6 Clear Credit Card Eligibility Factors – Know Before You Apply

Table of Contents

Credit Card Eligibility Requirements are the fundamental benchmarks set by financial institutions to assess a prospective applicant’s suitability for a credit card. Understanding these requirements is crucial for anyone looking to apply for a new credit card, as meeting them significantly increases your chances of approval and can even influence the terms of the card you receive. This comprehensive guide will break down the various factors that lenders consider, providing clarity on what you need to know before submitting an application.

Understanding Credit Card Eligibility

Credit card issuers evaluate potential cardholders based on a range of criteria to determine their creditworthiness and ability to repay debt. This evaluation helps mitigate the risk for lenders and ensures that applicants are offered products appropriate for their financial situation. The process involves a thorough review of personal, financial, and credit-related information. Successfully navigating these eligibility requirements is the first step toward securing a credit card that aligns with your financial goals, whether it’s building credit, earning rewards, or managing everyday expenses.

The criteria for credit card eligibility are not universally fixed; they can vary significantly between different card issuers and even across various types of credit cards offered by the same institution. For instance, a premium rewards card will typically have stricter requirements than a secured credit card designed for individuals building or rebuilding their credit. Therefore, understanding the specific prerequisites for the card you’re interested in is paramount. Financial institutions are legally obligated to assess an applicant’s ability to repay before extending credit.

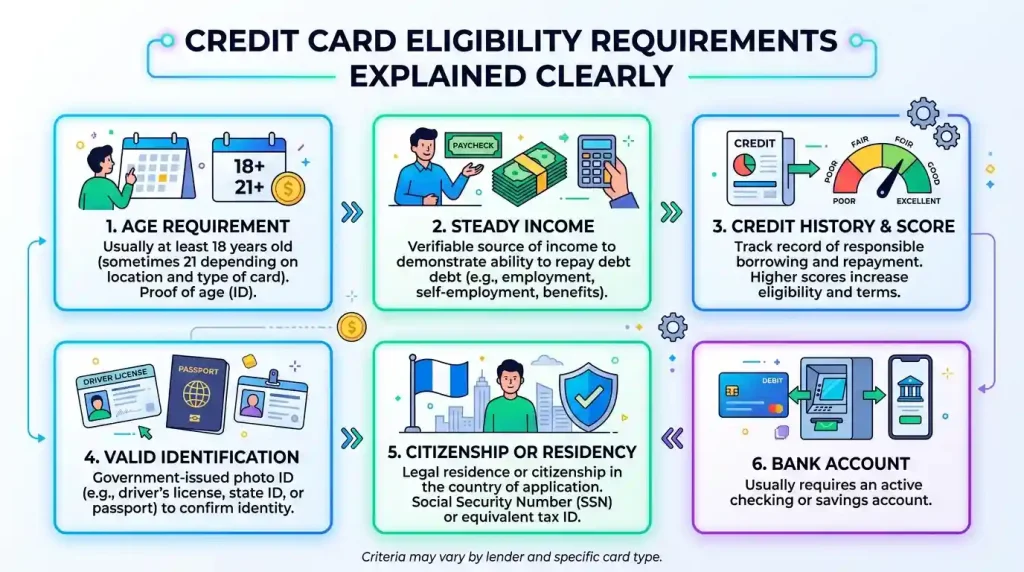

Key Eligibility Criteria for Credit Cards

Several core factors consistently appear as primary eligibility criteria across most credit card applications. These include age, income, credit score, and residency. Each plays a vital role in painting a complete picture of an applicant’s financial health and responsibility.

Age Requirements

In the United States, you must be at least 18 years old to legally apply for a credit card in your own name, as this is the legal age for entering into contracts. However, simply reaching the age of 18 does not guarantee approval. Federal law, specifically the Credit Card Accountability Responsibility and Disclosure (CARD) Act of 2009, places additional requirements on applicants between the ages of 18 and 20.

- Ages 18-20: If you are in this age group, you generally must demonstrate independent income sufficient to make minimum credit card payments on your own. This income cannot typically include household income from parents or guardians unless you have reasonable access to those funds, such as in a joint bank account, or if you reside in a community property state. Alternatively, applicants in this age range may apply with a co-signer (usually a parent or guardian) who agrees to be responsible for the debt if the primary applicant is unable to pay. However, it’s worth noting that many major credit card issuers do not allow co-signers.

- Ages 21 and older: Once you are 21 or older, you can generally list household income on your application if you have reasonable access to those funds, which can help partners or spouses qualify for credit even if they do not work. This age group faces fewer restrictions regarding income verification compared to younger applicants.

For those under 18, becoming an authorized user on a trusted family member’s or friend’s credit card account is a common way to begin building a credit history. As an authorized user, you receive a card linked to another person’s account, allowing you to make purchases, but the primary cardholder remains responsible for all payments.

Income and Employment Stability

Your income is a significant factor in credit card eligibility because lenders need assurance that you can afford to make at least the minimum payments on your new credit card. While there isn’t a universally mandated minimum income requirement, individual issuers set their own internal guidelines, which can vary greatly depending on the type of card. Premium cards with extensive rewards and benefits typically demand higher income levels than starter or secured cards.

When applying for a credit card, you’ll be asked to provide your annual income. This can encompass a broad range of sources, not just salary from full-time employment:

- Full-time or part-time employment wages, salary, bonuses, tips, or commissions.

- Self-employment or freelance income.

- Retirement income, such as IRA or 401k withdrawals, Social Security, or pension payments.

- Rental income from properties you own.

- Investment income, including dividends, interest, and capital gains distributions.

- Public assistance, such as certain disability income.

- Insurance payments providing long-term coverage.

- Income from a spouse, household member, or partner if you have reasonable access to these funds (typically for applicants 21 and older).

- Financial aid, including grants, scholarships, or some student loans.

- Allowance received from a parent or family member.

Issuers also consider your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to manage new credit responsibilities, making you a less risky applicant.

Credit Score and History

Your credit score is arguably one of the most critical factors influencing credit card approval and the terms you’ll receive. This three-digit number, typically ranging from 300 to 850 (FICO and VantageScore models), acts as a snapshot of your creditworthiness, estimating how likely you are to repay debt on time. The higher your score, the better your chances of approval and access to more favorable interest rates and rewards programs.

Lenders use credit scores as a risk indicator; a high score suggests you are a lower financial risk. Most credit cards, particularly those with strong rewards, require applicants to have a “good” to “excellent” credit score, generally considered to be 670 or higher on the FICO scale.

Key components that make up your credit score include:

- Payment History: Consistently making on-time payments is the most important factor, accounting for 35% of your FICO Score.

- Amounts Owed/Credit Utilization: This refers to the amount of credit you’re using compared to your total available credit. Experts recommend keeping your credit utilization ratio (CUR) below 30%, with lower percentages being even better.

- Length of Credit History: A longer credit history with responsibly managed accounts generally looks more favorable to lenders.

- Credit Mix: Having a diverse mix of credit accounts (e.g., credit cards, installment loans) can positively impact your score.

- New Credit/Credit Inquiries: Applying for multiple new credit accounts in a short period can temporarily lower your score due to “hard inquiries” on your credit report.

If you have a limited or poor credit history, options like secured credit cards or becoming an authorized user can help you establish or rebuild your credit.

Residency and Identity Proof

Credit card issuers require applicants to provide specific personal and identifying information to verify their identity and comply with regulations. This information typically includes:

- Full legal name.

- Date of birth.

- Current residential address (not a P.O. Box), and proof of address if it differs from your ID. Some cards may only be available to residents of particular cities or states.

- Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). This allows lenders to access your credit report and history.

- Employment status.

Lenders use this data to verify your identity and review your financial history. Providing accurate information is essential, as even minor mistakes can lead to application denial.

The Role of Your Credit Score in Eligibility

Your credit score is often the first and most impactful piece of information a credit card issuer considers when you apply for a new account. It serves as a strong indicator of your financial behavior and risk level. Understanding the different credit score ranges and what they typically qualify you for can significantly guide your application process.

There are two primary credit scoring models used by lenders: FICO Score and VantageScore. Both models assess your creditworthiness based on similar factors but may weigh them differently.

FICO Score Ranges:

- Exceptional: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

VantageScore Ranges:

- Excellent: 781-850

- Good: 661-780

- Fair: 601-660

- Poor: 500-600

- Very Poor: 300-499

Generally, a credit score of 700 or higher gives you good odds of approval for most credit cards, particularly those with premium rewards. However, cards designed for individuals with fair or poor credit are also available, though they might come with higher interest rates and fewer perks. Secured credit cards, which require an upfront deposit, are often accessible even with lower scores (e.g., around 500-580), serving as a crucial tool for building or rebuilding credit.

It’s important to remember that your credit score is not the sole determinant. Even with a good credit score, an application can be denied due to other factors such as high debt relative to income, a short credit history, or too many recent credit applications. Conversely, a high income alone may not secure approval if your credit score is low.

Navigating Different Card Types and Their Requirements

The world of credit cards is diverse, with various types designed to cater to different financial needs and credit profiles. Understanding the specific eligibility requirements for each category can help you choose the right card and avoid unnecessary application rejections.

| Credit Card Type | Typical Credit Score Range | Income Requirements | Key Characteristics & Eligibility Notes |

|---|---|---|---|

| Secured Credit Cards | Poor to Fair (300-669 FICO) | Flexible, often minimal or no specific requirement; focuses on ability to provide a security deposit. | Requires a cash deposit that often serves as your credit limit. Ideal for building credit from scratch or rebuilding damaged credit. Less stringent income checks as the deposit mitigates risk. |

| Student Credit Cards | No Credit to Fair (300-669 FICO) | Proof of independent income required for applicants under 21; typically more lenient due to student status. | Designed for college students, often with limited or no credit history. May require proof of enrollment. Can offer rewards tailored to student spending. |

| Unsecured Cards (General) | Fair to Good (580-739 FICO) | Moderate to good income expected, sufficient to manage payments; DTI ratio considered. | Standard credit cards without a security deposit. Requirements vary widely based on specific card features (e.g., rewards, low APR). Your credit limit is based on your income and credit history. |

| Rewards & Travel Cards | Good to Excellent (670-850 FICO) | Higher income often required due to potential for higher credit limits and benefits. | Offer points, miles, or cash back on purchases. Can come with annual fees. Strict credit score and income requirements for approval, given the benefits offered. |

| Premium/Luxury Cards | Excellent (740-850 FICO) | Very high income expected, often with substantial assets, to qualify for exclusive perks and high credit limits. | Exclusive cards with extensive travel perks, concierge services, and high annual fees. Require exceptional credit and significant financial stability. |

| Business Credit Cards | Good to Excellent (670-850 FICO) | Business revenue and applicant’s personal income considered. Most issuers require a personal guarantee. | Designed for business expenses. Eligibility may depend on business age, revenue, and the applicant’s personal credit score. No strict incorporation required for most basic business cards. |

Each card type serves a specific segment of the market, and understanding these distinctions is key to a successful application. For example, if you are new to credit, applying for a premium travel card is likely to result in a denial, whereas a secured or student card would be a more appropriate starting point.

Common Reasons for Credit Card Application Rejection

Even with a solid understanding of eligibility requirements, credit card applications can sometimes be denied. It’s important to be aware of the common pitfalls that can lead to rejection so you can address them before applying or understand why an application might have been unsuccessful.

Some of the most frequent reasons for denial include:

- Poor or No Credit History: A low credit score or a lack of established credit history makes it difficult for lenders to assess your risk, often leading to denial, especially for unsecured cards.

- Insufficient Income: If your income is deemed too low to comfortably handle the potential credit limit and minimum payments, your application may be rejected.

- High Debt-to-Income (DTI) Ratio: Lenders are wary of applicants who already have a significant portion of their income dedicated to existing debt payments. A high DTI suggests you might struggle with additional credit.

- Too Many Recent Credit Applications/Hard Inquiries: Applying for multiple credit cards within a short period can signal financial distress to lenders and result in denials. Each application typically results in a “hard inquiry” on your credit report, which can temporarily lower your score.

- Negative History with the Issuer: If you’ve had a past negative relationship with the specific bank or issuer (e.g., defaulted on a previous card, an unresolved collection), they may be disinclined to approve a new application.

- Errors on Your Application: Simple mistakes, such as an incorrect address, transposed digits in your Social Security number, or an inaccurate income total, can lead to automatic denial.

- High Credit Utilization Ratio: If you are already using a large percentage of your existing credit limits (typically over 30%), it can indicate over-reliance on credit and negatively impact your chances.

- Recent Bankruptcy: A recent bankruptcy filing is a major red flag for lenders and will likely result in a denial for most standard credit cards.

If your application is denied, the issuer is legally required to send you an adverse action notice explaining the primary reasons for the denial. This letter can be invaluable in understanding what areas you need to improve before reapplying.

Improving Your Chances of Approval

Even if you don’t meet all the ideal eligibility criteria today, there are proactive steps you can take to strengthen your financial profile and increase your odds of credit card approval in the future.

Here are actionable strategies to improve your eligibility:

- Improve Your Credit Score: This is fundamental. Focus on making all payments on time, as payment history is the most significant factor in your credit score. Work to reduce existing debt and keep your credit utilization ratio low (ideally below 10-30%). You can monitor your credit score through various free services to track your progress. For a deeper dive into credit scores and their importance, consider consulting resources like this Federal Trade Commission guide on credit scores.

- Increase Your Income and Reduce Debt: While increasing income takes time, it directly improves your debt-to-income ratio, making you a more attractive applicant. Actively paying down outstanding debts, especially high-interest ones, will also lower your DTI.

- Check for Prequalification/Pre-approval: Many card issuers offer tools that allow you to check if you’re prequalified or pre-approved for certain cards without impacting your credit score (this is a “soft inquiry”). This can give you an idea of your approval odds before you submit a formal application, which involves a “hard inquiry” that can slightly ding your score.

- Avoid Multiple Applications: Space out your credit card applications. Applying for too many cards in a short period can appear desperate to lenders and lead to denials due to multiple hard inquiries. A good rule of thumb is to wait at least 3 to 6 months between applications if you’re actively seeking new credit.

- Correct Errors on Your Credit Report: Regularly review your credit reports from all three major bureaus (Experian, Equifax, and TransUnion) for inaccuracies. Errors can negatively impact your score and lead to undeserved rejections. You are entitled to a free copy of your credit report annually from each bureau.

- Establish a Banking Relationship: Having an existing relationship with a bank, especially a checking account with direct deposit, can sometimes improve your chances of approval for their credit cards. They may already have insight into your financial habits.

- Consider Secured or Student Credit Cards: If you have limited or poor credit, these cards are specifically designed to help you build credit responsibly. They have more lenient approval requirements and can serve as a stepping stone to better unsecured cards.

Conclusion

Meeting credit card eligibility requirements is a multi-faceted process that goes beyond just having a good credit score. It involves a holistic assessment of your age, income, employment stability, debt-to-income ratio, residency, and overall financial history. While the specific criteria can vary between issuers and card types, a clear understanding of these factors empowers you to approach the application process strategically. By proactively managing your finances, maintaining a strong credit profile, and selecting cards appropriate for your current financial standing, you significantly increase your likelihood of approval. Remember that a credit card is a powerful financial tool, and responsible use is key to unlocking its full potential and building a healthy financial future.