7 Best Credit Cards for No Credit History – Easy Approval Guide

Table of Contents

Credit cards for no credit history with easy approval are a critical starting point for millions of individuals looking to establish a financial footprint. Entering the financial world without a credit history can often feel like a Catch-22: you need credit to get credit. This dilemma leaves many feeling frustrated, especially when faced with applications that require an established credit score. However, the landscape of personal finance has evolved, and numerous options now exist for those with a blank credit file. This comprehensive guide will explore the avenues available, helping you understand how to secure a credit card, build a strong credit profile, and ultimately unlock greater financial opportunities. We’ll delve into various card types, approval strategies, and best practices to ensure your journey from no credit to good credit is as smooth and successful as possible.

Understanding “No Credit History”

Having “no credit history” is distinctly different from having “bad credit.” Bad credit implies a history of missed payments, defaults, or bankruptcies that negatively impact your credit score. No credit history, on the other hand, means you simply haven’t used credit products like loans or credit cards before, or your credit activity has been minimal and recent, making it difficult for lenders to assess your risk. This scenario is common for young adults, recent immigrants, or anyone who has historically used cash or debit for all transactions. Lenders rely on credit reports to determine your creditworthiness, and without sufficient data, they cannot accurately predict your ability to repay debt. This lack of information is often perceived as a risk, leading to rejections for conventional credit products. The challenge then becomes demonstrating responsibility without a track record. Understanding this distinction is the first step toward choosing the right financial products to begin building your credit profile effectively. Your journey to a robust financial standing begins with acknowledging your current position and strategically selecting tools designed for your specific situation. Many financial institutions now offer pathways specifically designed for individuals in this exact predicament, recognizing the demand and importance of financial inclusion. They understand that a lack of history does not equate to a lack of responsibility, and they’ve tailored products accordingly to help new users get started on their credit journey. It’s about finding those specific products and understanding their mechanisms.

Why Building Credit is Crucial

Building a solid credit history is not merely about getting a credit card; it’s a foundational element of modern financial life. A good credit score, typically ranging from 670 to 850, acts as your financial passport, influencing various aspects of your life. Firstly, it dictates your ability to secure loans for major purchases, such as a car or a home. Lenders use your credit score to determine your eligibility and the interest rates you’ll pay, with better scores leading to lower rates and substantial savings over the life of a loan. Secondly, many landlords now check credit reports when you apply to rent an apartment, viewing it as an indicator of your reliability and ability to meet financial obligations. A strong credit history can give you an edge in competitive rental markets. Thirdly, utility companies, cell phone providers, and even insurance companies may use your credit information to decide whether to require a deposit or to offer you better rates. In some cases, employers might even review credit reports for certain positions, particularly those involving financial responsibilities. Therefore, establishing and maintaining a positive credit history from an early stage is paramount for accessing favorable financial products, securing housing, and even advancing career opportunities. Without credit, you may find yourself limited to higher interest rates, requiring larger deposits, or even being denied essential services. It’s an investment in your future financial flexibility and security. Maintaining a good credit profile also offers peace of mind, knowing that you are prepared for unexpected financial needs or opportunities that may arise, further emphasizing its role as a cornerstone of personal finance.

Types of Credit Cards for Beginners

For individuals with no credit history, the good news is that the financial market offers several tailored options to help you get started. These cards are specifically designed to minimize risk for lenders while providing a pathway for consumers to establish a credit profile. Understanding the different types available is key to choosing the one that best fits your financial situation and goals. Each option has its unique benefits and considerations, and selecting wisely can set the stage for successful credit building. The common thread among these beginner-friendly cards is their focus on demonstrating responsible financial behavior, which is precisely what lenders are looking for when you lack an established history. They serve as stepping stones, allowing you to prove your reliability before moving on to more conventional, higher-limit credit products. By starting with these specialized cards, you can avoid the frustration of repeated rejections and instead focus on establishing a positive financial track record from day one. It’s about smart strategic choices in the initial phase of your credit journey.

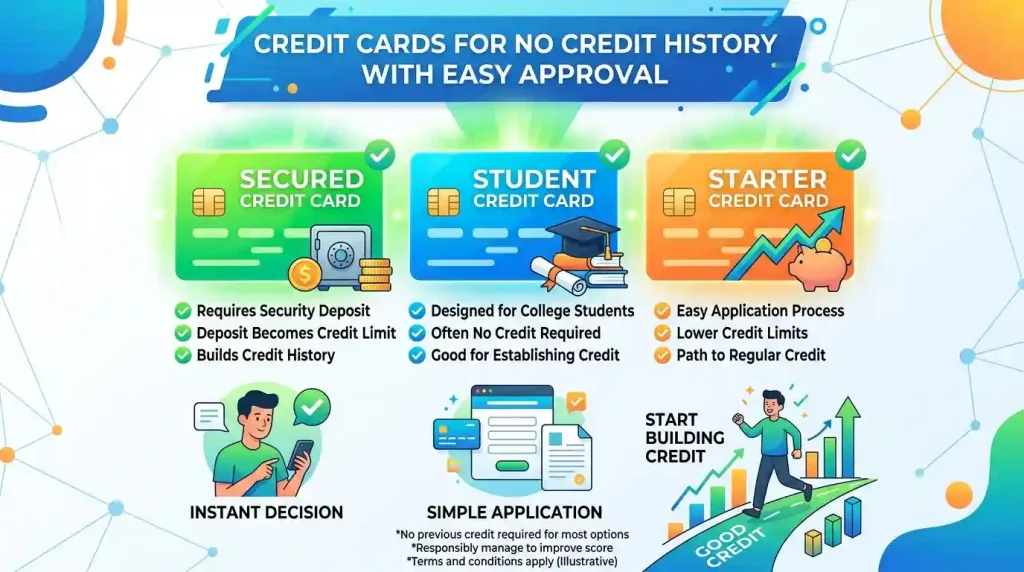

Secured Credit Cards: A Foundation for Credit Building

Secured credit cards are arguably the most common and effective tool for individuals with no credit history. They work by requiring a cash deposit, which typically becomes your credit limit. For example, if you deposit $300, your credit limit will be $300. This deposit serves as collateral, significantly reducing the risk for the issuer and making approval much easier, even for those with no credit at all. While you’re using your own money as collateral, the card functions exactly like a regular credit card. You make purchases, receive monthly statements, and are required to make payments. The crucial difference is that your payment activity is reported to the major credit bureaus (Equifax, Experian, and TransUnion). Consistent, on-time payments demonstrate responsible financial behavior, which is then recorded on your credit report, helping to build your credit score over time. After a period of responsible use, often 6 to 12 months, many secured card issuers will offer to convert your card to an unsecured card and return your deposit. This transition signifies that you’ve successfully built enough trust with the lender to qualify for credit without collateral. It’s a reliable method to demonstrate creditworthiness and often the quickest route to an unsecured card. When evaluating secured credit cards, look for those with low or no annual fees and ensure they report to all three major credit bureaus, as this maximizes the impact of your positive payment history. Some secured cards even offer interest on your deposit, though this is less common. The key benefit is not just the credit limit, but the opportunity to establish a positive payment history. For further tips on building your credit, you might find valuable insights by exploring resources on effective credit building strategies.

Student Credit Cards: Designed for the Academic Journey

Student credit cards are specifically designed for college students, recognizing that many students have little to no credit history but often have a future income potential. These cards typically come with lower credit limits and fewer perks than premium cards, but they offer an invaluable opportunity to build credit while pursuing higher education. Lenders usually require proof of enrollment and may consider factors like part-time employment income or even the ability of a co-signer (though co-signers are less common for student cards themselves, they might be for other loans). The approval criteria for student cards are generally more lenient than for standard unsecured cards, making them accessible to those who might otherwise be rejected. Like secured cards, the primary benefit of a student credit card is its ability to report your payment activity to credit bureaus, allowing you to establish a credit history before you even graduate. Responsible use—paying your balance on time and keeping your credit utilization low—is paramount. Many student cards also offer student-specific benefits, such as rewards for good grades or discounts on educational purchases. While they might not offer the highest rewards, their main purpose is to serve as a stepping stone. They are an excellent way for students to learn financial responsibility and build a credit score that will benefit them in post-graduation life, from renting an apartment to financing a car. It’s important for students to remember that these are real credit cards, and irresponsible use can lead to debt and damage their nascent credit profile. Choosing a card that helps you understand the basics of credit management, such as timely payments and responsible spending, is far more beneficial than focusing on high rewards at this early stage. Many institutions partner with universities or offer specialized programs to cater to students, making these cards quite prevalent in the market for young adults.

Becoming an Authorized User: A Simple Start

Another accessible route to building credit without directly applying for a card is becoming an authorized user on someone else’s credit card account. This strategy involves a trusted individual—a parent, spouse, or close relative—adding you to their existing credit card account. As an authorized user, you’ll receive your own card linked to their account, allowing you to make purchases. Crucially, the account’s entire credit history, including its age, credit limit, and payment history, can then appear on your credit report. If the primary account holder has a long history of on-time payments and low credit utilization, this positive activity can significantly boost your credit score. However, this method comes with a major caveat: the primary account holder’s irresponsible behavior will also reflect on your credit report. If they miss payments or carry high balances, it could negatively impact your score. Therefore, it’s vital to choose a primary account holder who is financially responsible and trustworthy. While it’s an easy way to get started, becoming an authorized user doesn’t give you full control over the account, nor does it teach you the complete discipline of managing your own credit line. It’s often best used as a temporary measure or in conjunction with other credit-building strategies. It also doesn’t always guarantee that all credit bureaus will include the authorized user’s history in the same way, so results can vary slightly. For individuals who are starting from zero, however, it can provide a quick initial boost that makes it easier to qualify for your own secured or student card down the line.

Credit-Builder Loans: An Alternative Path

While not a credit card, a credit-builder loan is an excellent tool for establishing credit history, especially if you’re struggling to get approved for even a secured card. This type of loan works in reverse: instead of receiving a lump sum upfront, the money is held in an interest-bearing savings account or certificate of deposit (CD) by the lender. You make regular monthly payments on the loan, typically over 6 to 24 months. Each on-time payment is reported to the credit bureaus. Once you’ve paid off the entire loan, the principal amount is released to you, often with the accumulated interest. This mechanism demonstrates your ability to make consistent payments, a key factor in credit scoring. The benefit is twofold: you build a positive payment history, and you create a savings fund. Credit-builder loans are designed for those with no credit or poor credit, so approval is usually very easy. Interest rates can vary, and there might be administrative fees, so it’s important to compare options. It’s a disciplined approach to building credit and savings simultaneously, offering a low-risk way to prove your financial reliability to future lenders. This can be a particularly attractive option for those who prefer a structured savings component alongside their credit-building efforts. The disciplined repayment schedule inherently encourages responsible financial habits, preparing you for managing other credit products in the future. It’s a transparent way to build credit without the immediate temptation of a credit line.

| Credit Building Product | Primary Mechanism | Pros for Beginners | Cons for Beginners | Typical Approval Ease |

|---|---|---|---|---|

| Secured Credit Card | Requires a cash deposit as collateral. | Very high approval rate; direct credit card experience; deposit often refundable. | Requires upfront deposit; typically lower credit limits. | Very Easy |

| Student Credit Card | Unsecured card for enrolled students. | No deposit needed; specific benefits for students; builds credit directly. | Requires student status; lower credit limits than standard cards. | Easy (with proof of enrollment) |

| Authorized User | Added to someone else’s existing account. | Instant credit history boost (if primary user is responsible); no direct application or fees. | Dependent on primary user’s financial habits; less direct control. | N/A (no approval process for the user) |

| Credit-Builder Loan | You make payments into a savings account, then receive the funds. | Builds payment history; forces savings; no credit check often. | Funds are locked until loan is paid off; may have fees/interest. | Very Easy |

Strategies for Easy Approval

Even with credit cards designed for no credit history, a strategic approach can significantly increase your chances of easy approval. The goal is to present yourself as a low-risk applicant, even without a lengthy financial past. Firstly, ensure you meet the basic eligibility criteria. While a credit score isn’t a factor, lenders will still look for proof of identity, age (typically 18 or older), and a valid Social Security number or Individual Taxpayer Identification Number (ITIN). Secondly, provide accurate and honest income information. While you might not have a high income, demonstrating a steady source of funds (from a job, student aid, or even allowances) can reassure lenders that you have the means to make payments. Be prepared to provide documentation if requested. Thirdly, consider applying for products known for their easy approval. Secured credit cards and credit-builder loans are almost guaranteed approval if you meet basic requirements and can provide the deposit (for secured cards). Student cards also have more lenient criteria. Fourthly, avoid applying for too many cards at once. Each application can result in a hard inquiry on your nascent credit file, which can temporarily lower your score. It’s better to apply for one or two suitable options and wait to see the outcome. Finally, if you’re denied, don’t be discouraged. Ask the lender why you were denied; they are legally required to provide this information. This feedback can help you understand what areas to improve before reapplying. Sometimes, it might be as simple as correcting an error in your application or choosing a different product. Taking these steps not only enhances your approval prospects but also lays a solid groundwork for responsible credit management. Patience and persistence are key when starting your credit journey. The better you understand the specific requirements of each product, the more effectively you can tailor your application to increase your chances of success and minimize any potential setbacks. It’s about being informed and strategic in your approach. Knowing your current financial standing, even without a credit history, is vital, and resources on how credit scores work can be immensely helpful.

Choosing the Right Card: Key Considerations

Selecting the ideal credit card when you have no credit history involves more than just getting approved; it’s about choosing a card that aligns with your financial goals and helps you build credit effectively. Several factors should guide your decision-making process. First and foremost, look at the annual fee. Many beginner-friendly cards, especially secured ones, may charge an annual fee. While some fees are acceptable if the card helps you build credit, strive for cards with low or no annual fees to minimize costs. Secondly, consider the interest rate (APR). While you should aim to pay your balance in full each month to avoid interest, a lower APR can protect you if you ever carry a balance. Look for cards with competitive rates, although for credit-building cards, APRs can sometimes be higher. Thirdly, evaluate any rewards programs. While not the primary focus for a first credit card, some secured or student cards offer modest rewards, such as cash back on certain purchases. If two cards are otherwise equal, a small rewards program can be a nice bonus. Fourthly, check for upgrade paths. Some secured cards are designed to transition to an unsecured card after a period of responsible use, often with the return of your deposit. This can be a significant benefit, as it streamlines your progression to a more traditional credit product. Finally, ensure the card reports to all three major credit bureaus (Equifax, Experian, and TransUnion). This is paramount for credit building, as consistent reporting maximizes the impact of your positive payment history across the board. A card that only reports to one or two bureaus will not be as effective in establishing a comprehensive credit profile. By carefully considering these factors, you can select a credit card that not only offers easy approval but also serves as a robust tool for establishing and enhancing your creditworthiness over time. The choice of your first credit card is an important one; it sets the tone for your financial future. Prioritize cards that offer transparency in their terms and conditions, and always read the fine print before committing. Understanding the nuances of credit card terms is fundamental to making an informed decision that supports your long-term financial health, and platforms like Wikipedia can offer extensive information on the general principles of credit cards and their functions.

Best Practices for Responsible Credit Card Use

Once you’ve secured a credit card, the real work of building credit begins. Responsible use is paramount, as every action you take with your card will be reported to credit bureaus and impact your score. The following best practices will help you establish a strong credit foundation:

- Pay Your Bills on Time, Every Time: This is arguably the most critical factor in your credit score. Missing a payment can severely damage your credit. Set up automatic payments or calendar reminders to ensure you never miss a due date. Even a single late payment can set back your credit-building efforts by months or even years.

- Keep Your Credit Utilization Low: Credit utilization refers to the amount of credit you’re using compared to your total available credit. Experts recommend keeping your utilization below 30%—ideally even lower, around 10%—to demonstrate responsible management. For example, if your credit limit is $300, try to keep your balance below $90. High utilization can signal to lenders that you are over-reliant on credit.

- Pay Your Balance in Full: Whenever possible, pay your entire statement balance before the due date. This avoids interest charges, saving you money, and demonstrates excellent financial discipline. Carrying a balance, especially with high interest rates common on beginner cards, can quickly lead to accumulating debt.

- Monitor Your Credit Report: Regularly check your credit report for errors or fraudulent activity. You’re entitled to a free copy of your credit report from each of the three major credit bureaus once a year through AnnualCreditReport.com. Early detection of discrepancies can prevent significant problems down the line.

- Don’t Close Old Accounts (Eventually): As your credit history grows and you obtain better cards, resist the urge to close your oldest accounts, especially if they have no annual fee. The length of your credit history is a significant factor in your credit score, and keeping older accounts open can boost your average account age.

- Understand Your Card’s Terms: Be aware of your card’s annual fee, APR, grace period, and any other associated fees. Knowing these details helps you use your card wisely and avoid surprises. Understanding the terms helps you make informed decisions about how and when to use your card.

By diligently following these practices, you will not only build a robust credit history but also cultivate healthy financial habits that will serve you well throughout your life. Remember, building good credit is a marathon, not a sprint, requiring consistent effort and discipline. These foundational habits are crucial for long-term financial health and open doors to future financial opportunities, from mortgages to business loans. The responsible management of your first credit card lays the groundwork for all future financial interactions, setting a precedent for your reliability as a borrower.

Conclusion

Navigating the world of credit cards with no credit history can seem daunting, but as we’ve explored, there are clear, accessible pathways to establish and build a strong financial foundation. From secured credit cards that offer a guaranteed starting point to student cards tailored for academic life, and even the strategic use of authorized user status or credit-builder loans, options abound for those committed to financial responsibility. The key lies in understanding these different products, selecting the one that best suits your current situation, and then practicing diligent, responsible credit card use. By consistently paying bills on time, keeping credit utilization low, and monitoring your credit report, you will steadily build a positive credit history. This history is not just a number; it’s a testament to your financial reliability, unlocking better interest rates, easier loan approvals, and greater financial freedom. Your journey from no credit to a robust credit profile is an investment in your future. Start today, make informed choices, and commit to the best practices, and you’ll soon find that the doors to a world of financial opportunities begin to open.