back.

Key Factors to Consider When Choosing a Cashback Card

Selecting the right cashback credit card, or combination of cards, depends heavily on your individual spending habits and financial goals. Several factors should influence your decision to ensure you’re truly maximizing your savings.

- Spending Habits: Analyze your monthly expenses to identify where you spend the most. If a significant portion of your budget goes towards groceries and gas, a card offering high cashback in those categories would be more beneficial than a general flat-rate card. Conversely, if your spending is highly varied, a flat-rate card might be more straightforward and offer better overall value.

- Annual Fees: Some premium cashback cards may charge an annual fee. It’s essential to calculate whether the cashback you expect to earn will outweigh the cost of the fee. If a card charges a $95 annual fee, but you anticipate earning $300 in rewards, it could be a worthwhile investment. However, many excellent cashback cards come with no annual fee, making them a great starting point.

- Sign-Up Bonuses: Many credit card issuers offer lucrative sign-up bonuses for new cardholders, often awarded after meeting a minimum spending requirement within a specified timeframe. These bonuses can provide a substantial initial boost to your cashback earnings, sometimes equivalent to hundreds of dollars. Leveraging these offers strategically can significantly accelerate your savings.

- Redemption Options: While cashback is generally straightforward, redemption options can vary. Common methods include statement credits, direct deposits to a bank account, or gift cards. Some cards might offer better value for certain redemption types, or have minimum redemption thresholds (e.g., $25 in rewards). Evaluate which options are most convenient and valuable for you.

- APR and Interest Rates: A critical consideration, especially if you anticipate carrying a balance, is the Annual Percentage Rate (APR). Cashback rewards can be quickly negated by high interest charges. The golden rule for rewards cards is to pay your balance in full every month to avoid interest payments, which would otherwise diminish or even eliminate your cashback benefits.

Strategies for Maximizing Your Cashback Rewards

Once you’ve chosen the right cards, implementing smart strategies will help you get the most out of every purchase. Maximizing cashback is an ongoing effort that involves organization and mindful spending.

One of the most effective strategies is to combine different types of cashback cards. This often involves pairing a flat-rate card for everyday purchases with one or more bonus category cards for specific high-spending areas. For example, you might use a card that offers 5% back on groceries for your supermarket runs, and a 2% flat-rate card for all other expenses. This multi-card approach ensures that you’re always earning the highest possible rate for each transaction.

Another key strategy is to diligently track rotating bonus categories and activate them promptly. Many issuers notify cardholders of upcoming categories, and setting calendar reminders can help you stay on top of these changes. Adjusting your spending to align with these categories can significantly boost your quarterly earnings.

Leveraging sign-up bonuses is also a powerful way to maximize initial savings. When opening a new card, plan your spending to meet the required threshold for the bonus without overspending on unnecessary items. This immediate influx of cashback can be a substantial benefit.

Beyond credit cards, consider incorporating cashback apps and shopping portals. Many banks and airlines offer online shopping portals that provide extra cashback or points when you shop through their links. These can be stacked with your credit card rewards for even greater savings.

| Cashback Model | Description | Typical Cashback Rate | Ideal User | Example Category (if applicable) |

|---|---|---|---|---|

| Flat-Rate | Earns the same percentage back on all eligible purchases. | 1.5% – 2% | Prefers simplicity, varied spending. | N/A (all purchases) |

| Tiered Rewards | Offers different reward rates based on spending categories. | 2% – 3% (select categories), 1% (others) | Consistent high spending in specific areas. | Groceries, Dining, Gas |

| Rotating Categories | Highest rates in categories that change quarterly; requires activation. | 5% (bonus categories), 1% (others) | Willing to manage categories, higher earning potential. | Quarterly: Gas, Groceries, Online Shopping |

Common Cashback Categories and How to Leverage Them

Cashback programs often focus on specific spending categories that are common for most consumers. Knowing these categories and having the right card for each can significantly enhance your rewards.

- Groceries: Supermarket spending is a major household expense, and many cards offer elevated cashback for grocery purchases. Some cards might offer 3-6% cashback on groceries, making them incredibly valuable for families. Be aware that some cards exclude superstores like Walmart or Target from their grocery bonus categories.

- Gas Stations: With fluctuating fuel prices, earning cashback on gas can provide substantial savings. Several cards offer 3-5% back on gas purchases. Some programs have even seen a doubling of issuers offering gas rewards from 2023 to 2024.

- Dining and Entertainment: For those who frequently eat out or enjoy entertainment, cards offering bonus cashback on restaurant, dining, and even streaming services are highly beneficial. Rates can range from 3% to 5% in these categories.

- Online Shopping: As e-commerce continues to grow, many cards now provide enhanced cashback for online purchases. This can sometimes be a rotating category or a fixed bonus for specific online retailers.

- Travel: While travel cards often offer points or miles, some cashback cards also provide elevated rewards for travel bookings, especially when booked through the card issuer’s portal.

- Drugstores: Several cards also offer bonus cashback on drugstore purchases, which can be useful for health and personal care expenses.

- Utilities and Streaming Services: Some unique cashback categories now include home utilities, internet, cable, phone services, and streaming subscriptions, reflecting modern spending habits.

To effectively leverage these categories, it is recommended to review your monthly statements to identify your top spending areas and then select credit cards that align with those categories. For instance, if you spend heavily on both groceries and dining, you might use one card for groceries and another for dining to maximize rewards across both.

Potential Pitfalls and How to Avoid Them

While cashback offers present a fantastic opportunity for savings, there are several pitfalls that, if not managed carefully, can negate any earned rewards.

- Carrying a Balance and Paying Interest: This is arguably the biggest trap. High interest rates on cashback cards can quickly erode any rewards earned if you carry a balance from month to month. As reported by Bankrate, with average credit card APRs often exceeding 20%, earning 2% cashback while paying 20% interest means you are losing money, not saving. Always pay your statement balance in full by the due date to avoid interest charges.

- Annual Fees Outweighing Rewards: Some cards with attractive cashback rates come with an annual fee. If your annual spending and the resulting cashback don’t surpass the fee, the card isn’t providing a net benefit. Always calculate the net value (total cashback minus annual fee) to ensure profitability.

- Overspending to Earn Rewards: The temptation to spend more just to earn more cashback or hit a sign-up bonus threshold is a common mistake. Only spend on purchases you would have made anyway and within your budget. Credit card rewards should supplement, not dictate, your spending habits.

- Missing Out on Introductory Bonuses or Category Activations: Sign-up bonuses often have specific spending requirements and time limits. Forgetting to meet these can mean missing out on significant rewards. Similarly, for rotating category cards, failing to activate the bonus categories each quarter will result in earning only the base cashback rate. Setting reminders can help prevent these oversights.

- Complex Redemption Processes and Expiring Rewards: While cashback is generally straightforward, some programs might have minimum redemption amounts, or rewards could expire if not redeemed within a certain timeframe or if the account is inactive. Always be aware of your card’s redemption policies and aim to redeem rewards regularly. Statement credits or direct deposits are often the most efficient redemption methods.

To avoid these pitfalls, financial literacy and disciplined credit card management are essential. Regular monitoring of statements, setting up automatic payments, and understanding the terms and conditions of each card are crucial steps. For more information on responsible credit card usage and consumer protection, you can refer to resources like the Consumer Financial Protection Bureau (CFPB).

Advanced Tactics for the Savvy Spender

For those who are highly organized and committed to optimizing their cashback earnings, several advanced tactics can push savings even further.

- Credit Card Stacking: This involves combining multiple cards, each optimized for different spending categories, to achieve the highest possible cashback rate across all your purchases. For example, you might use a card with 5% on groceries, another with 3% on dining, and a flat 2% card for everything else. This strategy requires diligent tracking and ensures no spending opportunity is missed.

- Using Shopping Portals and Apps: Beyond credit card rewards, many online shopping portals and apps offer additional cashback for purchases made through their platforms. These can often be stacked with your credit card rewards. Always check if a shopping portal offers a bonus before making a significant online purchase.

- Leveraging Loyalty Programs: Some credit cards integrate with specific merchant loyalty programs, allowing for even greater savings. This creates a symbiotic relationship where cardholders can earn rewards from both the credit card and the retailer.

- Understanding Merchant Category Codes (MCCs): Credit card issuers categorize merchants using MCCs. Sometimes, a purchase that seems like one category (e.g., a supermarket purchase at a large retailer) might code differently, affecting your cashback rate. Understanding how merchants are coded can help you choose the right card for maximum rewards.

- Taking Advantage of Annual Credits and Perks: Some premium cashback cards, despite their annual fees, offer valuable annual credits (e.g., for travel, dining, or streaming services) or perks like cell phone protection and extended warranties that can offset the fee and enhance overall value.

These advanced strategies require a higher level of commitment and organization but can significantly increase your overall cashback earnings. It’s crucial to always stay informed about your card’s terms and conditions, as well as any changes to reward structures.

Conclusion

Credit card cashback offers are a powerful tool for maximizing your savings, transforming everyday expenses into tangible financial benefits. By understanding the different cashback models—flat-rate, tiered, and rotating categories—and aligning them with your personal spending habits, you can strategically choose cards that provide the most value. Key considerations such as annual fees, sign-up bonuses, and redemption options play a vital role in this selection process.

The most crucial aspect of any cashback strategy is responsible credit card management. Always paying your balance in full each month is paramount to avoid interest charges that would otherwise negate your earned rewards. Avoiding overspending, diligently tracking bonus categories, and redeeming rewards efficiently are also essential practices. For the savvy spender, combining multiple cards, leveraging shopping portals, and understanding unique category codes can further amplify savings. Ultimately, by approaching credit card cashback offers with a well-thought-out strategy and financial discipline, you can unlock significant savings and make your money work harder for you.